SHARE PURCHASE AGREEMENT STRATEGIC CONSIDERATIONS

Share Purchase Agreement in a Canadian Business Sale: Strategic Considerations for Sellers and Their M&A Advisors

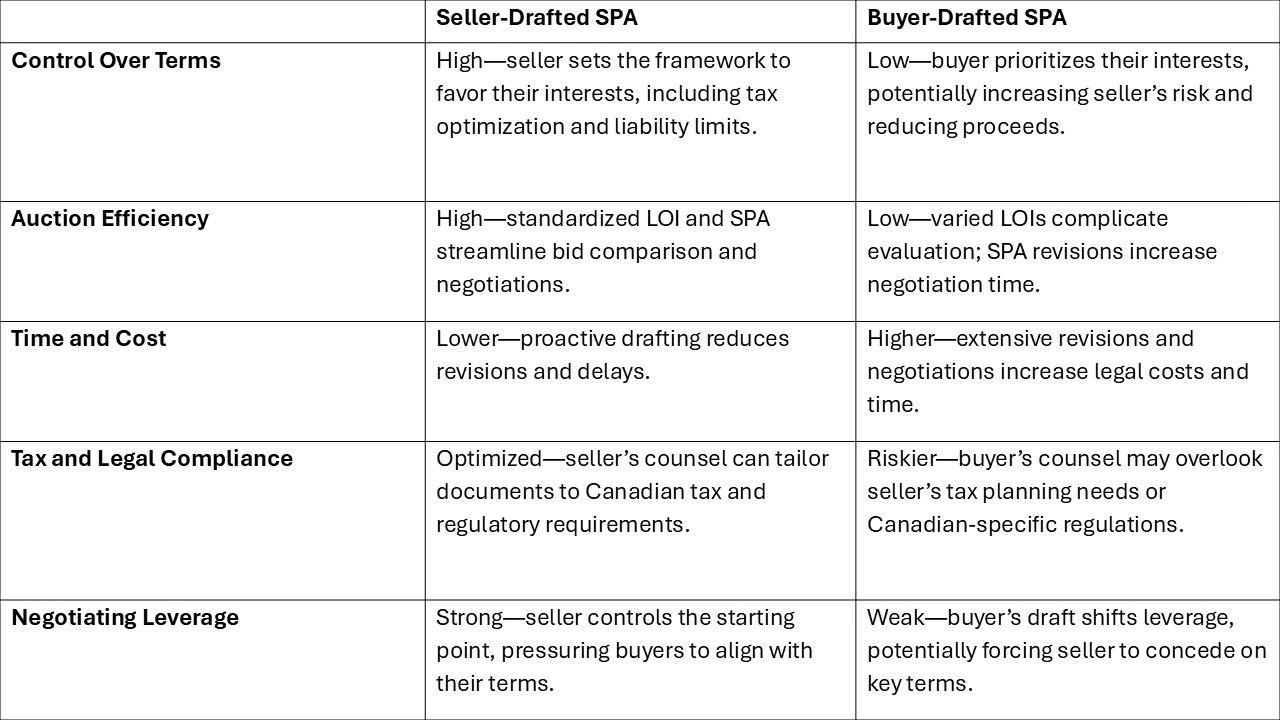

In a Canadian business share sale, the Share Purchase Agreement (SPA) is the cornerstone document that formalizes the transfer of shares from the seller to the buyer, detailing critical terms such as purchase price, representations and warranties, indemnities, conditions precedent, and post-closing obligations. The Letter of Intent (LOI), typically non-binding except for provisions like confidentiality or exclusivity, precedes the SPA and outlines key deal terms, serving as a framework for negotiations. In an auction process, where multiple suitors compete, a pivotal decision for sellers and their M&A advisors is whether to have their legal counsel draft the SPA and LOI or allow the buyer’s legal counsel to take the lead. This article examines the advantages of the seller drafting these documents as part of the auction process, particularly when shortlisted suitors submit their best and final LOI, contrasts this with allowing the buyer to draft the LOI and SPA, and highlights the strategic timing of introducing the SPA in a Canadian share sale.

The Role of the SPA and LOI in a Canadian Business Share Sale

The SPA governs the legal and financial mechanics of a share sale, ensuring compliance with Canadian laws, such as the *Canada Business Corporations Act* or provincial securities regulations, and addressing tax considerations under the *Income Tax Act*. The LOI sets the stage by outlining the proposed purchase price, deal structure, due diligence timelines, and exclusivity terms. In an auction, the seller solicits bids from multiple parties, shortlists suitors, and requests their “best and final” LOI before selecting a buyer for exclusive negotiations. The timing and control of drafting these documents significantly influence the transaction’s outcome.

Strategic Timing of the SPA in the Auction Process

In a well-orchestrated auction, the seller’s M&A advisors and legal team typically introduce a draft SPA ahead of granting exclusivity to a buyer. This draft is often made available through a virtual data room (VDR) well before the LOI is executed and before exclusivity is granted to the final party. By presenting the SPA early, the seller maintains control over the transaction’s framework during the competitive phase of the auction, when their leverage is at its peak. This approach contrasts with the buyer producing their own SPA after exclusivity is granted, at which point the leverage often shifts to the buyer due to the seller’s commitment to a single party.

Advantages of the Seller and Their M&A Advisors Drafting the SPA and LOI

When the seller’s legal counsel drafts the LOI and SPA, particularly by introducing the SPA via the VDR ahead of exclusivity, several advantages emerge:

1. Control Over Terms and Structure

By drafting the LOI and SPA, the seller can tailor terms to their advantage, such as:

- Limiting post-closing liabilities through narrow indemnities or capped representations and warranties.

- Structuring the deal to optimize tax outcomes, such as leveraging the lifetime capital gains exemption for qualifying small business corporations under the *Income Tax Act*.

- Setting clear timelines and conditions precedent that align with the seller’s goals, such as expedited due diligence or regulatory approvals under the *Competition Act* or *Investment Canada Act*.

Introducing the SPA early via the VDR ensures that shortlisted suitors review and respond to the seller’s preferred terms during the competitive bidding phase, preserving the seller’s leverage before exclusivity shifts the dynamic.

2. Streamlined Auction Process

A seller-drafted LOI template standardizes bids, enabling the seller and their M&A advisors to compare offers based on consistent terms, such as purchase price structure (e.g., cash vs. earn-outs) or exclusivity periods. Similarly, providing a draft SPA in the VDR allows suitors to assess the seller’s expectations upfront, reducing surprises and aligning bids with the seller’s framework. This clarity is critical in a Canadian context, where share sales involve complex tax and regulatory considerations.

3. Maximizing Leverage Pre-Exclusivity

By introducing the SPA before exclusivity, the seller capitalizes on the competitive tension among suitors. Shortlisted buyers, aware of rival bids, are incentivized to accept the seller’s SPA framework to remain competitive, rather than proposing significant changes that could weaken their position. This contrasts with the post-exclusivity phase, where the selected buyer, having secured exclusivity, may produce an SPA that prioritizes their interests, shifting leverage away from the seller.

4. Time and Cost Efficiency

Drafting the SPA early allows the seller to address potential issues—such as tax liabilities, employee obligations under Canadian employment law, or environmental concerns—before buyers conduct due diligence. This proactive approach minimizes revisions and delays, reducing legal costs. A seller-drafted SPA in the VDR also signals preparedness, encouraging suitors to move quickly and align with the seller’s terms.

5. Canadian-Specific Legal and Tax Optimization

A seller’s legal counsel, familiar with Canadian nuances, can craft an SPA that optimizes tax outcomes (e.g., structuring payments to defer tax liabilities) and ensures compliance with regulations like the *Investment Canada Act* for foreign buyers. Early introduction of the SPA allows these considerations to be embedded in the deal structure before exclusivity narrows the seller’s negotiating power.

Contrast: Allowing the Buyer’s Legal Counsel to Draft the LOI and SPA Post-Exclusivity

When the seller allows the buyer to draft the LOI and SPA, particularly after exclusivity is granted, several challenges arise:

1. Loss of Control and Leverage

Once exclusivity is granted, the buyer gains significant leverage, as the seller is committed to negotiating with a single party. A buyer-drafted SPA, typically produced post-exclusivity, prioritizes the buyer’s interests, potentially including:

- Broad indemnities or extended representations and warranties that increase the seller’s post-closing liabilities.

- A deal structure less favorable to the seller, such as an asset sale instead of a share sale, which may trigger adverse tax consequences under Canadian law.

- Buyer-friendly conditions, such as prolonged due diligence or financing contingencies, that delay closing.

For example, a buyer may propose a holdback or escrow for a portion of the purchase price, tying up the seller’s proceeds for years.

2. Inconsistent Bids in an Auction

Allowing suitors to submit their own LOIs during the auction results in varied terms, making it harder to compare bids. Post-exclusivity, a buyer-drafted SPA may introduce terms that deviate from the LOI, requiring extensive negotiations to realign with the seller’s goals.

3. Increased Negotiation Time and Costs

A buyer-drafted SPA often requires significant revisions to address the seller’s needs, leading to prolonged negotiations and higher legal costs. In Canada, where share sales involve complex tax and regulatory considerations, a buyer’s counsel may overlook seller-specific issues, necessitating costly rework.

4. Risk of Buyer-Driven Delay

Post-exclusivity, a buyer may use the drafting process to extend due diligence or introduce vague conditions precedent, giving them leverage to renegotiate terms or walk away. This is particularly risky in Canada, where regulatory approvals (e.g., *Investment Canada Act* reviews for foreign buyers) can already introduce delays.

5. Less Favorable Tax Outcomes

A buyer-drafted SPA may not account for the seller’s tax planning needs, such as eligibility for the capital gains exemption or deferral of tax liabilities. This could reduce the seller’s net proceeds compared to a seller-drafted SPA tailored for Canadian tax efficiency.

Comparing the Two Approaches in a Canadian Share Sale

Strategic Considerations for Sellers and M&A Advisors

In a Canadian business share sale, particularly in an auction, the seller and their M&A advisors should prioritize drafting the LOI and SPA, introducing the SPA via the VDR before exclusivity and well ahead of LOI execution. This approach offers:

1. Maximizing Value and Leverage

Introducing the SPA pre-exclusivity leverages the competitive auction environment, encouraging suitors to align with the seller’s terms to secure the deal. This maximizes the purchase price and minimizes concessions.

2. Mitigating Canadian-Specific Risks

Early drafting allows the seller to address Canadian tax and regulatory nuances, such as optimizing for the capital gains exemption or ensuring compliance with the *Investment Canada Act*, before leverage shifts to the buyer.

3. Maintaining Momentum

A seller-drafted SPA in the VDR keeps the transaction on track, reducing delays and signaling professionalism to suitors.

However, in limited scenarios, allowing the buyer to draft the LOI or SPA may be considered:

Single Buyer Negotiations: In a non-auction sale with a single buyer, the seller may allow a buyer-drafted LOI to gauge intent, provided their counsel rigorously negotiates terms.

Buyer-Specific Needs: If a buyer has unique regulatory or financing requirements (e.g., a foreign buyer subject to *Investment Canada Act* review), allowing them to propose certain terms post-exclusivity may facilitate the deal, though the seller should retain control over key provisions.

Conclusion

In a Canadian business share sale, having the seller’s legal counsel draft the LOI and SPA, and introducing the SPA via the VDR before exclusivity, offers significant advantages over allowing the buyer to draft these documents post-exclusivity. By controlling terms, leveraging the competitive auction phase, optimizing tax and regulatory outcomes, and minimizing delays, the seller maximizes value and mitigates risks. The early introduction of the SPA ensures the seller’s priorities are embedded in the deal structure before leverage shifts to the buyer. Sellers and their M&A advisors should collaborate with experienced Canadian legal counsel to craft documents that align with their strategic goals and navigate the complexities of Canadian corporate and tax law.

For further guidance on structuring a share sale or engaging M&A advisors in Canada, consult legal and financial professionals with expertise in the Canadian market.