MAXIMIZING YOUR EXIT: EARN-OUTS VS. REVERSE EARN-OUTS

Maximizing Your Exit: Earn-Outs vs. Reverse Earn-Outs for Canadian Business Owners Selling a $5M–$50M Revenue Company

As a Canadian entrepreneur who's built a $5 million to $50 million revenue business, you've weathered economic storms, scaled operations, and created real value—often in intangibles like customer loyalty or proprietary processes. But when it comes to selling, valuation gaps can stall deals: You see untapped potential; buyers want proof. Contingent structures like earn-outs and reverse earn-outs bridge this divide, tying payments to post-sale performance. Better yet, a seller-financed reverse earn-out can optimize taxes for you while keeping buyers cash-neutral on the upside portion.

In this guide, we'll unpack these tools from the Canada Revenue Agency (CRA) perspective, compare cash flows and trade-offs, and walk through a real-world example of the most tax-efficient setup for sellers that's funding-friendly for buyers. With no major CRA changes to these rules in 2024–2025 (beyond general inflation indexing like the 4% prescribed interest rate for Q1 2025), the strategies below remain robust. Always model with your tax advisor—these can save 20–30% on taxes while smoothing liquidity.

Earn-Outs: Pay for Performance, But Watch the Tax Trap

An earn-out pays a base price at closing, with bonuses if milestones (e.g., 15% revenue growth) are hit over 1–5 years. It's ideal for goodwill-heavy businesses like yours, where future earnings justify a premium.

CRA Treatment

Under the Income Tax Act (ITA), base proceeds qualify as capital gains (50% taxable), but earn-out payments risk full inclusion as business income via paragraph 12(1)(g)—taxed at marginal rates up to 53%. Relief comes via the "cost recovery method" in archived Interpretation Bulletin IT-426R (still guiding CRA audits):

- Applies to share sales (not assets): Treat payments as additional capital gains, reported when "determinable" (certain and payable).

- Requirements: Arm's-length deal, tied to unquantifiable goodwill, max 5 years, Canadian-resident seller.

- Defer tax with a capital gains reserve (up to 5 years). For asset sales (common in your range), payments are often fully taxable income—no reserve.

Buyers get gradual cost base increases for depreciation.

Reverse Earn-Outs: Upfront Confidence with Downside Protection

A reverse earn-out front-loads the full price (e.g., $20M), but you repay shortfalls if targets miss—via cash, set-off, or forgiveness. It's gaining popularity for clean exits in volatile sectors.

CRA Treatment

Full upfront amount is capital gains proceeds (50% taxable), assuming reasonable expectation of meeting targets at closing. Repayments create capital losses (3-year carryback or indefinite forward). No s. 12(1)(g) income risk, making it versatile for share or asset sales. A 2022 Tax Court ruling (Bouchard v. The King) clarified: True repayment obligations are key—not just a "cap.

"Buyers' cost base starts high, adjusts down on repayments (potential recapture risk).

Seller-Financed Reverse Earn-Outs: The Tax Win That's Cash-Neutral for Buyers

To make reverses buyer-friendly without upfront cash for the contingent slice, you "lend" it back via a promissory note (vendor take-back or VTB loan). Buyer pays base cash + issues a note for the rest; you forgive principal on shortfalls. This:

- Keeps CRA treatment as a reverse (capital gains upfront, losses on reductions).

- Adds interest income (taxable at marginal rates, but deductible for buyer).

- Ensures market terms (e.g., 5–7% interest to match 2025 prescribed rates and avoid imputed income under s. 80.4).

It's economically identical to a standard reverse but phases buyer outlays, ideal for PE buyers or family offices tight on capital.

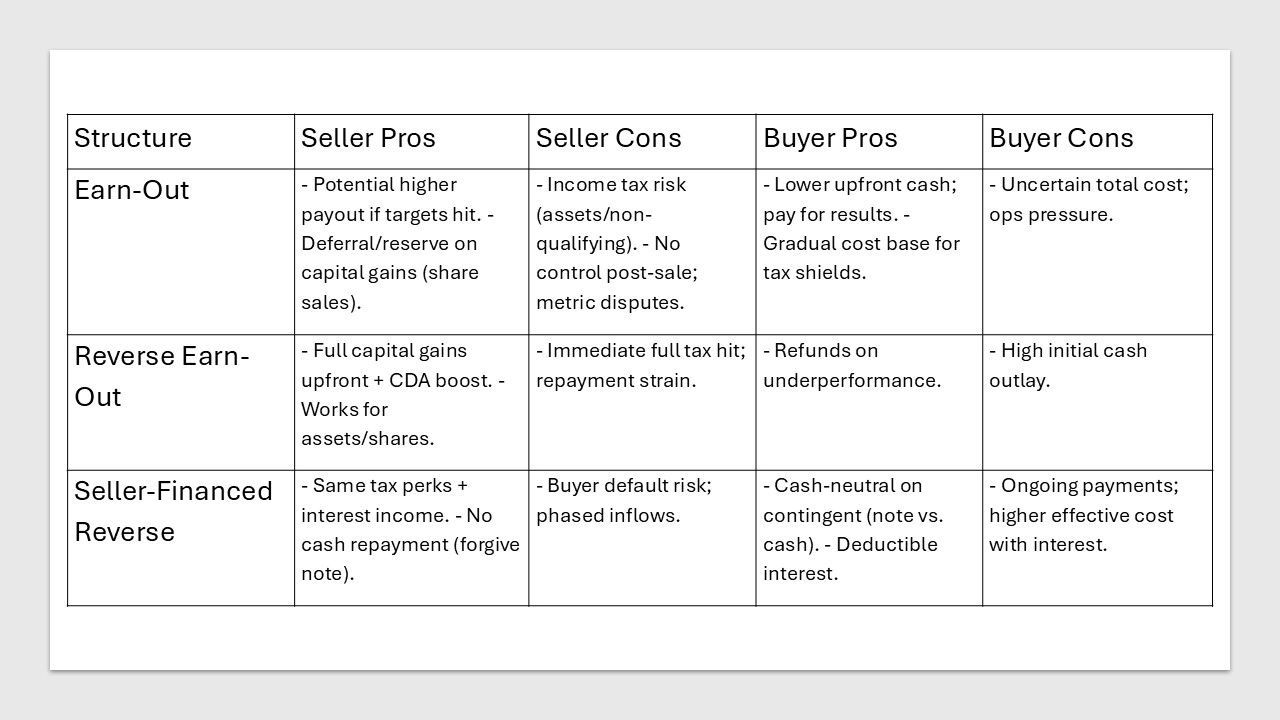

Pros, Cons, and Cash Flow: At a Glance

Advantages and Disadvantages

Tailored to your profile—assuming a share sale for max seller benefits.

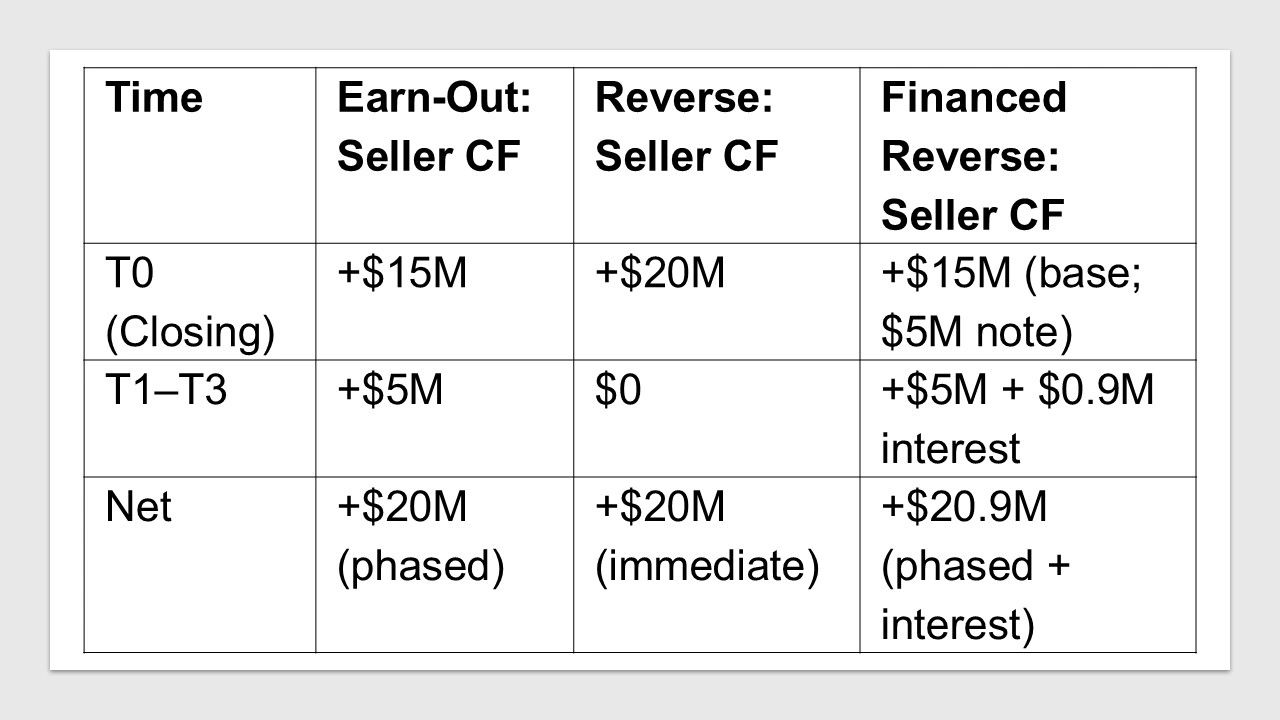

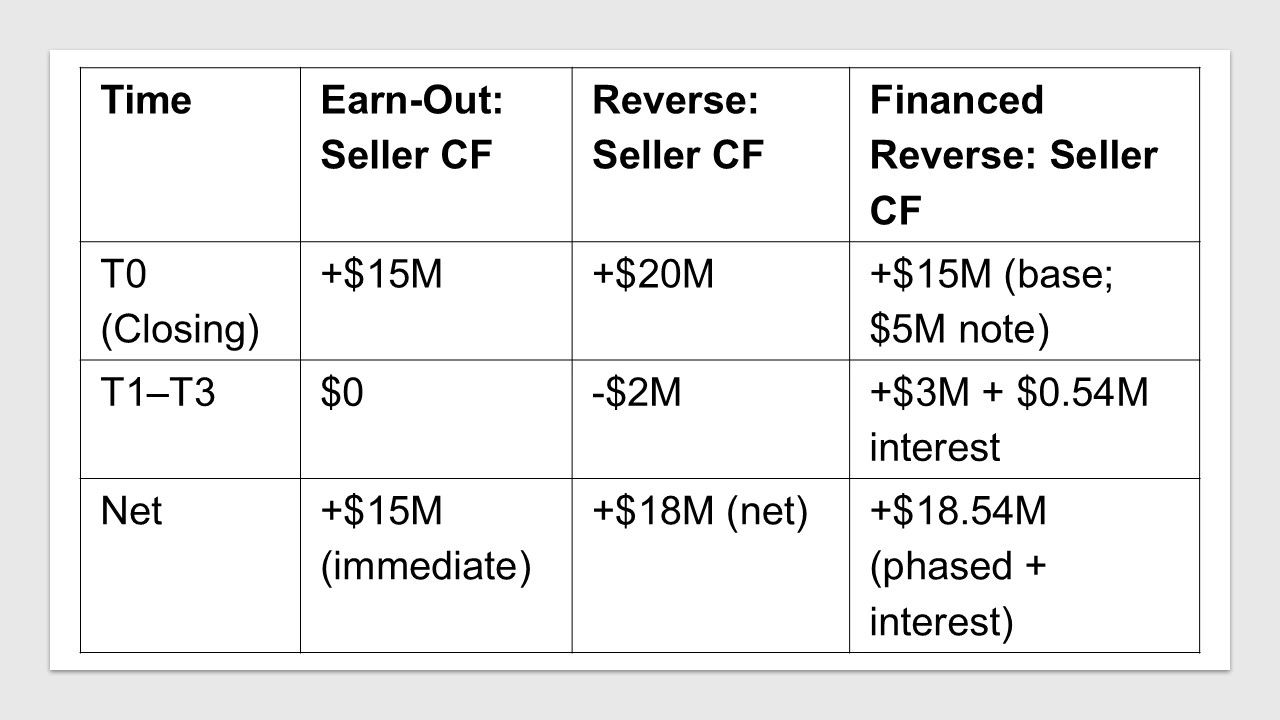

Cash Flow Comparison

Using a $20M deal ($15M base + $5M contingent, 1-year milestone). Seller view: + inflow, - outflow. Scenarios: Targets met (A) or missed by $2M (B). For financed reverse, assume 6% interest on $5M note over 3 years.

Scenario A: Targets Met

Scenario B: Targets Missed ($2M Shortfall)

Buyer Flip: Earn-out saves $5M upfront; standard reverse risks overpay; financed keeps T0 at $15M, with phased repayments.

Example: Implementing the Most Seller-Tax-Advantaged, Buyer-Cash-Neutral Exit

Meet Alex, owner of a $25M-revenue SaaS firm in Ontario (asset-heavy, but structured as shares for tax perks). Buyer (a PE fund) values at $18M base + $7M contingent on 20% EBITDA growth over 2 years. Alex wants capital gains treatment and quick liquidity; buyer needs cash neutrality for integration.

Step-by-Step: Seller-Financed Reverse Earn-Out Setup

1. Structure the Deal (Pre-LOI):

- Total price: $25M ($18M base cash + $7M contingent via note).

- Share sale to qualify for capital gains (50% inclusion; lifetime exemption up to $1M if QSBC).

- Milestones: Clear, auditable (e.g., audited EBITDA, no "gaming" clauses).

- Note: 3-year amortizing promissory at 6% interest (market rate; secures with assets). Forgiveness clause: Reduce principal by shortfall % (capped at $7M).

2. Closing (T0):

- Buyer pays $18M cash (from financing—neutral on contingent).

- Issues $7M note to Alex (FMV = face value).

- Alex reports $25M capital gain ($12.5M taxable; reserve unavailable due to contingency, but CDA swells for tax-free dividends).

- Tax hit: ~$5–6M (at 48% effective), but losses carry back 3 years if needed.

3. Post-Closing Monitoring:

- Alex stays as advisor (1-year contract) to align incentives.

- Independent accountant verifies metrics annually.

4. Outcomes:

- Targets Met: Buyer repays $7M + $1.26M interest over 3 years. Alex nets $26.26M total (phased liquidity for reinvestment; interest taxed as income but ~$0.6M net after 53% rate).

- Missed by $3M (43% Short): Forgive $3M on note; buyer pays $4M + prorated interest ($0.72M). Alex nets $22.72M (capital loss on $3M for carryback; offsets prior gains).

- Buyer Cash Flow: $18M T0 (same as earn-out base), then $7M/$4M phased—no upfront risk on upside.

Why Tax-Optimal for Alex? Full capital gains vs. earn-out's income risk; immediate CDA access. Vs. standard reverse: No repayment cash crunch. Savings: ~$1.5M in taxes (income vs. cap gains on $7M).

Why Cash-Neutral for Buyer? Contingent funded by note, not cash—preserves $7M for ops/debt service. Interest deductible, lowering effective cost.

Your Next Steps: Exit Smarter, Not Harder

For $5M–$50M deals, seller-financed reverses often edge out earn-outs: Superior tax treatment, flexibility, and alignment in uncertain times (e.g., post-2025 rate cuts). But they're not one-size-fits-all—asset sales may tilt to earn-outs, and disputes lurk in metrics.

Start by stress-testing with your M&A lawyer, accountant, and valuator. Tools like Excel models (sensitizing shortfalls/interest) reveal breakeven points. With CRA's 2025 audit enhancements, document "reasonable expectations" rigorously. Your legacy deserves an exit that funds the next chapter—structured right, these tools deliver. Ready to crunch numbers? Reach out to a specialist today.