2025 H1 Report

CANADIAN M&A ACTIVITY SLOWS IN VOLUME BUT SHOWS VALUE RESILIENCE THROUGH MID-2025

TORONTO (Sept. 30, 2025) — Mergers and acquisitions in Canada through the first half of 2025 reflected a mixed picture: fewer deals amid economic headwinds, but surging values driven by blockbuster transactions.

Deal volume dipped across major trackers, hitting multiyear lows in some metrics, while total values climbed sharply year over year. The trends, drawn from reports by PwC Canada, ION Analytics and Kroll, underscore resilience in larger deals despite uncertainty from trade tensions and interest rates.

As of late September, full third-quarter data remains preliminary, with comprehensive reports expected in October. First-half figures, however, paint a clear snapshot of year-to-date activity compared with 2024.

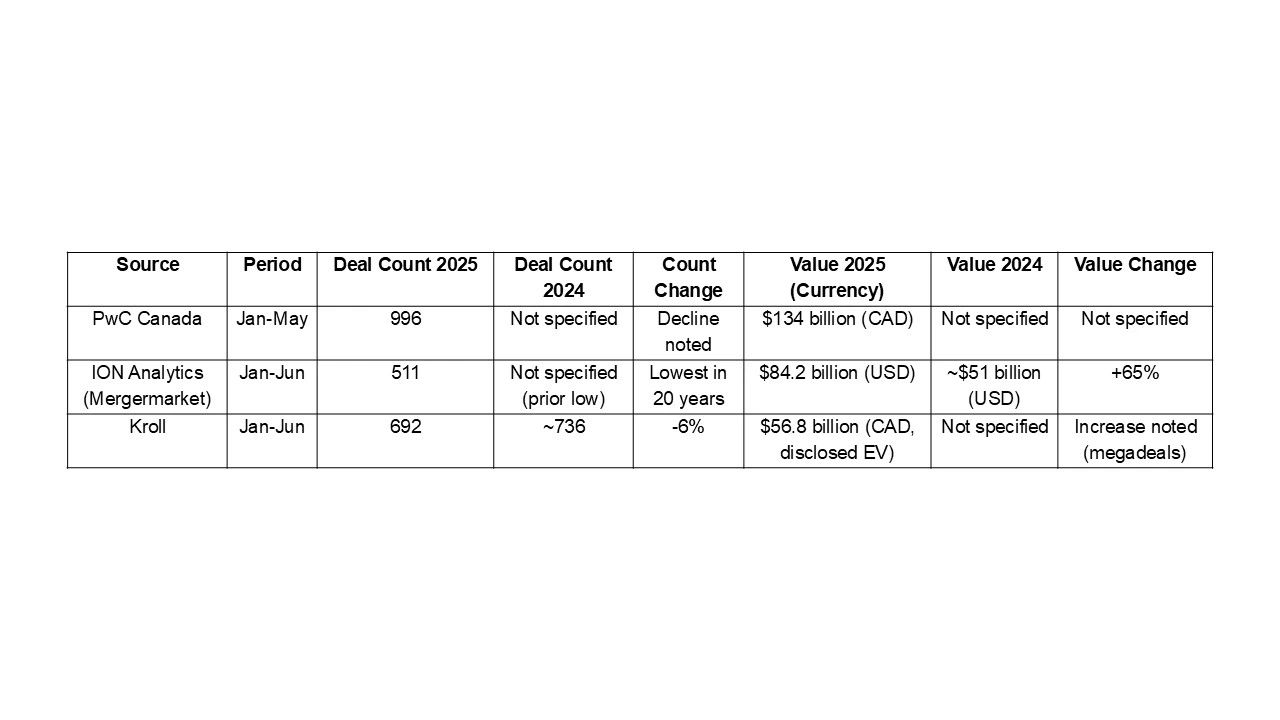

Key Metrics: H1 2025 vs. H1 2024

Data varies by source due to differences in scope — such as minimum deal sizes, inclusion of undisclosed values and focus on announced versus completed transactions. Here's a comparison based on the latest available:

PwC's mid-year update highlighted a slowdown in inbound and domestic deals, with outbound Canadian acquisitions rising.

The firm's data covers announced deals without a minimum threshold, capturing broader activity.

ION Analytics reported the sharpest value jump, fueled by sectors like energy and utilities, though deal counts fell to the lowest half-year level since tracking began two decades ago.

Its figures focus on deals above $5 million, emphasizing cross-border flows.

Kroll noted a modest volume drop but pointed to megadeals — those over $1 billion — as a bright spot, with 39 such transactions averaging $3 billion each, up from 21 in 2024.

The report attributes value growth to strategic consolidations in private equity and industrials.

A Dentons analysis aligned with the value surge, pegging H1 totals at 113.7 billion Canadian dollars, a nearly 70% increase from the prior year.

What's Driving the Divergence?

Economic factors loom large. Persistent inflation, U.S. tariff threats and softening commodity prices curbed smaller deals, pushing buyers toward high-confidence, large-scale moves. Private equity firms, flush with dry powder, targeted resilient sectors like technology and renewables.

Cross-border activity, which accounts for nearly half of Canadian M&A, showed softening inbound flows early in the year before rebounding.

U.S. investors, a key driver, pulled back amid policy shifts, per Torys LLP's mid-year outlook.

Yet optimism persists for the second half. Falling interest rates and improving U.S.-Canada trade dynamics could unlock pent-up demand, analysts say. PwC forecasts a gradual uptick, particularly in financial services.

Looking Ahead to Year-End

With Q3 wrapping up, early signals from sector updates — like a dip in beverage M&A to 19 deals year to date — suggest volume pressures linger.

Financial services, however, saw a slight softening but innovative structures to navigate regulations.

Dealmakers eyeing 2025's close should prioritize speed and due diligence, as volatility favors the prepared. Full-year tallies will clarify if value gains offset volume woes, potentially setting a foundation for 2026 recovery.

Sources

- PwC Canada 2025 Mid-Year M&A Update: https://www.pwc.com/ca/en/services/deals/trends/mid-year-update.html

- ION Analytics Disruptive 1H25 Report: https://ionanalytics.com/insights/mergermarket/disruptive-1h25-fails-to-stem-canadian-ma-deal-flow/

- Kroll Canadian M&A Insights Summer 2025: https://www.kroll.com/en/publications/m-and-a/canadian-ma-industry-insights-summer-2025

- Dentons Canadian M&A Second Half 2025 Alert: https://www.dentons.com/en/insights/alerts/2025/august/18/canadian-manda-in-the-second-half-of-2025

- Torys LLP U.S. Cross-Border M&A Outlook: https://www.torys.com/our-latest-thinking/torys-quarterly/q3-2025/us-crossborder-ma

- Additional context from PwC Outlook: https://www.pwc.com/ca/en/services/deals/trends.html