ANCHOR HIGH: WHO SETS THE PRICE SETS THE DEAL

The first number in a business sale negotiation exerts a gravitational pull on every number that follows. Here is what the research says about who should set it, when and why most Canadian sellers get this wrong.

This is article 2 of 8 in a series examining the foundational negotiating strategies documented by academic and practitioner research — and comparing, for each strategy, the relative strengths and weaknesses of owner-direct versus advisor-led negotiation in Canadian lower-middle-market business sales. Each article draws on peer-reviewed research, transaction data and more than 30 years of Canadian M&A advisory experience.

The psychology of the first number

In 1974, Daniel Kahneman and Amos Tversky published a study in the journal Science that would change how researchers understood human decision-making. Among their findings was a phenomenon they called anchoring: the human tendency to rely disproportionately on the first piece of information encountered when forming a judgement, even when that information is arbitrary, incomplete or openly acknowledged as a starting point rather than a final answer.

In a negotiation, the first number stated does not merely open the conversation. It becomes the gravitational centre around which every subsequent adjustment orbits. Counteroffers, concessions and final settlements all tend to cluster closer to the anchor than either party would predict or intend. The effect is not subtle. It is one of the most replicated findings in behavioural economics, and it operates whether the parties are experienced professionals or first-time negotiators.

For a Canadian business owner selling a company, the implications are direct: whoever sets the opening number in the negotiation holds a structural advantage that persists through every round of discussion that follows. The question of whether to anchor first — and at what level — is therefore not a tactical nicety. It is one of the highest-leverage decisions in the entire sale process.

What the research confirms

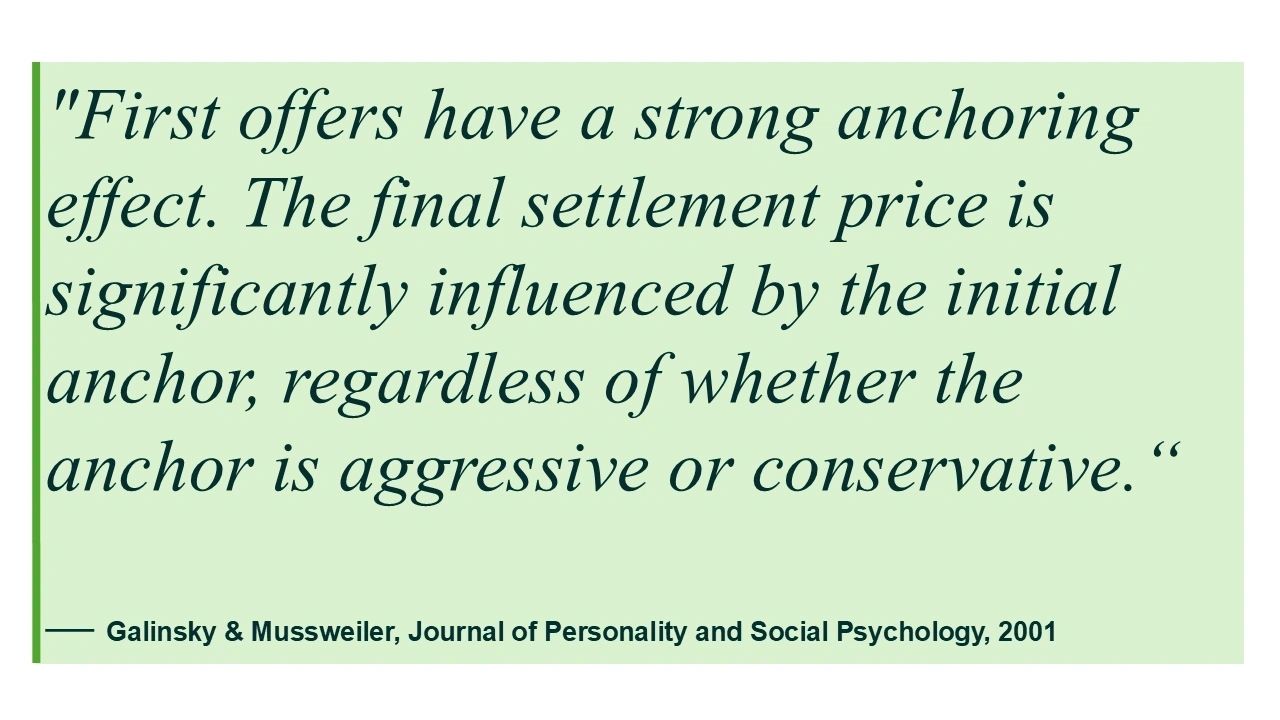

The anchoring effect in price negotiations has been studied extensively. The most directly relevant work for M&A practitioners comes from Adam Galinsky and Thomas Mussweiler at Columbia Business School, whose 2001 study in the Journal of Personality and Social Psychology tested anchor effects in simulated negotiations and found that first-mover advantage is real, measurable and durable. Negotiators who anchor first achieve significantly better outcomes — and those who anchor ambitiously but credibly outperform those who anchor conservatively.

The key word is credibly. A number that cannot be defended collapses under professional scrutiny. An anchor that is ambitious but supported by documented valuation analysis, comparable transaction data and a clear articulation of the business's value drivers holds. The difference between an anchor that sticks and one that crumbles is preparation — specifically, the quality of the valuation work and narrative behind the opening number.

A second relevant finding from Galinsky and Mussweiler is what they call the "consider the opposite" effect: negotiators who are explicitly instructed to think about why an anchor might be wrong are partially — but only partially — able to adjust away from it. Even when buyers actively try to discount an ambitious seller anchor, they remain anchored. The pull of the first number is that powerful.

RESEARCH NOTE: Kahneman and Tversky's foundational anchoring research (Science, 1974) established that initial reference points shape final judgements even when parties know the anchor is arbitrary. Galinsky and Mussweiler (2001) confirmed that in price negotiations specifically, ambitious but defensible anchors set by the seller consistently produce better outcomes than conservative ones — or than waiting for the buyer to anchor first. Sources: doi.org/10.1126/science.185.4157.1124 and doi.org/10.1037/0022-3514.81.4.657

The Canadian lower-middle-market anchoring challenge

In Canada's lower-middle market — businesses with $5 million to $50 million in annual revenue — anchoring dynamics are particularly consequential for two reasons.

First, there is no publicly available comparable transaction database that gives business owners ready access to defensible valuation benchmarks. In the large-cap public markets, comparable company multiples and precedent transactions are widely reported and easily referenced. In the lower-middle market, that data exists but it is held primarily by advisors, private equity firms and M&A data providers. An owner without access to that data cannot construct a credible anchor. They are anchoring in the dark.

Second, the buyers that typically pursue lower-middle-market businesses — private equity sponsors, family offices, strategic acquirers with active acquisition programmes — have seen hundreds of transactions and carry their own internalized sense of what businesses in any given sector should trade at. If the seller does not anchor first with a well-supported number, the buyer will anchor with theirs. And the buyer's anchor will reflect the buyer's interests, not the seller's.

Pepperdine University's Private Capital Markets Report (2024) documents that seller-side advisory representation is consistently associated with higher acquisition premiums in this market segment. A significant component of that premium is attributable to professional anchor construction — the deliberate, research-backed setting of the opening price before buyer contact begins.

When the owner negotiates directly: two ways anchoring fails

Owners who negotiate directly face two distinct anchoring failure modes. Both are common. Both are costly.

Failure mode one: not anchoring at all

The most frequent mistake is declining to state an asking price early in the process. The reasoning is usually some version of: "I want to see what they offer before I show my hand." This feels strategically prudent. In practice, it is a structural error.

When a seller declines to anchor, the buyer anchors instead. The buyer's opening offer reflects their acquisition model, their target return requirements and their assessment of what the seller's floor might be — none of which are aligned with maximizing seller value. From that point forward, the entire negotiation proceeds from a buyer-set reference point. Every concession the seller wins is measured against the buyer's anchor, not the seller's aspirations.

Waiting to see what the buyer offers is not neutrality. It is a unilateral surrender of the most powerful structural advantage available to the seller.

Failure mode two: anchoring without preparation

The second failure mode is anchoring without the valuation preparation required to hold the anchor under professional scrutiny. An owner who states an asking price based on personal expectations, conversations with peers or informal industry rules of thumb will face immediate, structured challenge from a sophisticated buyer. Questions about EBITDA adjustments, customer concentration, revenue quality, capex requirements and working capital normalization are standard buyer due diligence — and each one is a potential lever to chip away at an unsupported anchor.

An anchor that cannot be defended is worse than no anchor. It signals to the buyer that the seller has not done their homework, invites aggressive downward pressure and establishes a negotiating pattern of seller retreat that is very difficult to reverse.

What owner-direct anchoring does well

There are genuine circumstances where an owner can anchor effectively without an advisor. An owner with deep sector knowledge, access to recent comparable transaction data and strong financial analysis capability can construct and defend a credible opening number. Some strategic buyers also respond well to a direct, confident owner-stated price — particularly where a long-standing relationship exists and the buyer understands the business well.

These circumstances exist. They are simply less common in the lower-middle market than owners tend to assume — and the consequences of getting the anchor wrong are disproportionately large relative to the transaction value at stake.

When an M&A advisor negotiates on your behalf: deliberate anchor construction

A sell-side M&A advisor's approach to anchoring begins months before the first buyer conversation. The opening price is not a number chosen at the start of a meeting — it is the output of a structured analytical process, and it is the foundation on which the entire negotiation is built.

The valuation process behind the anchor

Before any buyer contact, a competent advisor conducts a thorough valuation analysis: normalized EBITDA calculation, comparable public company multiples, precedent transaction analysis from private market databases, and a qualitative assessment of the business's specific value drivers — customer quality, growth trajectory, management depth, competitive position and market dynamics.

That analysis produces an asking price that is ambitious relative to the midpoint of the value range — but defensible at every point of challenge. The advisor knows in advance which buyer objections will arise, because they have seen them in prior transactions, and the anchor has been constructed to absorb those objections without collapsing.

The confidential information memorandum as anchor reinforcement

The asking price does not stand alone. It is embedded in a confidential information memorandum (CIM) — a professionally prepared document that presents the business's financial performance, strategic position and growth opportunity in the most favourable accurate light. The CIM is itself an anchoring instrument: it frames the business at the level of the asking price, not at the level of what a buyer might otherwise assume.

Buyers who receive a well-prepared CIM alongside an ambitious asking price are anchored by both the number and the narrative. The combination is substantially more durable than a stated price alone.

Consistency across all buyer interactions

In a competitive process with multiple buyers, the advisor maintains a consistent anchor across every conversation, every management presentation and every indication of interest. No individual buyer receives signals that the anchor is flexible, negotiable or reflective of desperation. The asking price is the asking price, uniformly, until the process produces competing offers that give the seller genuine negotiating room.

An owner negotiating directly with multiple buyers — or, more commonly, sequentially with one buyer at a time — cannot maintain this discipline. Different conversations at different times inevitably produce inconsistencies that experienced buyers probe and exploit.

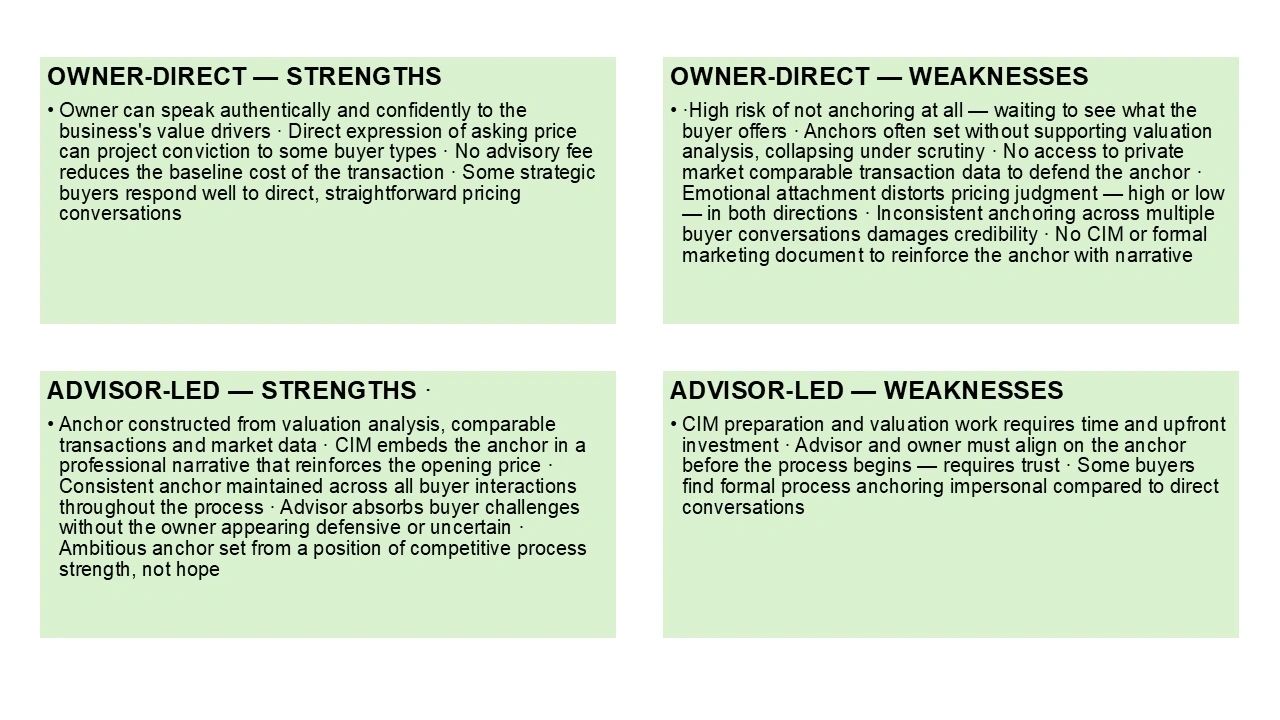

Head-to-head: anchoring in owner-direct versus advisor-led negotiations

A note on what "ambitious but credible" actually means

The research is clear that ambitious anchors outperform conservative ones — but the word credible carries real weight. An anchor that is demonstrably unsupportable damages the seller's credibility and sets a negative tone for the entire negotiation.

Ambitious means: at or above the top of the defensible value range, reflecting the business's strategic value to the right buyer rather than its average value to all buyers. It means pricing for the best-fit acquirer, not the median one.

Credible means: supportable by valuation analysis, consistent with comparable transactions in the sector, and capable of withstanding professional scrutiny at every point of challenge. An anchor does not need to be the final price. It needs to be a number the seller can defend with a straight face under professional questioning.

The combination — ambitious and credible — is what drives the outcomes the research documents. Either quality without the other produces inferior results.

What this means if you are planning to sell your business

The anchoring insight reduces to three practical disciplines for any Canadian business owner approaching a sale.

First, commit to anchoring first. The research is unambiguous: waiting to see what the buyer offers concedes the most durable structural advantage in the negotiation before it begins. Set the number. Own it.

Second, build the anchor before you build the relationship. The opening price should be determined by analysis, not by what feels comfortable to say to a buyer you have just met. By the time a buyer is at the table, the anchor needs to be ready.

Third, invest in the preparation that makes the anchor hold. Comparable transaction data, normalized financial analysis and a clear value narrative are not optional refinements — they are the foundation of an anchor that survives professional scrutiny. Without that foundation, an ambitious number becomes an embarrassing retreat waiting to happen.

Sources and further reading

Kahneman, D. & Tversky, A. (1974) — "Judgment under uncertainty: heuristics and biases" — Science, 185(4157) doi.org/10.1126/science.185.4157.1124

Galinsky, A.D. & Mussweiler, T. (2001) — "First offers as anchors" — Journal of Personality and Social Psychology, 81(4) doi.org/10.1037/0022-3514.81.4.657

Harvard Program on Negotiation — Anchoring in negotiation pon.harvard.edu/daily/negotiation-skills-daily/the-drawbacks-of-goals

Malhotra, D. & Bazerman, M.H. — Negotiation Genius (Bantam Books, 2007) amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

Pepperdine University Private Capital Markets Report (2024) bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

GF Data M&A Report (2023) gfdata.com/resources/reports

Next in the series

Article 3 of 8 Separate people from the problem: why emotional entanglement is the most common and most costly negotiating error Canadian business owners make — and how process design protects against it.

The complete series

Click any article to read in full

Strategy 1 · Leverage & alternatives | BATNA — know your best alternative to a negotiated agreement

How competitive alternatives determine who holds power at the negotiating table, and why the development of a strong BATNA is fundamentally different in an owner-direct versus advisor-led process.

Strategy 2 · Opening position | Anchor first and anchor high

Who sets the opening number, and why that decision shapes the entire deal. The research on anchoring bias and what it means when an owner anchors without preparation, or fails to anchor at all.

Strategy 3 · Relationship management | Separate people from the problem

Why emotional entanglement is the most costlynegotiating error business owners make, and how professional buyers exploit it deliberately, through tactics that are entirely standard in their world and entirely unfamiliar in the owner's.

Strategy 4 · Deal structure | Focus on interests, not positions

How understanding what buyers actually want — rather than what they say they want, creates deal structures that maximize total value. Why positional bargaining leaves money on the table and interests-based negotiation finds it.

Strategy 5 · Offer construction | Multiple simultaneous offers of equivalent value

How presenting two or three complete deal packages simultaneously reveals buyer priorities without a single unilateral concession, and why the analytical preparation required to do it well is beyond most owner-direct negotiations.

Strategy 6 · Communication discipline | Strategic silence

The discipline of not talking, and why most owners unknowingly concede with every word they speak after making an offer. How an advisor-managed process builds silence structurally into the negotiating dynamic, so the owner never has to fight the instinct to fill it.

Strategy 7 · Process architecture | Control the process, not just the outcome

Why process design is the most consequential negotiating variable in a business sale, and why it is structurally inaccessible to owners who negotiate without an advisor. A stage-by-stage comparison of what a designed process delivers versus a default one.

Strategy 8 · Series finale | Time pressure and deadlines

How the final 20 per cent of available time shapes the majority of concessions, and who controls the clock when it matters most. The deadline effect, the four tactics buyers use to manufacture timeline pressure, and why clock management governs all seven strategies that precede it.