LEASE EXTENSIONS IN CANADIAN LOWER MIDDLE MARKET M&A

Lease Extensions in Canadian Lower Middle Market M&A: The Hidden Risks of Adding Two Years to Your Term

In Canada's lower middle market M&A landscape, deals involving businesses with $5–$50 million in revenu, —the separation of operating companies (OpCo) from real estate holdings (HoldCo) is a staple strategy for owners seeking tax efficiency and asset protection. When selling OpCo via a share purchase, the existing lease (already at market rates and terms) transfers seamlessly to the buyer. With three years remaining, proposing a "reset" to extend it to five years, preserving all current provisions—seems like a no-brainer for deal continuity. It locks in occupancy for the buyer and steady income for your HoldCo.

Yet, this seemingly benign two-year extension shifts dynamics from a shorter-term arm's-length arrangement to a mid-term commitment, amplifying exposures in a post-closing world governed by provincial commercial tenancy laws (e.g., Ontario's Commercial Tenancies Act) and federal CRA transfer pricing rules (ITA section 247). In volatile sectors like manufacturing or logistics, where 40% of deals tangle with real estate, those extra years can compound uncertainties. Below, we zero in on the incremental risks this extension introduces for buyers and sellers, plus targeted mitigations drawn from real-world lower middle market transactions.

Why the Extra Two Years Matter: A Quick Primer

In a share sale, the buyer inherits OpCo's market-rate lease obligations without disruption. The reset, via a closing-time amendment, extends the term while keeping rent, use rights, maintenance, and other terms unchanged. This avoids near-term renegotiation headaches but extends the horizon when business trajectories, market rents, or landlord-tenant relations could evolve. Provincial laws treat this as a binding contract on successors, so negotiation is key to layering in protections. For deals closing in 3–6 months, baking this into the SPA as a mutual condition prevents last-minute snags.Now, let's drill into the added risks: These aren't the everyday lease pitfalls but the unique bite from stretching to five years.

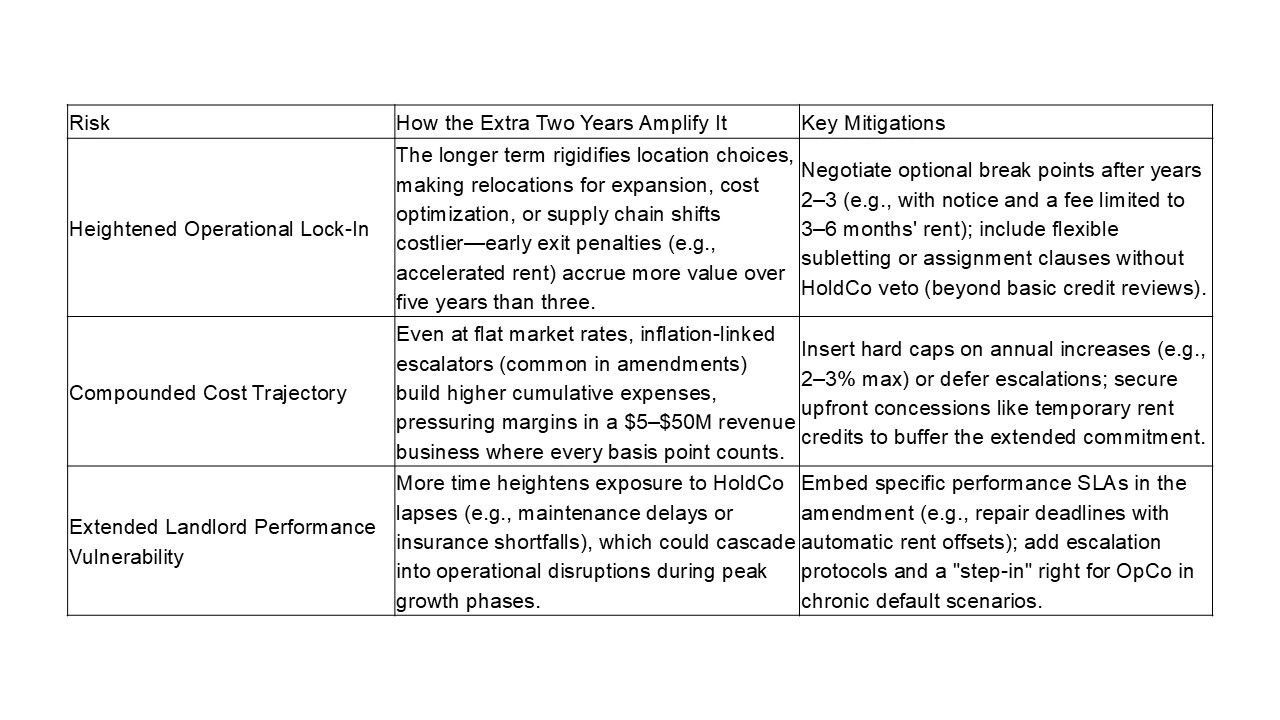

Incremental Risks for the Buyer: Locked In Longer, Exposed More

Buyers prize the extension for integration stability, but it tethers OpCo to the property amid potential pivots, inflating the stakes over those additional two years.

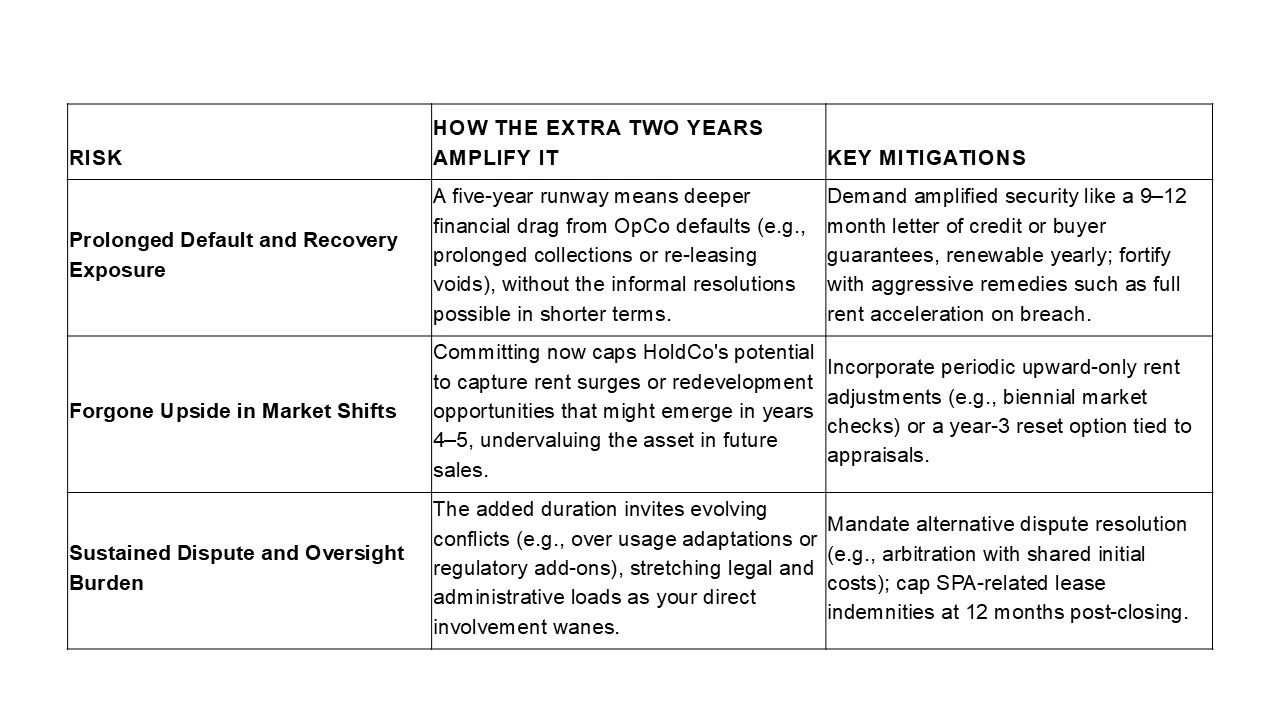

Incremental Risks for the Seller: Security at the Cost of Agility

For you as HoldCo owner, the extension wards off vacancy but prolongs ties to a buyer-controlled tenant, forgoing the reset window after three years.

In a rising-rate environment, these could quietly deflate HoldCo's standalone appeal—independent valuations at amendment signing provide a defensible baseline.

Steering Clear of the Traps: Actionable Strategies for Lower Middle Market Deals

Lower middle market M&A thrives on pragmatism, not perfection. To neutralize these extension-specific risks without derailing momentum:

- Valuation Lockdown: Commission a neutral appraiser jointly for the amendment terms, $5K–$15K well spent to bulletproof against CRA flags or haggling.

- SPA Integration: Tie the reset to closing with buyer/seller approvals; include a three-year fallback if consensus falters. Escrow 5–10% of proceeds for lease contingencies.

- Deal Structure Smarts: Favor share purchases for seamless inheritance, asset sales trigger consents that complicate extensions. Watch provincial nuances: Ontario's flexibility vs. BC's fairness scrutiny.

- Forward Modeling: Run sensitivity analyses on five-year scenarios during diligence; consider a four-year hybrid if two extra years feels too sticky.

- Expert Alignment: Engage cross-disciplinary advisors (M&A lawyers, tax specialists) from LOI onward. In this deal size, where real estate threads 40% of transactions, it's your edge.

The Bottom Line: Extend Wisely, or Risk the Overhang

Adding two years to a market-rate lease isn't inherently risky, it's a stability booster that polishes OpCo's handover. But in Canada's dynamic lower middle market, it subtly magnifies lock-in for buyers and opportunity costs for sellers. Handled with foresight, it fortifies value; overlooked, it festers into post-deal friction.

Disclaimer: Not legal or tax advice—always consult qualified professionals for your transaction.