HOW PROFITABILITY THRESHOLDS DRIVE GREATER BUSINESS EXIT VALUE

When planning for the sale of a business or business unit, size matters.

Revenue matters, but from the prospective of business buyers, the size of a company’s EBITDA is particularly important. Both strategic and financial buyers alike view EBITDA (earnings before interest, taxes, depreciation, and amortization) as a key yardstick for where the business sits relative to others within a particular industry. Buyers are also likely to compare other metrics surrounding EBITDA like what is the EBITDA margin percentage when compared to overall sales revenues? How much “DA” (depreciation & amortization) is included in the overall EBITDA calculation? While these other metrics are certainly important, the overall earnings number will be the very first barrier in attracting various buyers to the business. Knowing the level of earnings required to attract diverse types of suitors is helpful when you want to reverse engineer your business sale to maximize your company’s selling price and exit value.

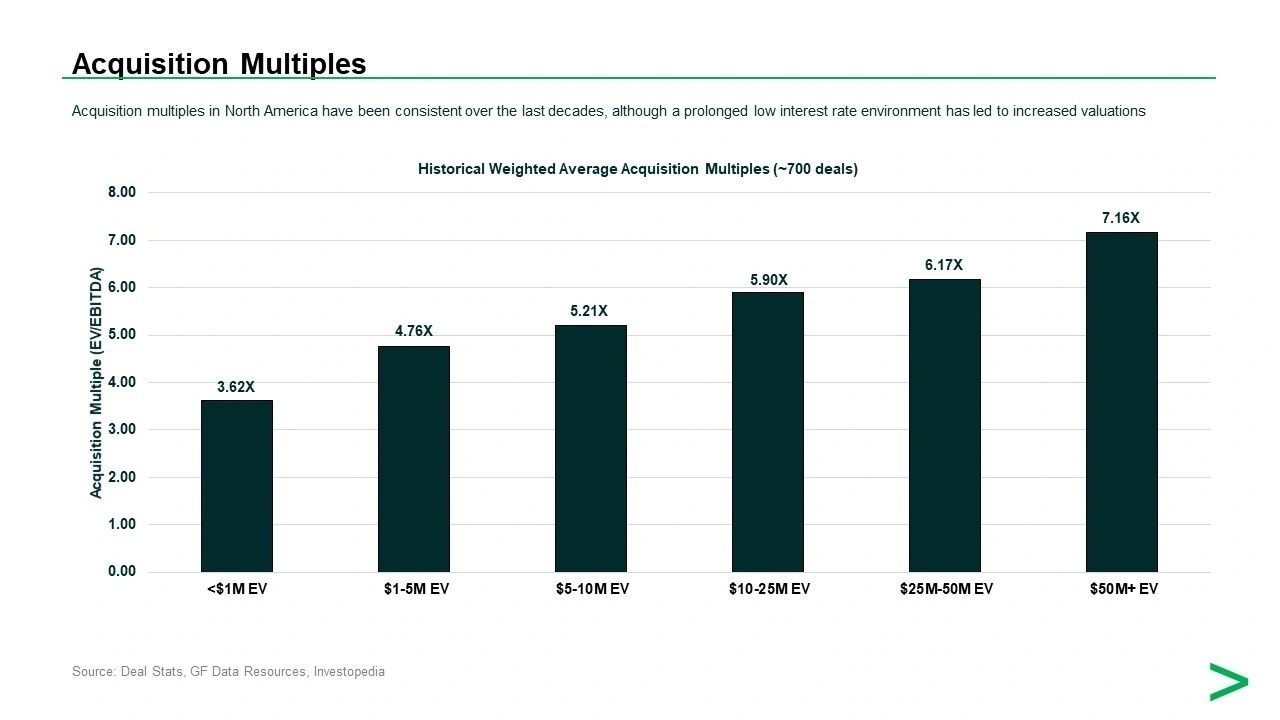

North American transaction acquisition multiples have been consistent over the last decades, although a prolonged low interest rate environment in Canada and the United States has led to increased valuations. From the data one can observe the following which together with our own experience leads us to the following potential business exit value.

EBITDA=$1,000,000+ (~4.76 Multiple)

Just like businesses in general, there are many strategic, search funds, family offices, serial entrepreneurs and private equity buyers that will play below the $1M EBITDA threshold. Many of them do so in hopes that they can play the arbitrage game and acquire companies on the cheap. It is getting more difficult to buy below market, especially as companies increase in size. It is easier for buyers to acquire below market when they move lower down the value chain as many of these companies have customer/regional concentration issues, unsophisticated systems and other not-so-desirable characteristics that create wiggle-room for buyer negotiation.

While surpassing the $1M mark is somewhat of a signal, the most legitimate and healthy financial and strategic buyers will be playing well above this level, holding out for the companies with greater sophistication and better company preparation for scale. Many will be looking for that company that could be used for bolt-on acquisitions. In fact, it is the $1M to $5M EBITDA size threshold that many a financial or strategic buyer will target as a bolt-on acquisition in an industry roll-up.

EBITDA=$2,000,000 to $3,000,000+ (~4.76 – 5.9 Multiple)

Something tends to happen between the $2M and $3M levels of EBITDA. First, companies get more complex. They become more sophisticated in their accounting, resource planning, operations, and sales. They tend to hire up-market talent and thus the business becomes more of a well-oiled machine. In most cases, the family bookkeeper (or someone simply trained internally) no longer is the keeper of the financial statements. In short, the EBITDA is a signal of a more mature target. The increase in sophistication may not always the case, but the EBITDA helps signal that it is certainly a potentiality. This level of EBITDA is at least a prerequisite for many a buyer. There is also a slight bump in the EBITDA multiple paid for businesses in this range.

Additionally, once a company crests the $2M EBITDA number they become less of a potential target for individual buyers. This is a distinction. When companies are small, they are more easily purchased by individual buyers looking to acquire a lifestyle business. As valuations creep above that level, buyers tend to get a bit more sophisticated, in many cases, financial and strategic buyers bring their own equity and debt and structure the deals as they see fit. In other words, the larger pool of more unsophisticated buyers begins to shrink.

This is also the level at which many strategic and financial buyers will begin to “take a look.” Many entrepreneurs, investment funds and small cap public companies has made their reputation as a buyer in this lower middle-market range, growing the business both organically and inorganically and then selling the company or operating business unit later to another party higher up the acquisition food chain.

EBITDA=$5,000,000 + (6.17 – 7.16 Multiple)

The most well-known strategic and financial buyers will not pay attention until you reach a minimum of $5M EBITDA, but many prefer $5M. In fact, some have arbitrary, but set and disciplined thresholds above $5M. This level of EBITDA could be truly deemed “the middle market.” Most would consider anything below the $5M EBITDA size range as “lower” middle-market.

Once a company reaches this range of EBITDA, the multiples paid increase yet again. Due to the large amount of investor capital available in the market, it is very difficult to find a “good deal” or an “arbitrage play” when companies reach this size. Multiples are higher, companies get more expensive, but the opportunity for scaled returns also increases.

When it comes to doing deals, both buyers and intermediaries have their own internal gauge on how low they will dip before they agree to take on a mandate or start the process. For both buyers and intermediaries, the argument is most often a time-value trade-off. It takes just as much time and effort to source, close and manage a deal that is $1M in EBITDA as it does to do a deal that is $5M. There is a vast difference in the payout for the same amount of time/effort input, however. For the financial buyers, the conundrum is compounded by the amount of capital a fund may have available to deploy under a given mandate. If the fund is large enough, doing deals under $5M would simply be a waste of time and not a general effective use of financial and human resources.

Conclusion

Entrepreneurs and shareholders looking to sell their businesses should consider the ramifications and adjust their expectations of the magical EBITDA size thresholds both intermediaries and buyers will want to see before seriously engaging with you. It may be helpful to adjust toward growth, but also to prepare the business internally. EBITDA may be the first barrier, but other strategic, human resources, operations, sales, marketing, accounting, and finance hurdles may await an entrepreneur or group of shareholders that is simply expecting interest in their business by targeting the wrong audience buyers for a successful business transition, divesture, or sale.

The Shaughnessy Group is a lower middle-market corporate finance advisory firm. With our collective experience, access to industry data and resources we can confidentially examine a company to provide a realistic value range. Request your free report.

Seeking the Latest Insights?

Subscribe to our newsletters, register for upcoming events, download free content from our library of resources below.