THE FIVE-YEAR FALLACY

"I'll Just Run It Five More Years" Is Costing Canadian Business Owners Millions

A business owner recently learned his company had a 4x EBITDA valuation. His response? "Why would I sell for that? I can run this for another five years, make more money, and then just shut the doors."

On the surface, this logic seems sound. Four times earnings, collected over five years, equals twenty times earnings. Why take four when you could take twenty?

But this reasoning contains several compounding errors that, when properly analyzed, reveal why the "run it five more years" strategy almost always destroys value. Let's examine this through a concrete example of a hypothetical lower-middle-market Canadian manufacturing company.

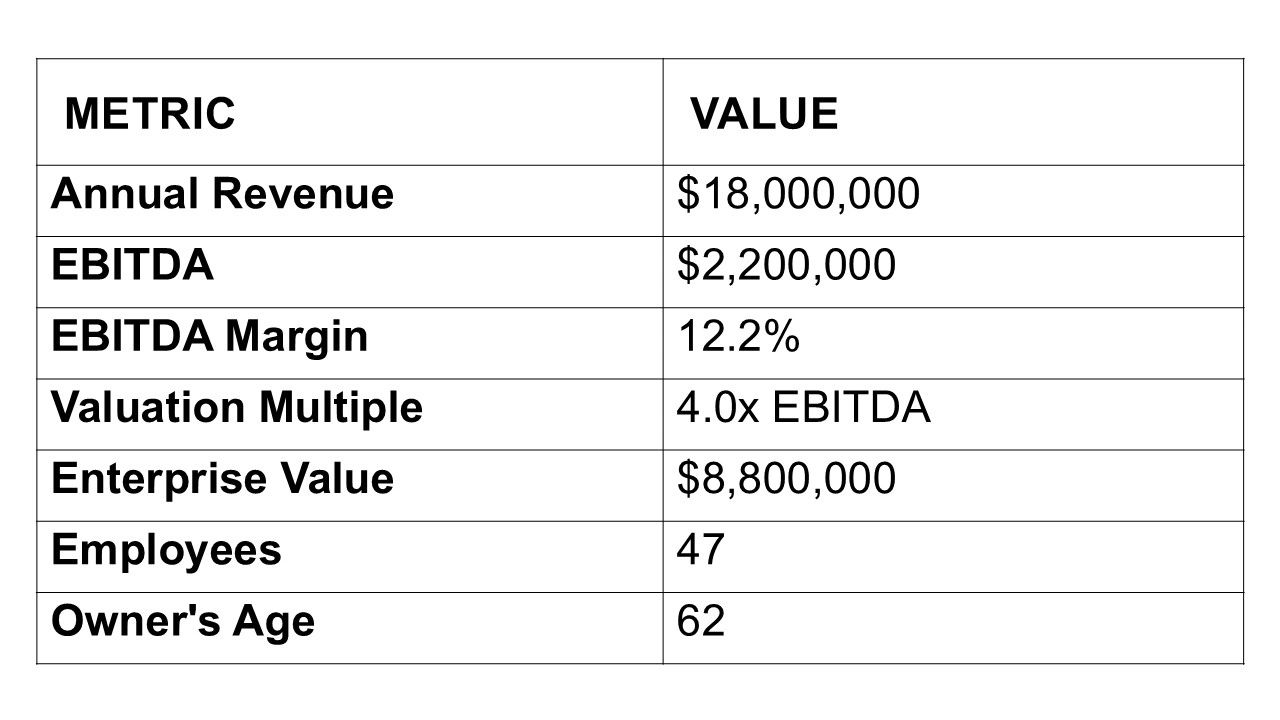

The Business: ACME Components of Canada Ltd.

Consider Margaret Chen, 62, sole owner of ACME Components of Canada Ltd, a precision machining company based in Toronto, Ontario. The business has the following characteristics:

Margaret's logic: "If I sell today, I get $8.8 million. If I run it for five more years at $2.2 million per year, I'll extract $11 million, and I get to keep my salary and benefits the whole time. Why would I take less?"

Let's examine why this reasoning fails.

Error #1: EBITDA Is Not Cash in Your Pocket

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. The key words are "before" - this is not the cash Margaret actually takes home. From that $2.2 million EBITDA, she must subtract:

Working capital requirements: Manufacturing businesses typically require 15-20% of revenue in working capital. With $18M revenue, that's roughly $2.7-3.6M tied up in inventory, receivables, and operations that can't be distributed.

Maintenance capital expenditures: CNC machines, tooling, and facility maintenance don't stop because Margaret wants to wind down. Figure $200,000-400,000 annually just to maintain current capacity.

Debt service: If the company carries any debt (common in manufacturing for equipment financing), principal and interest payments come out of operating cash flow.

Corporate taxes: Before dividends, the corporation pays tax. In Ontario, active business income above the $500,000 small business limit is taxed at a combined federal-provincial rate of approximately 26.5%.

Realistically, of that $2.2M EBITDA, Margaret might extract $1.0-1.2M annually in a combination of salary and dividends after all operating requirements are met.

Error #2: The Tax Treatment Is Dramatically Different

This is where the math decisively favors a sale.

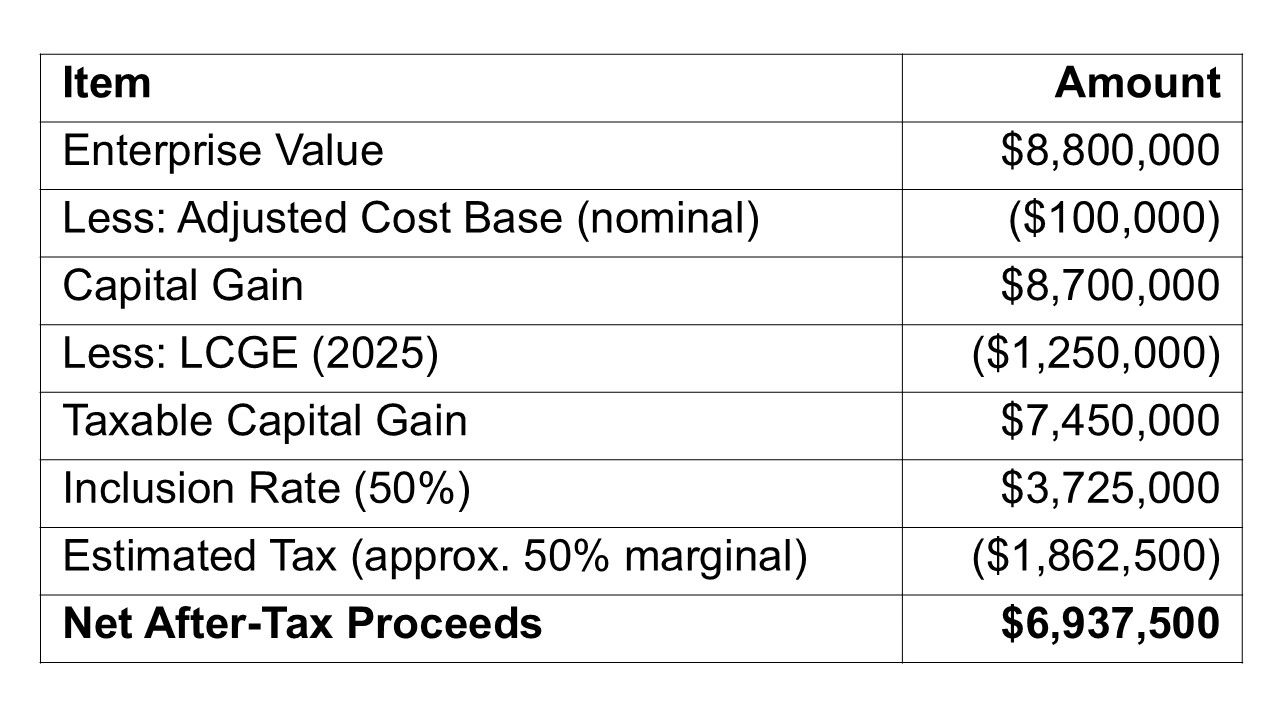

Scenario A: Sell Today

If Margaret sells her comapny as a qualifying share sale, she can access the Lifetime Capital Gains Exemption (LCGE). As of June 25, 2024, the LCGE limit increased to $1.25 million for qualified small business corporation shares, with indexation resuming in 2026.

Sale Proceeds Calculation:

Note: The capital gains inclusion rate remains at 50% for 2024-2025. The Government of Canada announced on March 21, 2025 that it does not intend to proceed with the proposed increase to 66.7%. Tax calculations are illustrative; consult a qualified tax professional for your specific situation.

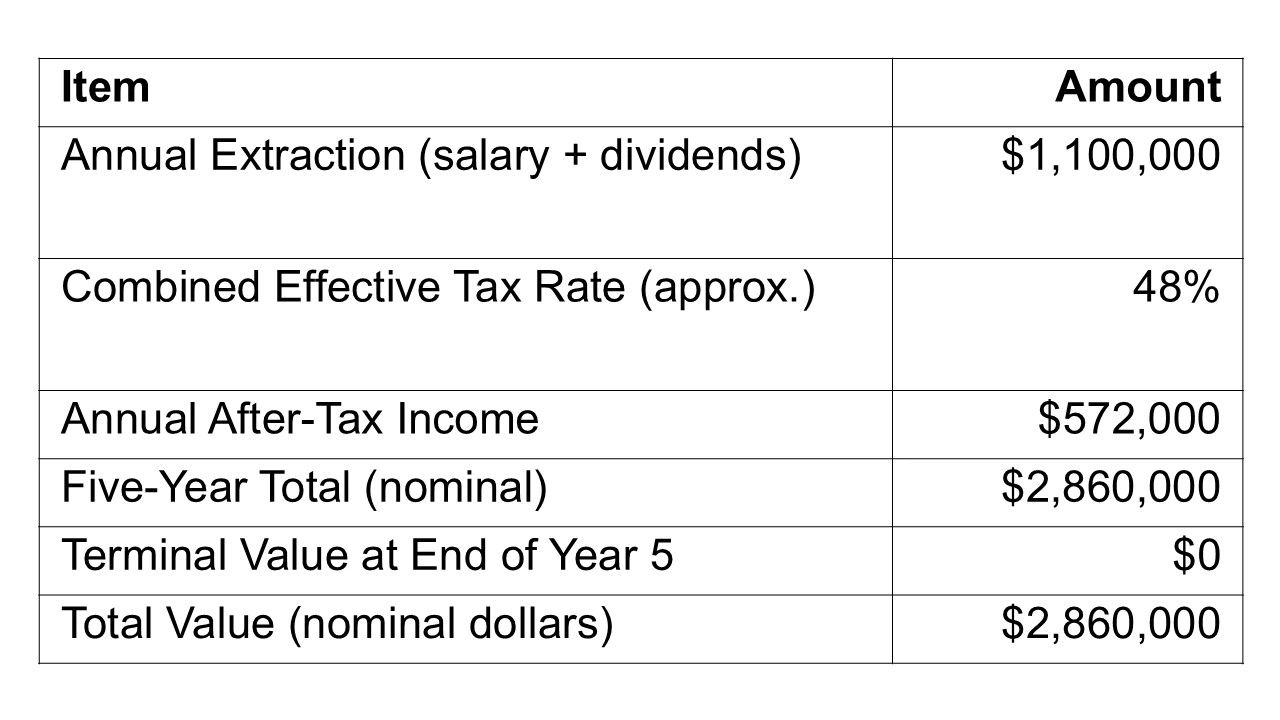

Scenario B: Run It Five More Years

If Margaret continues operating and extracts $1.1M annually through a combination of salary and dividends, she faces significantly different tax treatment:

Salary income: Taxed at her full marginal rate. In Ontario, combined federal-provincial rates reach 53.53% on income over $253,414.

Dividend income: Subject to corporate tax first, then personal tax on distribution. The integration principle is designed so combined rates approximate salary taxation, typically landing in the 45-50% range at high income levels.

Five-Year Extraction Calculation:

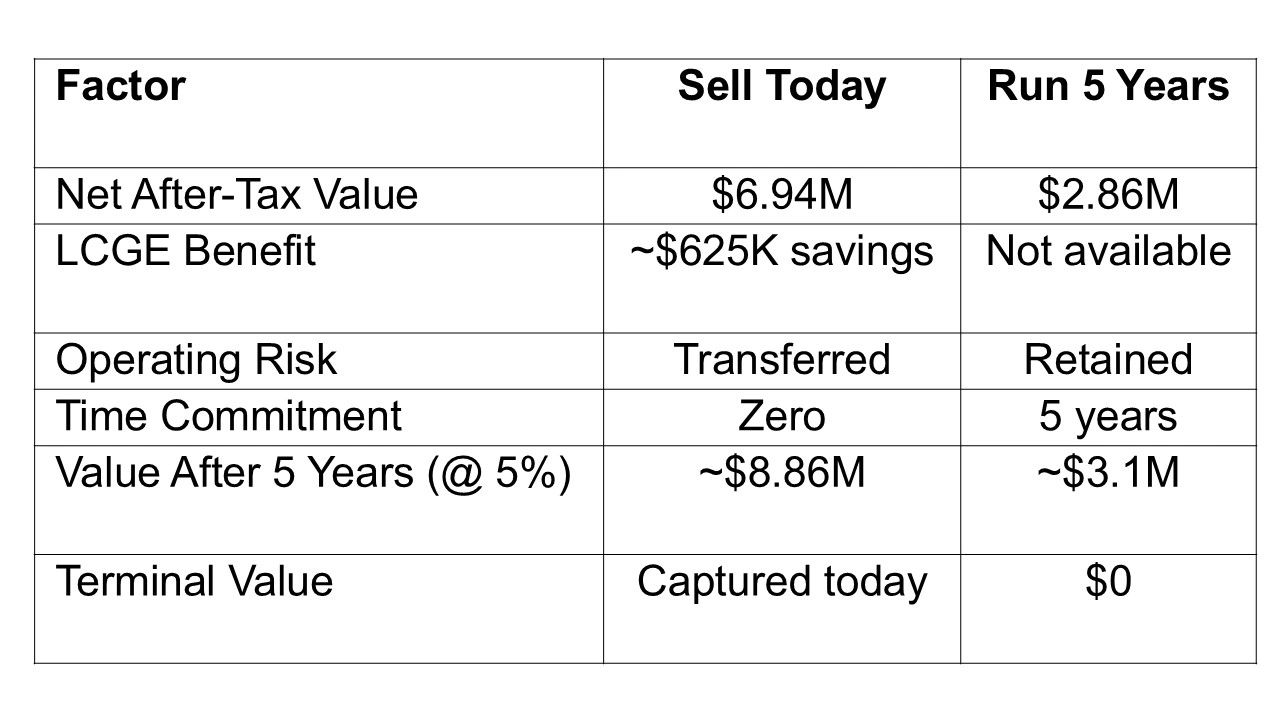

Even in nominal terms, Scenario B produces less than half of Scenario A. Margaret would receive $2.86M over five years versus $6.94M today.

Error #3: Time Value of Money

A dollar today is worth more than a dollar in five years. If Margaret sells today and invests the $6.94M net proceeds conservatively at 5% annually, she would have approximately $8.86M after five years - without lifting a finger.

Meanwhile, the $2.86M she extracts over five years in Scenario B has declining present value. Discounted at a modest 5% rate, the present value of that income stream is approximately $2.5M.

The gap widens further: $6.94M today versus a present value of $2.5M for the "run it longer" strategy.

Error #4: Five Years of Stable Earnings Is a Big Assumption

Margaret's calculation assumes EBITDA remains constant at $2.2M for five years. But businesses face constant threats:

Customer concentration: If her top three customers represent 40% of revenue (common in manufacturing), losing even one could devastate earnings.

Key person risk: Her shop foreman with 25 years of experience is 58. What happens if he retires or has health issues?

Competitive pressure: Offshore competition, technological changes, or a well-funded competitor could erode margins.

Owner health: Margaret herself is 62. What if she can't maintain her current pace?

Economic cycles: Manufacturing is cyclical. A recession could cut orders 20-40%.

The buyer paying 4x EBITDA today is essentially insuring Margaret against all these risks. They're taking the downside in exchange for upside potential she may not be positioned to capture.

Error #5: The Dividend "Tax Shelter" Misconception

Some owners believe they can shelter income by leaving profits in the corporation and paying themselves dividends at a lower rate. This reflects a misunderstanding of how Canadian tax integration works.

Canada's dividend gross-up and tax credit system is specifically designed so that the combined corporate plus personal tax burden is roughly equivalent whether income is taken as salary or dividends. The system "integrates" to prevent arbitrage.

For CCPCs earning active business income:

Income up to the small business limit (approximately $500,000) is taxed corporately at combined rates of 9-12.2% depending on province. When distributed as eligible dividends, the gross-up and dividend tax credit mechanism results in combined rates that approximate salary taxation at that income level.

Additionally, retaining earnings to invest passively inside the corporation triggers another problem: once passive investment income exceeds $50,000 annually, the small business deduction begins to phase out, increasing the corporate rate on active business income.

The dividend strategy may offer modest timing benefits, but it doesn't fundamentally change the comparison with a sale - it just optimizes around the edges of a structurally inferior outcome.

Error #6: Opportunity Cost of Owner's Time

Five more years of ownership means five more years of Margaret's personal involvement. What is that worth?

At 62, she's trading her peak earning years outside the business, her health, her ability to pursue other interests, and the stress of daily operations. Running a manufacturing company with 47 employees isn't passive income - it's demanding work.

If Margaret values her time at even $300,000 per year (a modest assumption for someone running an $18M company), that's $1.5M in opportunity cost over five years that doesn't appear in her calculation.

The Complete Comparison

Why Buyers Pay Multiples

The buyer isn't paying 4x EBITDA because they're foolish. They're paying for:

Future earnings: The right to capture profits for years 6, 7, 8 and beyond that Margaret won't be around to collect.

Synergies: Operational improvements, cost savings, or revenue opportunities the buyer can capture that Margaret cannot.

Growth potential: Investment capacity Margaret may lack to expand the business.

Risk tolerance: The buyer can absorb setbacks that might devastate a sole owner dependent on the business for retirement.

Margaret's "run it five more years" strategy isn't clever financial engineering. It's leaving millions of dollars on the table while taking on years of risk and effort.

The Right Question

Instead of asking "Why would I sell for 4x?" Margaret should be asking "What would I have to believe about the future to make running this business for five more years the better choice?"

The answer would require: perfectly stable earnings, no health issues, no key person departures, no competitive threats, no economic downturns, and a willingness to work another five years at an intensity level that most 62-year-olds don't want to maintain.

That's a lot to bet on. The math says sell.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws are complex and subject to change. All examples are illustrative and simplified; actual results will vary based on individual circumstances. Consult qualified tax and legal professionals before making any business transition decisions.

Sources and References

Capital Gains and LCGE:

• Canada Revenue Agency, "Capital Gains - 2024": canada.ca/capital-gains

• Canada Revenue Agency, "Line 25400 - Capital Gains Deduction": canada.ca/line-25400

• CFIB, "Lifetime Capital Gains Exemption": cfib-fcei.ca/lcge

Corporate Tax Rates:

• Canada Revenue Agency, "Corporation Tax Rates": canada.ca/corporation-tax-rates

• KPMG Canada, "Canadian Corporate Tax Tables": kpmg.com/ca/corporate-tax-tables

• TaxTips.ca, "2025 Corporate Income Tax Rates": taxtips.ca/corporate-tax-rates-2025

Personal Tax Rates:

• TaxTips.ca, "Ontario 2025 & 2026 Tax Rates": taxtips.ca/taxrates/on

• TaxTips.ca, "Canada's 2025 Federal Tax Rates": taxtips.ca/taxrates/canada

• PWC, "Canada - Individual - Taxes on Personal Income": taxsummaries.pwc.com/canada/individual