GEOPOLITICAL RISKS: DUE DILIGENCE FOR CANADIAN SELLERS

A guide for business owners preparing for exit in the $5 million to $50 million revenue range

If you are a Canadian business owner considering a sale to a private equity buyer, understanding what happens before a bid is submitted can mean the difference between a successful transaction and months of wasted effort.

This guide examines the qualitative attributes PE firms assess during due diligence and the increasingly critical dimension of geopolitical and regulatory risk that Canadian sellers must understand in 2026.

For businesses generating $5 million to $50 million in annual revenue — Canada’s lower middle market — these considerations are particularly important. PE buyers apply rigorous evaluation frameworks before committing capital.

Part 1: Qualitative Due Diligence — What PE Buyers Assess Before Bidding

Private equity firms are disciplined investors. According to industry research, the average PE firm evaluates approximately 80 opportunities for every single investment. Understanding what they look for can help you prepare your business to meet or exceed their expectations.

1. Management Team Quality and Depth

This is often the single most important factor in a PE buyer’s evaluation. They are not just buying your business — they are buying the team that will run and grow it after the transaction closes.

What PE firms evaluate:

• Leadership experience and track record

• Depth of the management bench beyond the founder or owner

• Willingness and ability of key executives to stay after acquisition

• Succession planning and key-person risk mitigation

• Management’s ability to operate independently without the current owner

Seller tip: If the owner is the business — holding all key relationships, making all decisions and driving all sales — that represents significant key-person risk that will concern PE buyers and may negatively affect valuation.

2. Customer Concentration and Relationships

What PE firms evaluate:

• Revenue distribution across the customer base (red flag: any single customer exceeding 10% to 15% of revenue)

• Length and quality of customer relationships

• Contractual versus transactional revenue mix

• Customer switching costs and barriers to exit

• Transferability of relationships after acquisition

Customer diligence is often the most revealing part of PE due diligence. Buyers will analyze revenue by customer, including top customers as a percentage of revenue, concentration trends, contract terms and renewal dates, customer tenure and churn rates, and expansion revenue within existing accounts.

3. Competitive Position and Market Dynamics

What PE firms evaluate:

• Defensibility of market position and barriers to entry

• Differentiation from competitors

• Industry growth trajectory and market size

• Fragmentation of the market (consolidation or buy-and-build opportunity)

• Regulatory environment and emerging risks

PE firms often look for problem areas they can fix to add value, such as an underperforming sales function or operational inefficiencies. A savvy deal team will meet with managers, visit suppliers and interview customers to uncover opportunities not visible in the confidential information memorandum.

4. Revenue Quality and Predictability

What PE firms evaluate:

• Recurring versus one-time revenue mix

• Contract terms, renewal rates and customer churn

• Visibility into future revenue (backlog, pipeline quality)

• Seasonality and cyclicality exposure

• Pricing power and margin sustainability

Revenue quality issues that concern PE buyers include one-time project revenue that will not recur, revenue pulled forward from future periods, revenue from customers who subsequently churned and unsustainable pricing that will face pressure after acquisition.

5. Operational Infrastructure and Scalability

What PE firms evaluate:

• Systems and processes (ERP, CRM, financial reporting quality)

• Operational efficiency and capacity utilization

• Supply chain resilience and vendor relationships

• Technology infrastructure and technical debt

• Ability to scale without proportional cost increases

6. Employee and Organizational Factors

What PE firms evaluate:

• Employee tenure and turnover rates

• Compensation competitiveness and workplace culture

• Union relationships (if applicable)

• Training programs and knowledge documentation

• Organizational structure clarity and reporting lines

7. Legal, Regulatory and ESG Considerations

What PE firms evaluate:

• Litigation history and pending claims

• Regulatory compliance (environmental, labor, industry-specific)

• Intellectual property ownership and protection

• Contract assignability and change-of-control provisions

• ESG factors (increasingly relevant to institutional limited partners)

8. Growth Potential and Value Creation Levers

What PE firms evaluate:

• Organic growth opportunities (geographic expansion, new products, pricing optimization)

• Add-on acquisition targets for buy-and-build strategies

• Operational improvement and margin expansion opportunities

• Technology or digital transformation potential

• Exit pathway clarity (strategic buyers, secondary PE sale, potential IPO)

Part 2: Geopolitical and Regulatory Risk in Canadian M&A

Beyond traditional qualitative due diligence, 2026 brings an increasingly critical dimension that sellers and buyers must understand: Canada’s dramatically strengthened foreign investment review regime under the Investment Canada Act.

Even if you are selling to a Canadian PE firm, this matters. Your buyer’s exit strategy may involve foreign acquirers, and sector-specific risks could affect your company’s valuation and deal timeline.

The New Regulatory Reality

In March 2025, the federal government significantly expanded the grounds for national security reviews of foreign investments. For the first time, economic security is now explicitly recognized as a factor in determining whether an investment poses a threat to Canada’s national security.

Key statistics underscore the enforcement shift: In the past three fiscal years, approximately 50% of national security reviews have resulted in transactions being blocked, unwound via divestiture or abandoned by the investor. This represents a dramatic increase from historical patterns.

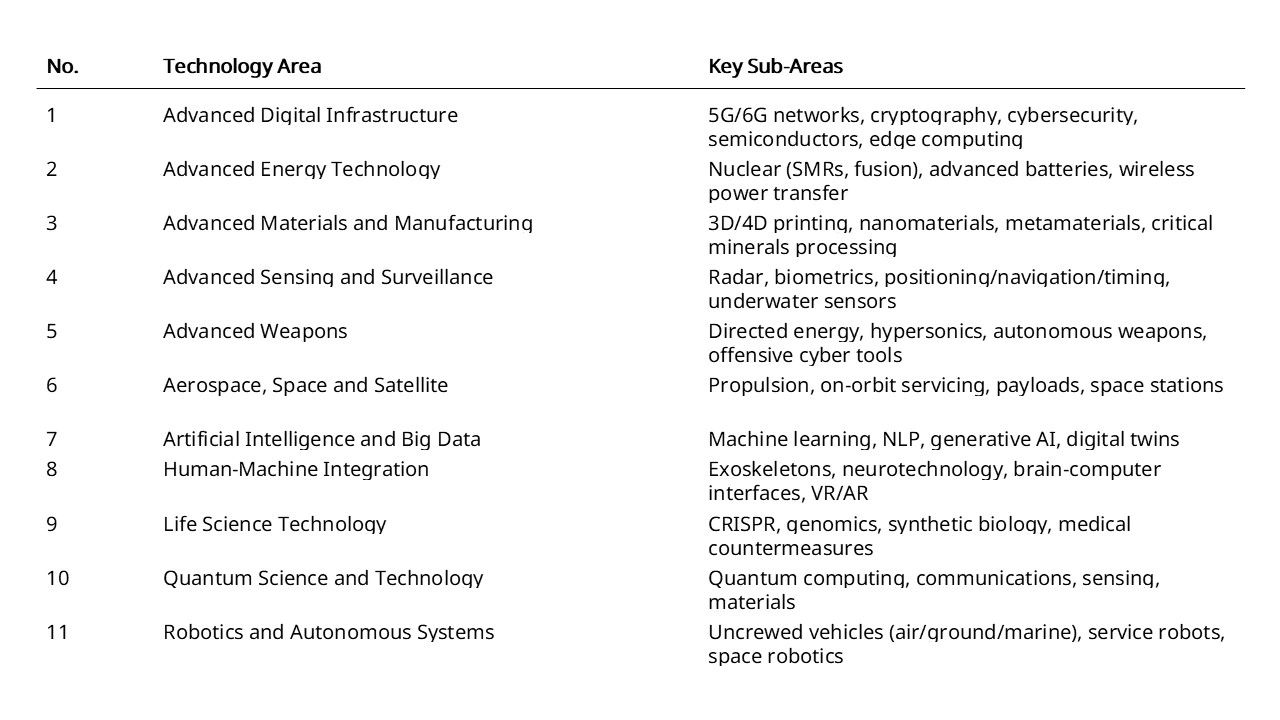

Canada’s 11 Sensitive Technology Areas

In February 2025, the federal government published its official Sensitive Technology List, identifying 11 broad technology areas that receive enhanced scrutiny in foreign investment reviews. If your business operates in any of these areas, both you and your potential buyers need to understand the implications:

The list covers technologies at various stages of development, from mature commercialized applications to emerging research. Even legacy technology that is still in use can trigger enhanced review.

Critical Minerals: A Virtual Prohibition for Certain Investors

Canada has taken an exceptionally firm stance on foreign state-owned enterprise investment in critical minerals. The policy states that SOE participation in any investment involving a Canadian business in the critical minerals sector will support a finding by the minister that there are reasonable grounds to believe the investment could be injurious to Canada’s national security.

This applies regardless of:

• Investment value (even minority stakes)

• Whether direct or indirect

• Whether controlling or noncontrolling

• Stage in the value chain (exploration, development, processing, refining)

Canada’s Critical Minerals List includes 31 minerals: lithium, cobalt, nickel, graphite, rare earth elements, uranium, copper and others essential for batteries, electric vehicles, defense and high-technology manufacturing.

Recent Enforcement Actions: A Warning for Sellers

The federal government has demonstrated its willingness to take decisive action, even retroactively:

• November 2022: Three Chinese investments in Canadian lithium companies ordered divested, including companies with mining operations outside Canada

• May 2024: Bluvec Technologies (anti-drone) and Pegauni Technology (wireless) ordered to wind up Canadian operations

• November 2024: TikTok Technology Canada ordered to wind up Canadian business

• June 2025: Hikvision Canada ordered to cease all operations, nearly 10 years after the company began operating in Canada

Critical insight: National security reviews can be initiated for investments implemented several years prior. The Hikvision order came nearly a decade after the company first incorporated in Canada.

Even U.S. Investors Now Face Scrutiny

Historically, investment from the United States was viewed as safe and largely exempt from the enhanced scrutiny applied to investments from countries like China and Russia. That has changed.

The 2023-24 Investment Canada Act Annual Report confirmed that, for the first time, a U.S. investment was subject to a national security review, which ultimately led to the investor withdrawing. In the current trade environment, economic security concerns now cast a shadow across all foreign investment, including from traditional allies.

Coming in 2026: Mandatory Pre-Closing Notification

New regulations expected to come into force in 2026 will require mandatory pre-closing notification for investments in certain sensitive sectors, regardless of investor nationality and whether the investment is controlling or minority.

This means transactions that previously could close without government review will now require advance filing and potential waiting periods.

Part 3: Practical Implications for Canadian Business Owners

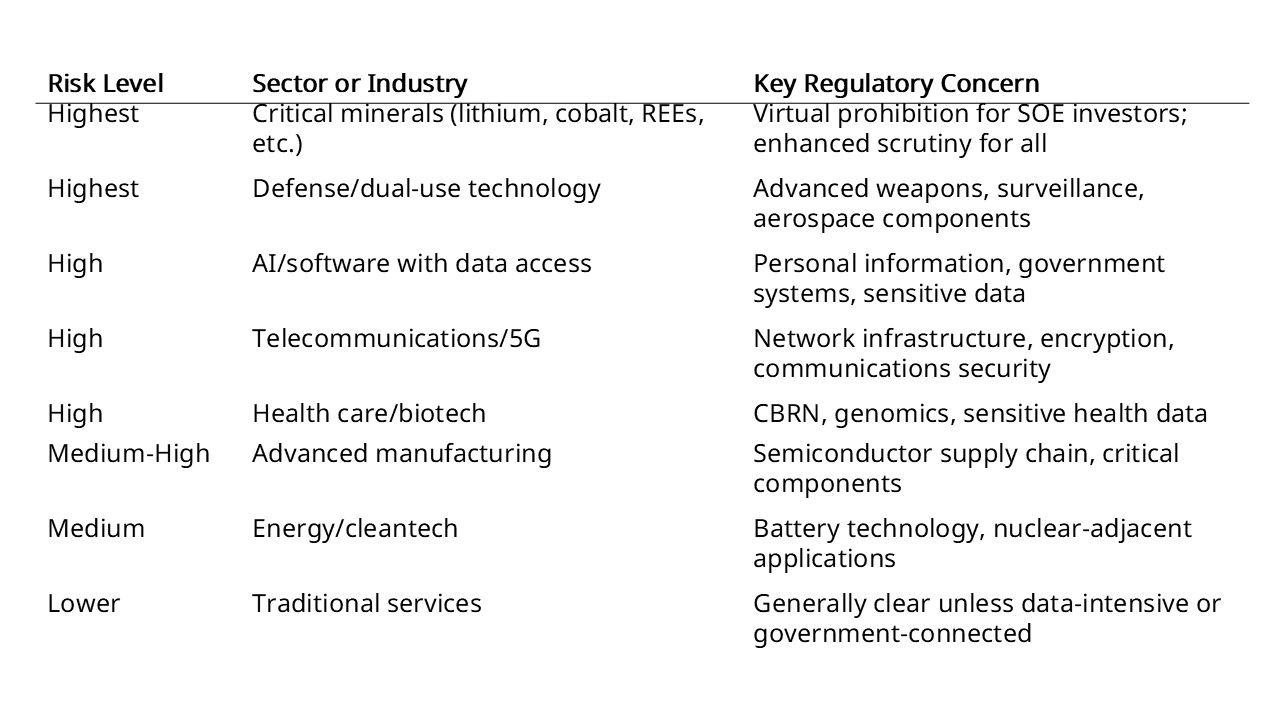

Sector Risk Assessment for M&A

Understanding where your business sits on the regulatory risk spectrum helps you anticipate due diligence questions and manage buyer expectations:

Key Due Diligence Questions You Should Prepare For

Sophisticated PE buyers will assess your business for geopolitical and regulatory risk. Be prepared to address:

1. Technology exposure: Does your business use, develop or have access to any of the 11 sensitive technology areas?

2. Critical minerals nexus: Any involvement in the 31 critical minerals value chain?

3. Government contracts: Any contracts with federal or provincial governments or security/defense agencies?

4. Data access: Does your business collect or store sensitive personal data on Canadians?

5. Supply chain integration: Would an acquisition integrate the business more deeply with a foreign economy?

6. Customer geography: Significant revenue from countries of concern (China, Russia, Iran)?

7. Ownership structure: Any existing foreign ownership or state-owned enterprise connections?

How Geopolitical Risk Affects Valuation and Deal Structure

For businesses in sensitive sectors, geopolitical risk can affect your transaction in several ways:

• Limited buyer universe: Foreign buyers from certain jurisdictions may be effectively excluded, reducing competitive tension

• Extended timelines: National security reviews can add more than 200 days to transaction closing if all stages run their maximum duration

• Conditionality risk: Buyers may require regulatory approval conditions that create uncertainty

• Exit pathway constraints: PE buyers will factor in limitations on their future exit options when determining valuation

• Undertaking requirements: Transactions may only be approved subject to binding conditions that affect operations

Preparing Your Business for Sale: Key Takeaways

Whether you are planning to sell in the next 12 months or the next five years, understanding both qualitative due diligence factors and geopolitical risk helps you build a more valuable, more saleable business.

For qualitative factors:

• Build management depth beyond the founder

• Diversify customer concentration

• Invest in systems, processes and documentation

• Strengthen recurring revenue streams

• Consider a sell-side quality of earnings report to de-risk the transaction for buyers

For geopolitical and regulatory risk:

• Assess your business against the 11 sensitive technology areas

• Understand how your sector is viewed by regulators

• Evaluate customer and supplier geography for concentration risk

• Consider how regulatory constraints may affect your buyer universe and exit options

• Work with advisors who understand both M&A execution and the regulatory landscape

Sources and Further Reading

• Government of Canada, Sensitive Technology List: canada.ca/en/services/defence/nationalsecurity/sensitive-technology-list.html

• Investment Canada Act, National Security Guidelines: ised-isde.canada.ca/site/investment-canada-act/en/investment-canada-act/guidelines/guidelines-national-security-review-investments

• Critical Minerals Policy: ised-isde.canada.ca/site/investment-canada-act/en/policy-regarding-foreign-investments-state-owned-enterprises-critical-minerals-under-investment

• ICA National Security Decisions: ised-isde.canada.ca/site/investment-canada-act/en/national-security-decisions

• Canada’s Critical Minerals Strategy: canada.ca/en/campaign/critical-minerals-in-canada/canadian-critical-minerals-strategy.html

Disclaimer: This article is for informational purposes only and does not constitute legal, tax or investment advice. Regulatory requirements and government policies are subject to change. Business owners considering a transaction should consult with qualified legal and financial advisors regarding their specific circumstances.