Build a fast-growing business that sells for a premium

Why the right time to add functional leadership is almost always sooner than it feels

By Karl E. Sigerist, Jr., ICD.D

Author, Selling Your Canadian Business: A Step-by-Step Guide to Maximizing Value and Securing Your Legacy

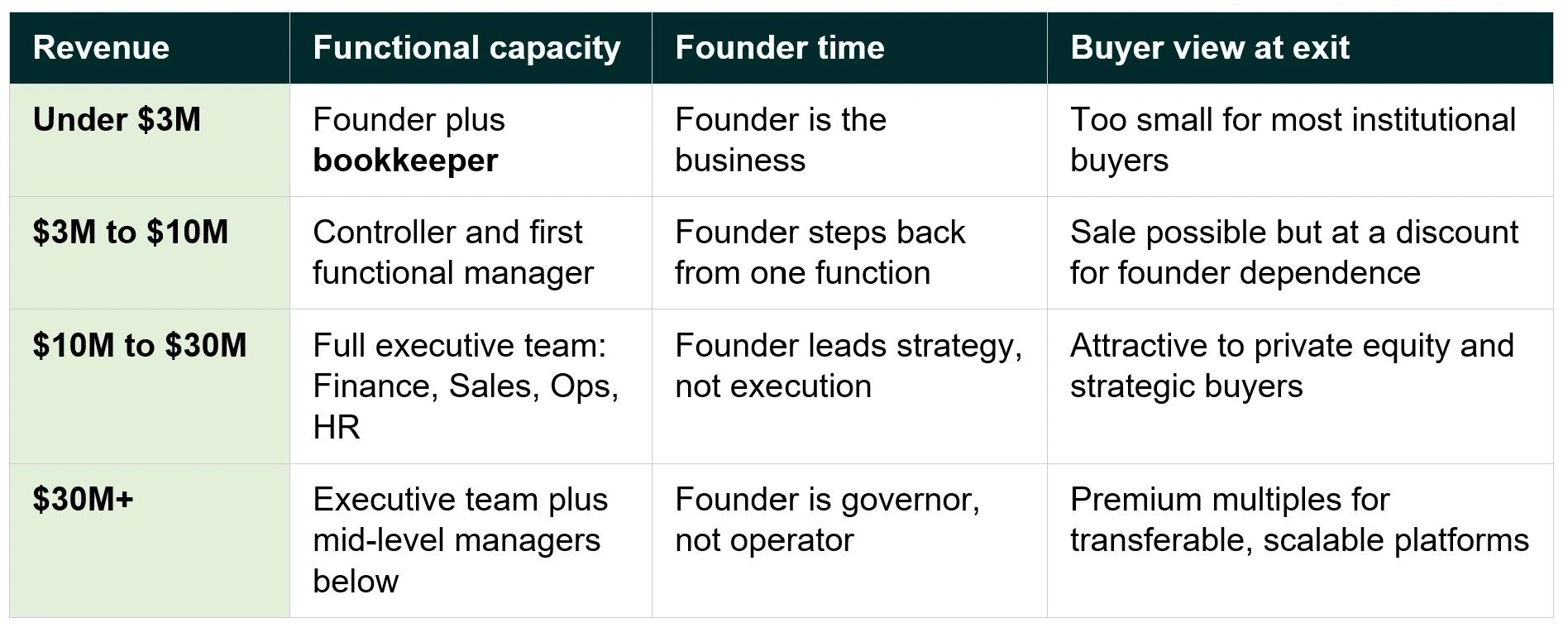

There is a moment in every successful Canadian business when the owner realizes the company has outgrown the way it is being run. The signs are familiar. The calendar is full but the strategy is thin. Decisions that used to take minutes now take weeks because the founder is the bottleneck on too many of them. The team is loyal and capable, but no one below the founder is making meaningful calls without checking in first. Revenue continues to climb, but it climbs because the founder works harder, not because the company has built capacity that does not require the founder.

In my work with Canadian business owners, and in writing Selling Your Canadian Business, I have come to believe this moment is the single most important inflection point in the life of a private business. Most owners reach it somewhere between $5 million and $15 million in revenue. The question that follows is the one this article is about. When should an owner add functional leaders to take over the work the founder has been doing? Hire too soon and the company cannot afford the salaries. Hire too late and the company stops growing, or worse, the owner cannot sell when the time comes because the business cannot operate without them.

The way out of that bind is not a hiring rule. It is a different way of thinking about what the company is worth, and what makes it worth more.

What makes a private business valuable

Three things determine what a private Canadian business is worth to a future owner. The first is how fast the business is growing. The second is how much profit it generates from each dollar of revenue. The third, and most often overlooked, is how much of that growth and profit depends on the current owner.

The third factor is the one that quietly governs the other two. A business that grows at 20 per cent a year with healthy margins, but whose growth flows entirely through the relationships and decisions of one person, is worth materially less than a business growing at 15 per cent with slightly lower margins. However, it has a team that can carry the work without the founder. Buyers understand this. They price it into every offer.

The valuation profession has a name for it. It is called the key person discount, and it is the reduction a buyer applies to a business when it depends too heavily on one individual. In Canada, the professional authority on business valuation is the Chartered Business Valuator Institute (CBV Institute), which has set the practice standard since 1971. CBVs are recognized by the courts and by the Canada Revenue Agency as the experts on questions of private business value. The CBV Institute has published extensively on the role of personal goodwill versus transferable commercial goodwill in private business valuation, which is the technical name for the same idea I am describing here.

The same principle is recognized internationally. In the United States, the Internal Revenue Service (the American equivalent of the Canada Revenue Agency) formalized it as Revenue Ruling 59-60, which is still the foundational guidance used by valuators on both sides of the border when valuing closely held businesses. The point is not that an American tax ruling governs a Canadian business sale. The point is that the underlying principle, that a business which depends too heavily on one person is worth less than one which does not, is universal in the valuation profession and has been for more than 60 years.

The published range of the key person discount is well established. Shannon Pratt, whose textbook is the standard reference in the field, places it between 10 and 25 per cent of enterprise value. Aswath Damodaran of NYU Stern, whose writing on private company valuation is widely used by Canadian and American practitioners, cites a similar range and notes that the discount tends to be larger for smaller, more service-intensive businesses. In Canadian practice, a CBV would assess the discount applicable to a specific business by examining the depth of the management team, the transferability of customer relationships, and the durability of the brand independent of the founder.

The math is straightforward. A Canadian business with $3 million in EBITDA, trading at a normalized multiple of 6.0x, has an enterprise value of $18 million. A 20 per cent key person discount strips $3.6 million off that. In my experience, the cost of building a credible functional team capable of removing that discount is almost always materially less than $3.6 million.

The mistake most Canadian business owners make

The mistake is not that owners hire the wrong people. It is that owners delay too long. The Business Development Bank of Canada (BDC) has documented this pattern across multiple studies of Canadian small and medium-sized businesses. Canadian SMEs are less likely than American peers to adopt formal management practices, to measure productivity systematically, and to invest in structured management depth. The Organisation for Economic Co-operation and Development (OECD), in its 2025 Economic Survey of Canada, identified this gap as one of the contributors to the productivity difference between Canada and the United States.

The reason is not lack of capability. It is psychology. The cost of an executive hire shows up immediately on the profit and loss statement, in the same quarter the offer letter is signed. The benefit, which is faster growth, more focused founder time, lower business risk and a higher exit multiple, shows up over three to five years and is partially invisible. Faced with a visible cost and an invisible benefit, most owners delay. The delay feels like financial discipline. In my experience advising Canadian owners through their exits, it is actually the most expensive decision they make.

A simple framework for the decision

There is a useful rule that has migrated out of the software industry into broader use. It is called the Rule of 40. It states that the revenue growth rate plus the EBITDA margin should exceed 40 per cent. The number was developed by venture capital investors as a quick test of whether a software company was growing efficiently. McKinsey and Company validated it empirically with a study of more than 200 software companies, finding that those meeting the Rule of 40 traded at enterprise-value multiples roughly two to three times those that did not. Bain and Company independently found that companies sustaining a score above the line traded at valuations roughly double those of companies below.

The original number applies most strictly to software. For other sectors, the equivalent is lower because the underlying economics are different. Manufacturing businesses typically operate with EBITDA margins of 10 to 15 per cent and growth rates of 5 to 10 per cent, so the practical benchmark sits around 25. Professional services businesses run at 15 to 25 per cent margins with growth in the high single digits, so the benchmark sits around 30. Distribution sits lower because margins are thin. Healthcare services sit higher because the underlying demand is more stable.

The point is not the precise number. The point is the discipline. An owner considering an executive hire can use the rule to answer one question. After the hire is made, does the combined score (revenue growth percentage plus EBITDA margin percentage) remain at or above the sector benchmark? If yes, the hire is consistent with creating value. If no, the hire is either premature, too expensive for the stage, or expected to produce growth that is not realistic.

The rule disciplines both errors at once. It catches owners who would otherwise hire too aggressively because such a hire would push the score below the line. It also catches owners who would otherwise delay too long because a business growing at five per cent with a 12 per cent margin is sitting at 17, well below any reasonable benchmark. It is failing to invest in the leadership capacity that growth would require.

What a build-out actually looks like for a Canadian lower-middle-market business

The build-out is not all at once. It is a sequence, and the sequence matters more than the calendar.

Three principles guide the sequence. First, the first hire goes into the function that is the binding constraint on the next 18 to 24 months of growth. If the business cannot grow because the founder is the only one closing deals, the first hire is a sales leader. If the business cannot grow because operations are stretched, the first hire is in operations. The hire that creates the most value is the one that unblocks the next leg of growth.

Second, finance professionalizes early. A strong controller, eventually backed by a VP Finance or fractional CFO, is the foundation that every other hire stands on. A founder who does not have accurate, timely financial reporting cannot evaluate whether subsequent hires are working. Buyers in the diligence process always start with finance. A finance function that has been professionalized for three years before sale is the single highest return investment available in the prelude to a transaction.

Third, fractional and interim executives are the bridge. A fractional CFO in Canada typically costs between $60,000 and $150,000 a year for one to two days a week, compared with $280,000 to $500,000 fully loaded for a permanent CFO. A fractional COO ranges from $36,000 to $180,000. A fractional CMO ranges from $50,000 to $150,000. The fractional market in Canada is mature enough now to fill the gap between needing senior leadership and being able to support it permanently. It is the most underused tool available to lower-middle-market Canadian owners.

What a future buyer actually wants to see

It is worth stepping into the head of the buyer. A private equity sponsor, a strategic acquirer, or a search fund principal looking at a Canadian business in the $5 million to $50 million revenue range is asking three questions in the diligence process.

Does this business have a credible plan to grow without the current owner? Not a forecast. Not a hope. A plan that is anchored in the team that will execute it. The buyer is looking for at least one functional executive in each of the critical areas, with a track record of carrying authority and producing results without daily direction from the owner.

Where does the current EBITDA actually come from? If the answer is that the founder personally accounts for the major customer relationships, the major supplier relationships, the pricing decisions and the strategic direction, the buyer applies the key person discount. If the answer is that those relationships and decisions are distributed across a team, the discount disappears.

What happens to revenue in the first 12 months after closing if the founder leaves immediately? This is the question that drives the discount on offers and the structure of earn-outs. The further the answer is from "essentially nothing happens," the more the price comes down and the more of it gets pushed into deferred consideration.

The owner who builds for these three questions, starting three to five years before a planned exit, sells at a premium. The owner who does not, sells at a discount, accepts more risk in the deal structure, or finds the business is unsellable at any reasonable price.

The Canadian succession window

The timing of this question matters because of where Canada sits in its business succession cycle. The Canadian Federation of Independent Business (CFIB) reported in 2023 that 76 per cent of Canadian small business owners intend to exit their business within 10 years, putting more than $2 trillion in business assets in play. Only nine per cent of those owners have a formal succession plan in place. The same CFIB research identified the four main barriers to a successful succession as finding a suitable successor, difficulty in valuing the business, the business's dependence on the owner's active involvement, and securing financing for the successor.

The middle two of those four barriers are the same problem from different angles. A business is difficult to value precisely because it depends too heavily on the owner. The value sits in the owner, not in the business. Removing that dependency is the single most reliable way to address both barriers at once.

For a Canadian founder building a business with the intention of selling it well, the implication is favourable. The talent is available. The bridges (fractional and interim executives) are available. The buyer demand is documented and growing. The window in which to build the team that justifies the exit multiple is open, but it is finite. In my experience, the team needs to be in place 18 to 24 months before the sale process begins for buyers to credit it as durable rather than recent.

What to do this quarter

For an owner who recognizes themselves in this description, four practical steps make sense regardless of where the business sits today.

- Identify the binding constraint. Which function, if it were led by someone other than the owner, would unblock the next leg of growth? The answer is usually clear once asked directly. It is also usually different from what the owner thinks at first glance.

- Engage a fractional executive in that function for three to six months. The cost is modest. The information return is high. The right fractional executive either grows into the permanent hire or helps the owner write the job description for the search that follows.

- Professionalize finance, if it has not been already. Monthly financial statements within 15 business days of period end. A 13-week cash forecast. A budget against which actuals are reviewed each month. None of this is expensive at the scale of a $5 million to $50 million business. All of it pays back in clearer decisions every month and a smoother diligence process when the time comes.

- Apply the sector-adjusted Rule of 40 to the business as it stands today, and again after each prospective hire is modelled. If the score after the hire falls below the sector benchmark, the hire needs to be redesigned or rephased. If the score is well above the benchmark, the business may be underinvesting in leadership and leaving value on the table.

A final thought

The owner who optimizes for the highest possible EBITDA margin in the current quarter will produce a respectable business. The owner who optimizes for the fastest possible revenue growth without regard to margin or risk will produce a fragile one. The owner who optimizes for the value of the business to a future owner, three or five years from now, will produce something else. A business that grows faster than its peer group because it has the leadership capacity to grow. A business that produces healthy profit margins because the leadership capacity is matched to revenue, not running ahead of it or behind it. A transferable business because the founder is one person on the team, not the entire team.

That is the business worth building. It is also the business worth selling.

Sources and further reading

- Chartered Business Valuator Institute (CBV Institute), Canada's professional authority on business valuation, recognized by the courts and the Canada Revenue Agency: https://cbvinstitute.com

- Canadian Federation of Independent Business (CFIB). Succession Tsunami: Preparing for a Decade of Small Business Transitions, 2023: https://www.cfib-fcei.ca/en/media/over-2-trillion-in-business-assets-are-at-stake-as-majority-of-small-business-owners-plan-to-exit-their-business-over-the-next-decade

- Business Development Bank of Canada. Productivity of Canadian Companies: https://www.bdc.ca/en/about/analysis-research/productivity-2016

- Organisation for Economic Co-operation and Development. OECD Economic Surveys: Canada 2025, Raising Business Sector Productivity: https://www.oecd.org/en/publications/2025/05/oecd-economic-surveys-canada-2025_ee18a269.html

- Pratt, Shannon. Valuing a Business: The Analysis and Appraisal of Closely Held Companies. Standard reference for the key person discount.

- Damodaran, Aswath. The Little Book of Valuation. John Wiley and Sons. Companion writing at https://aswathdamodaran.substack.com

- Chen, Charles et al. SaaS and the Rule of 40: Keys to the critical value-creation metric. McKinsey and Company, 2021: https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/saas-and-the-rule-of-40-keys-to-the-critical-value-creation-metric

- Bain and Company. Hacking Software's Rule of 40: https://www.bain.com/insights/hacking-softwares-rule-of-40/

- Churchill, Neil C. and Virginia L. Lewis. The Five Stages of Small Business Growth. Harvard Business Review, May 1983: https://hbr.org/1983/05/the-five-stages-of-small-business-growth

- Government of Canada, Innovation, Science and Economic Development. Key Small Business Statistics 2025: https://ised-isde.canada.ca/site/sme-research-statistics/en/key-small-business-statistics/key-small-business-statistics-2025

Stay informed

This article is one piece of a larger body of work I publish for Canadian business owners thinking about the value of their company and what it will take to sell it well one day. The full resource library at sellingyourcanadianbusiness.ca includes The Canadian Exit Briefing monthly newsletter, the podcast, the YouTube channel, downloadable guides, recorded interviews, upcoming speaking engagements and the full blog archive.

Subscribe and explore the resource library at https://sellingyourcanadianbusiness.com/

Karl E. Sigerist, Jr., ICD.D is the author of Selling Your Canadian Business: A Step-by-Step Guide to Maximizing Value and Securing Your Legacy.