THE NEGOTIATING SECRET CANADIAN SELLERS MISS

Why the ability to walk away credibly is the single most important source of leverage in a business sale, and why most owners surrender it before negotiations even begin.

This is article 1 of 8 in a series examining the foundational negotiating strategies documented by academic and practitioner research — and comparing, for each strategy, the relative strengths and weaknesses of owner-direct versus advisor-led negotiation in Canadian lower-middle-market business sales. Each article draws on peer-reviewed research, transaction data and more than 30 years of Canadian M&A advisory experience.

What BATNA is; and why it matters more than the asking price

There is a concept in negotiation theory that, once understood, changes how you read every deal you will ever be part of. It is called BATNA; Best Alternative to a Negotiated Agreement , and it was introduced to the world in 1981 by Roger Fisher and William Ury in their landmark work Getting to Yes, published through Harvard's Program on Negotiation.

The core idea is straightforward: your negotiating power in any discussion is not primarily determined by your asking price, your legal team or even the quality of your business. It is determined by how good your alternatives are if the negotiation fails. The party with the strongest BATNA, the best option available if no deal is reached, holds the most leverage. The party with the weakest BATNA is, structurally, the most desperate.

This matters enormously in the sale of a Canadian business, because for most owners, the gap between their perceived BATNA and their actual BATNA is wide, consequential and almost entirely invisible to them until it is too late.

In a business sale context, your BATNA is the best outcome you can achieve without this specific buyer. It might be continuing to operate the business. It might be a competing offer from another buyer. It might be an internal management buyout, a recapitalization or a structured wind-down. Whatever it is, the buyer across the table will spend considerable energy trying to assess it, and trying to weaken it.

The critical insight is this: a strong BATNA does not just give you a better alternative if negotiations fail. It changes the entire dynamic of the negotiation while it is happening. When you can credibly walk away, buyers move. They improve their offers, sharpen their timelines and become more flexible on structure. When you cannot credibly walk away, when the buyer correctly perceives that you have no real alternative, the leverage equation inverts, and it does not invert in your favour.

The Canadian lower-middle-market reality

Canada's lower-middle market, businesses with $5 million to $50 million in annual revenue, presents a specific BATNA challenge that is often underappreciated by owners planning a sale.

The pool of qualified buyers for any given business in this market segment is finite. It is not the deep, liquid market of large-cap transactions where dozens of well-capitalized acquirers compete actively. In the lower-middle market, the realistic universe of buyers for a given business might be 15 to 40 qualified parties, depending on the sector, geography, financial profile and the seller's personal transaction objectives. If only three or four of those parties are contacted, and the owner negotiates with a single buyer at a time, the structural BATNA is already compromised before the first conversation occurs.

This reality is compounded by what Pepperdine University's Private Capital Markets Report consistently identifies as the defining feature of this market segment: information asymmetry. Buyers in this market, particularly private equity sponsors, family offices and experienced strategic acquirers, negotiate acquisitions regularly, sometimes dozens of times per year. The typical business owner negotiates a business sale once or twice in a lifetime. That experience gap is a form of BATNA advantage the buyer brings to every table, every time.

An estimated 75 per cent of Canadian small and medium-sized businesses are expected to change hands over the next 10 years as the baby boomer generation exits. This wave of supply means that patient, well-capitalized buyers increasingly face a buyers' market in the lower-middle segment, unless sellers take deliberate steps to create competitive tension through process design.

RESEARCH NOTE: Pepperdine University's Private Capital Markets Report (2024) documents that seller-side advisory representation is associated with significantly higher acquisition premiums in information-asymmetric markets — a category that precisely describes the Canadian lower-middle market. The research attributes this premium to three factors: competitive process management, information control and negotiating experience. All three are BATNA-strengthening mechanisms. Source: bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

When the owner negotiates directly: the BATNA problem

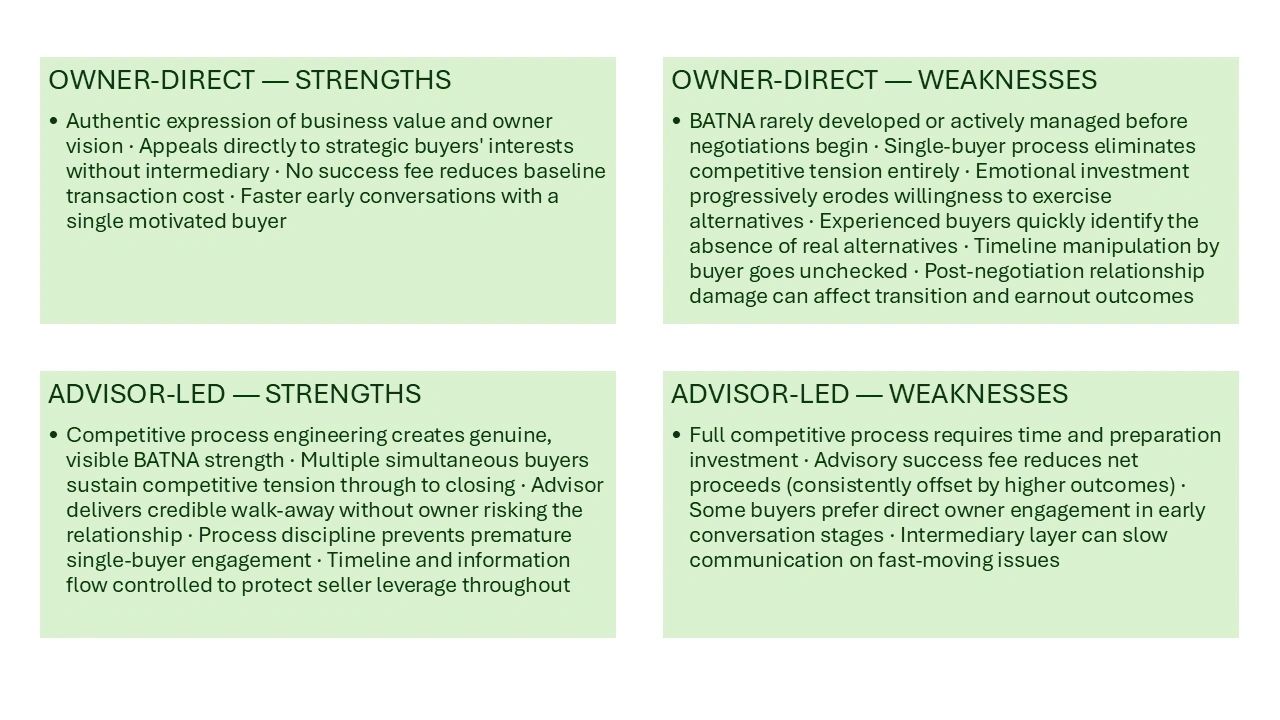

The appeal of negotiating directly is understandable. An owner who has spent 20 years building a business reasonably believes they know it better than anyone. They know the customers, the margins, the competitive landscape and the strategic value the business offers a prospective buyer. Why, the reasoning goes, would they pay an advisor to explain their own business to a buyer?

The answer lies not in explaining the business — but in managing the negotiating architecture around it.

The single-buyer trap

The most common BATNA-destruction pattern in owner-direct negotiations is what we might call the single-buyer trap. An owner receives an unsolicited approach from a buyer — often a competitor, a private equity firm that has acquired a portfolio company in their sector or a strategic acquirer making a quiet offer through a mutual contact. The conversation feels positive. The buyer expresses enthusiasm. An informal valuation discussion begins.

At this point, the owner is already in a structurally weak position, even if the buyer's initial indication of value feels attractive. The owner has one buyer. The buyer knows they have one buyer. The BATNA on both sides of the table is now clearly defined: the owner's alternative is to continue operating; the buyer's alternative is to approach another target. In most cases, the buyer's alternative is stronger — they have optionality across multiple potential acquisitions while the owner has none.

Research by Deepak Malhotra and Max Bazerman at Harvard Business School documents that negotiators in this position consistently underperform those with genuine alternatives — not because they make irrational decisions, but because the structural reality of their position limits what rational decisions are available to them.

The emotional BATNA problem

There is a second, subtler BATNA problem in owner-direct negotiations: emotional compromise. After months of direct engagement with a buyer — shared management presentations, due diligence conversations, early relationship development — the psychological cost of walking away from a deal in progress is genuinely high. The owner has invested time, emotional energy and, frequently, the beginning of a personal relationship with the buyer's team.

Buyers understand this, and experienced acquirers use the passage of time deliberately. Extended due diligence timelines, slow responses to term sheet negotiations and late-stage requests for additional information are not administrative delays — they are tactics that increase the owner's psychological investment in closure and simultaneously weaken their willingness to exercise their BATNA. The owner who began negotiations prepared to walk away if terms were not right has, six months later, become the party most motivated to complete the transaction on whatever terms are available.

Malhotra and Bazerman identify emotional investment in an outcome as one of the primary causes of poor negotiating results. Negotiators with high emotional attachment to completing a deal make systematically worse decisions — conceding earlier, accepting worse terms and failing to exercise valid alternatives.

What owner-direct negotiation does well

In the interest of balance: there are genuine strengths to owner-direct negotiation in specific circumstances. An owner who is naturally disciplined, emotionally detached and has genuinely attractive alternatives can negotiate effectively — and some buyers, particularly family offices and owner-operators acquiring strategically, prefer the directness and authenticity of dealing without intermediaries.

For transactions at the lower end of the market — businesses below $5 million in value, straightforward structures, a single motivated strategic buyer — the cost-benefit calculation for advisory representation is different than for a $20-million or $40-million transaction. The absolute value at stake must always be weighed against the cost and complexity of a full advisory process.

The strengths are real. They are simply structurally limited in most lower-middle-market transactions by the BATNA dynamics described above.

When an M&A advisor negotiates on your behalf: engineering BATNA

The most important thing a sell-side M&A advisor does — before a single negotiation tactic is deployed — is engineer the conditions under which your BATNA is maximized. This is not a metaphor. It is a literal description of what a well-designed competitive sale process accomplishes.

The competitive process as BATNA infrastructure

A structured, advisor-managed sale process begins with the identification of the complete universe of qualified buyers for your business — strategic acquirers, financial sponsors and other parties whose interests and acquisition criteria align with your company's profile. That universe is then systematically contacted, qualified and engaged through a controlled information disclosure process designed to maximize competitive tension.

The mechanics matter. When multiple qualified buyers receive the same information simultaneously, submit indications of interest on the same timeline and understand that they are competing against other parties whose identities and offer terms they cannot see, the seller's BATNA is not merely theoretical — it is visible. Every buyer in a competitive process knows they may lose the deal to a superior competing offer. That awareness is itself the most powerful negotiating tool available to a seller, and it is entirely the product of process design.

GF Data's M&A research consistently documents that advisor-managed competitive processes achieve meaningfully higher transaction multiples than single-buyer negotiations in the lower-middle market — a finding that directly reflects the BATNA-strengthening effect of competitive process management.

The credible walk-away

Beyond competitive tension, an M&A advisor provides something that is structurally unavailable to an owner negotiating directly: the credible walk-away — without the owner having to actually walk away.

When an advisor communicates to a buyer that their offer does not meet the seller's expectations and that the seller is prepared to continue the process with other interested parties, that communication is credible precisely because the buyer knows the process exists, knows other buyers are involved and knows the advisor has managed transactions where deals did not close. The walk-away threat is not a bluff — it is a professionally delivered statement of process reality.

An owner making the same communication in a direct negotiation faces a credibility problem: the buyer may correctly assess that the owner's appetite to restart a lengthy process from scratch is limited, and that the walk-away threat is not genuinely backed by an equivalent alternative. The owner may believe it. The buyer may not.

Protecting the owner-buyer relationship

There is a final, frequently underestimated BATNA advantage of advisor-led negotiation: the owner-buyer relationship is preserved for the moments when it matters most.

In a business sale where the owner is expected to remain through a transition period, roll equity into the new entity or participate in an earnout arrangement, the quality of the post-close relationship with the buyer is a direct financial consideration. Deals that emerge from direct owner negotiations often carry a damaged relationship — the inevitable friction of price negotiation, due diligence disputes and late-stage renegotiation has been absorbed by the people who need to work together afterward.

An advisor absorbs the adversarial dynamic. The owner can maintain the collaborative, future-focused relationship that serves their post-close financial interests.

Head-to-head: BATNA management in owner-direct versus advisor-led negotiations

What the research says

The evidence base on BATNA and competitive process management in M&A is substantial and consistent across methodologies.

Fisher and Ury's foundational work established BATNA as the primary determinant of negotiating power. Subsequent experimental research by Adam Galinsky and Thomas Mussweiler at Columbia Business School confirmed that negotiators with strong alternatives outperform those without — not marginally, but systematically and significantly across experimental conditions.

The most directly applicable academic evidence for Canadian sellers comes from Golubov, Petmezas and Travlos, whose 2012 study in the Journal of Finance examined the relationship between sell-side advisory representation and acquisition premiums across thousands of transactions. Their findings are unambiguous: sell-side representation is associated with significantly higher premiums, with the effect largest in precisely the conditions that characterize the Canadian lower-middle market — smaller transactions, less publicly available information and higher information asymmetry between buyers and sellers.

The cost of advisory representation — typically a success fee of three to six per cent of transaction value in the Canadian lower-middle market — is almost always recovered, and frequently exceeded many times over, through the BATNA-strengthening effect of a well-managed competitive process. The question is not whether you can afford representation. It is whether you can afford to negotiate without it.

What this means if you are planning to sell your business

Three practical implications follow from the evidence.

First, never begin a sale conversation with a single buyer unless you have explicitly decided that a single-buyer, off-market transaction is in your interest — and you fully understand the BATNA consequences of that choice. An unsolicited approach from a buyer is flattering. It is also a deliberate strategy to engage you before you have alternatives.

Second, the time to develop your BATNA is before you need it. A structured advisory process takes months to design and execute properly. An owner who begins building competitive tension after receiving an unsolicited offer is working from a weakened position. Begin the process from strength.

Third, run the numbers honestly. The cost of advisory representation — typically three to six per cent of transaction value in this market — is a known quantity. The cost of negotiating without one is harder to measure precisely, but the research is consistent: it is larger.

Sources and further reading

Fisher, Ury & Patton — Getting to Yes (3rd ed., Penguin Books, 2011) amazon.com/Getting-Yes-Negotiating-Agreement-Without/dp/0143118757

Harvard Program on Negotiation — BATNA explained pon.harvard.edu/daily/batna/negotiate-the-best-lease-agreement

Galinsky, A.D. & Mussweiler, T. (2001) — Journal of Personality and Social Psychology, 81(4) doi.org/10.1037/0022-3514.81.4.657

Golubov, Petmezas & Travlos (2012) — "When it pays to pay your investment banker" — Journal of Finance doi.org/10.1111/j.1540-6261.2012.01741.x

Malhotra, D. & Bazerman, M.H. — Negotiation Genius (Bantam Books, 2007) amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

GF Data M&A Report (2023) gfdata.com/resources/reports

Pepperdine University Private Capital Markets Report (2024) bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

Next in the series

The complete series

Click any article to read in full

Strategy 1 · Leverage & alternatives | BATNA — know your best alternative to a negotiated agreement

How competitive alternatives determine who holds power at the negotiating table, and why the development of a strong BATNA is fundamentally different in an owner-direct versus advisor-led process.

Strategy 2 · Opening position | Anchor first and anchor high

Who sets the opening number, and why that decision shapes the entire deal. The research on anchoring bias and what it means when an owner anchors without preparation, or fails to anchor at all.

Strategy 3 · Relationship management | Separate people from the problem

Why emotional entanglement is the most costlynegotiating error business owners make, and how professional buyers exploit it deliberately, through tactics that are entirely standard in their world and entirely unfamiliar in the owner's.

Strategy 4 · Deal structure | Focus on interests, not positions

How understanding what buyers actually want — rather than what they say they want, creates deal structures that maximize total value. Why positional bargaining leaves money on the table and interests-based negotiation finds it.

Strategy 5 · Offer construction | Multiple simultaneous offers of equivalent value

How presenting two or three complete deal packages simultaneously reveals buyer priorities without a single unilateral concession, and why the analytical preparation required to do it well is beyond most owner-direct negotiations.

Strategy 6 · Communication discipline | Strategic silence

The discipline of not talking, and why most owners unknowingly concede with every word they speak after making an offer. How an advisor-managed process builds silence structurally into the negotiating dynamic, so the owner never has to fight the instinct to fill it.

Strategy 7 · Process architecture | Control the process, not just the outcome

Why process design is the most consequential negotiating variable in a business sale, and why it is structurally inaccessible to owners who negotiate without an advisor. A stage-by-stage comparison of what a designed process delivers versus a default one.

Strategy 8 · Series finale | Time pressure and deadlines

How the final 20 per cent of available time shapes the majority of concessions, and who controls the clock when it matters most. The deadline effect, the four tactics buyers use to manufacture timeline pressure, and why clock management governs all seven strategies that precede it.