DON'T LET EMOTION COST YOU THE DEAL YOU BUILT

The most common reason Canadian business sales collapse or lose value has nothing to do with price. It has everything to do with the owner being the wrong person to negotiate their own deal.

This is article 3 of 8 in a series examining the foundational negotiating strategies documented by academic and practitioner research, and comparing the relative strengths and weaknesses of owner-direct versus advisor-led negotiation in Canadian lower-middle-market business sales. Each article draws on peer-reviewed research, transaction data and more than 30 years of Canadian M&A advisory experience.

The principle that changes how you see every negotiation

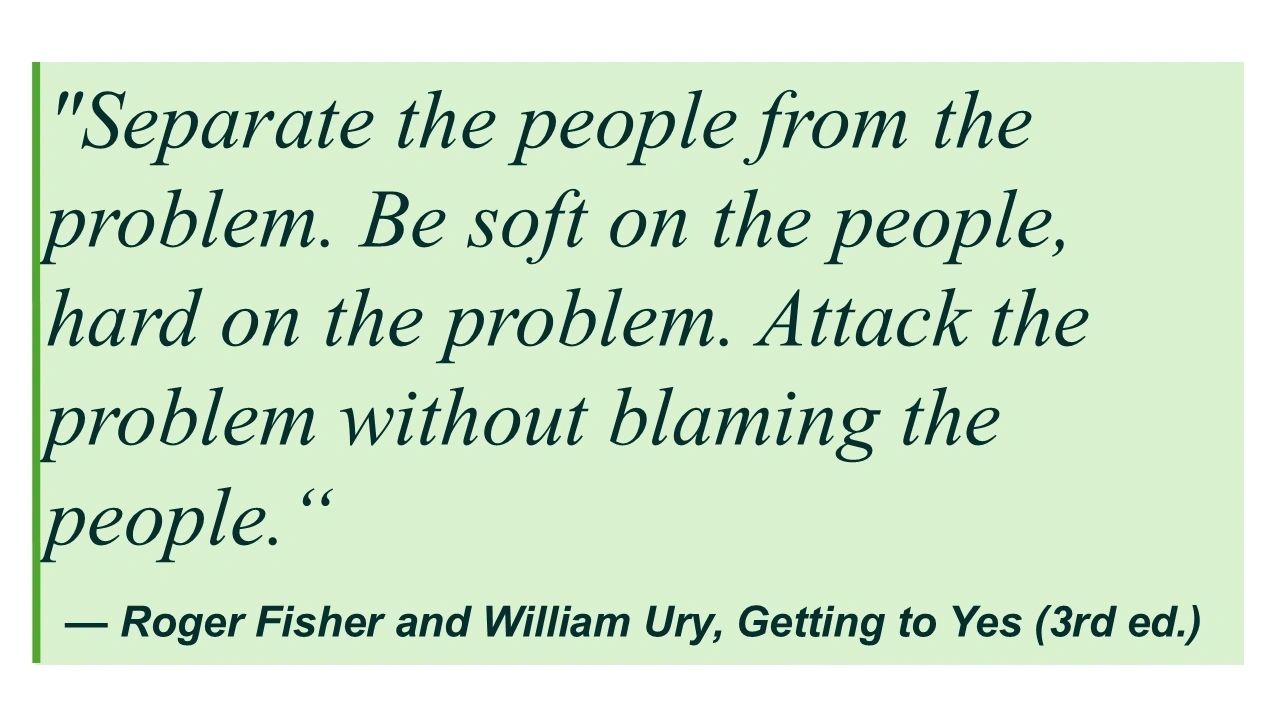

In their foundational work Getting to Yes, Roger Fisher and William Ury identified one of the most consistently destructive patterns in negotiation: the conflation of the relationship between parties with the substantive issues being negotiated. Their instruction was simple and direct. Separate the people from the problem.

What this means in practice is that the individuals across the table from each other in a negotiation are not the problem. The gap between their positions and interests is the problem. When negotiators lose sight of this distinction, they begin making decisions that serve the relationship dynamic rather than the commercial outcome. They concede on price to avoid conflict. They harden on structure because a due diligence question felt like a personal insult. They prioritize being liked over being well-compensated.

In most negotiations, the cost of this confusion is manageable. In a business sale that may represent the largest financial transaction of an owner's lifetime, it is not.

Why business owners are structurally vulnerable here

The principle of separating people from the problem is genuinely difficult to apply in any high-stakes negotiation. For a business owner selling their company, it is structurally harder than in almost any other context. Three factors explain why.

The identity problem

For most business owners, the company is not simply an asset. It is a professional identity built over decades. The products, the team, the culture, the customer relationships and the reputation in the market are extensions of the owner's judgment, effort and values. When a buyer challenges the valuation, questions the customer concentration, raises concerns about management depth or disputes the quality of earnings during due diligence, the owner does not experience these as commercial observations. They experience them as criticisms of work they spent their life building.

This is understandable. It is also one of the most reliable pathways to a poor negotiating outcome. Decisions made in response to perceived personal criticism are almost never optimal commercial decisions.

The dual-role problem

An owner negotiating directly occupies two roles simultaneously: relationship manager and commercial adversary. These roles are in direct tension. Being genuinely collaborative and warm with a buyer builds the kind of trust that makes deals close. Being a disciplined, hard-nosed negotiator protects the financial outcome. Doing both at the same time, with the same person, across the same table, is exceptionally difficult.

Experienced buyers understand this tension and use it deliberately. A buyer who compliments the business, expresses genuine enthusiasm for the team and cultivates a sense of personal connection with the owner is not simply being pleasant. They are making it psychologically harder for the owner to push back on price, hold firm on reps and warranties or threaten to walk away. The relationship that feels like a strength in the room is a liability at the negotiating table.

The reciprocity problem

Psychologist Robert Cialdini's research on influence identifies reciprocity as one of the most powerful drivers of human behaviour. When someone does something for us, or expresses genuine appreciation, we feel a strong compulsion to return it. In a negotiation, a buyer who is warm, generous with time, complimentary about the business and transparent about their intentions creates reciprocity pressure on the seller. The owner who has been treated generously feels a pull to respond in kind, often in the form of commercial flexibility.

This is not weakness or naivety. It is a normal human response to social generosity. It is also, in a negotiation, a systematic value-destruction mechanism. And experienced buyers are very good at triggering it.

RESEARCH NOTE: Cialdini's foundational research on influence, documented in Influence: The Psychology of Persuasion (updated edition, 2021), identifies reciprocity as one of the six core principles of persuasion. In a negotiation context, sellers who feel socially indebted to a buyer make measurably more concessions than those operating through an intermediary. The advisor removes the reciprocity dynamic by removing the direct social relationship from the commercial negotiation. Source: amazon.com/Influence-New-Expanded-Psychology-Persuasion/dp/0062937650

What the data says about emotion and deal outcomes

The academic evidence on emotional investment and negotiating outcomes is consistent and direct.

Deepak Malhotra and Max Bazerman at Harvard Business School document in Negotiation Genius that negotiators with high emotional attachment to a particular outcome make systematically inferior decisions across multiple dimensions. They concede earlier than the merits justify. They accept worse terms on non-price issues, such as earnout design, escrow provisions and reps and warranties, because their attention is consumed by protecting the headline number. They miss creative deal structures that might serve both parties because their emotional state narrows their cognitive aperture.

Axial's 2022 analysis of deal failures in the lower-middle market identifies relationship deterioration during the negotiation phase as one of the leading causes of transactions collapsing after a letter of intent has been signed. The pattern is consistent: an owner and buyer who began the process with genuine mutual enthusiasm allow the friction of due diligence and commercial negotiation to damage the relationship to the point where trust breaks down entirely. Once trust breaks down between parties who are negotiating directly, the deal rarely recovers.

The practical implication is not that owners should become emotionally disengaged from their businesses. It is that the commercial negotiation of the business sale is precisely the moment when emotional engagement becomes a liability rather than an asset.

When the owner negotiates directly: what goes wrong

The due diligence renegotiation

Due diligence is the phase of a transaction that most consistently triggers emotional breakdown in owner-direct negotiations. After an agreed letter of intent, the buyer's team begins a structured examination of the business: financials, contracts, customer relationships, employee arrangements, legal exposures and operational details.

For an owner who has built the business and knows it intimately, the experience of watching a team of lawyers and accountants scrutinize every corner of what they have created is genuinely uncomfortable. When that scrutiny produces findings, requests for adjustments or questions about items the owner considers irrelevant or unfair, the response is often defensive and emotional rather than strategic.

Experienced buyers use due diligence deliberately as a renegotiation tool. They surface findings, some legitimate and some manufactured, to create grounds for price reductions, expanded escrow requirements or more aggressive reps and warranties. An owner negotiating directly, whose emotional state has been compromised by months of scrutiny, is poorly positioned to distinguish between legitimate findings and tactical pressure. They are also poorly positioned to hold firm when holding firm is the right commercial response.

The timeline as emotional pressure

The longer a direct negotiation runs, the more the owner's emotional investment in completing the transaction grows. Six months into an exclusive negotiation, having shared confidential information, introduced the buyer to key employees and customers, and begun mentally planning for life after the sale, the owner's willingness to walk away from a bad deal has typically diminished substantially from where it began.

This is not irrational. It is a predictable consequence of sustained direct engagement. And it is a dynamic that sophisticated buyers manage deliberately by extending timelines at exactly the points in the process where the owner's emotional investment is highest and their commercial resistance is therefore lowest.

The post-close relationship cost

There is a final, frequently overlooked cost of emotional entanglement in direct negotiations: the damage to the relationship that must survive the transaction.

In the majority of lower-middle-market business sales, the owner does not simply hand over the keys at closing. They remain involved through a transition period, participate in an earnout arrangement or roll equity into the acquiring entity alongside the buyer. In each of these scenarios, the quality of the post-close relationship between the seller and the buyer's team is a direct financial consideration.

Deals that emerge from adversarial direct negotiations, where the owner and buyer have been grinding against each other for months without a buffer, often arrive at closing with a damaged relationship. The people who need to work collaboratively to generate the earnout are the same people who just spent six months fighting over every line of the purchase agreement. That dynamic rarely produces optimal post-close outcomes.

When an M&A advisor negotiates on your behalf: structural separation

The buffer by design

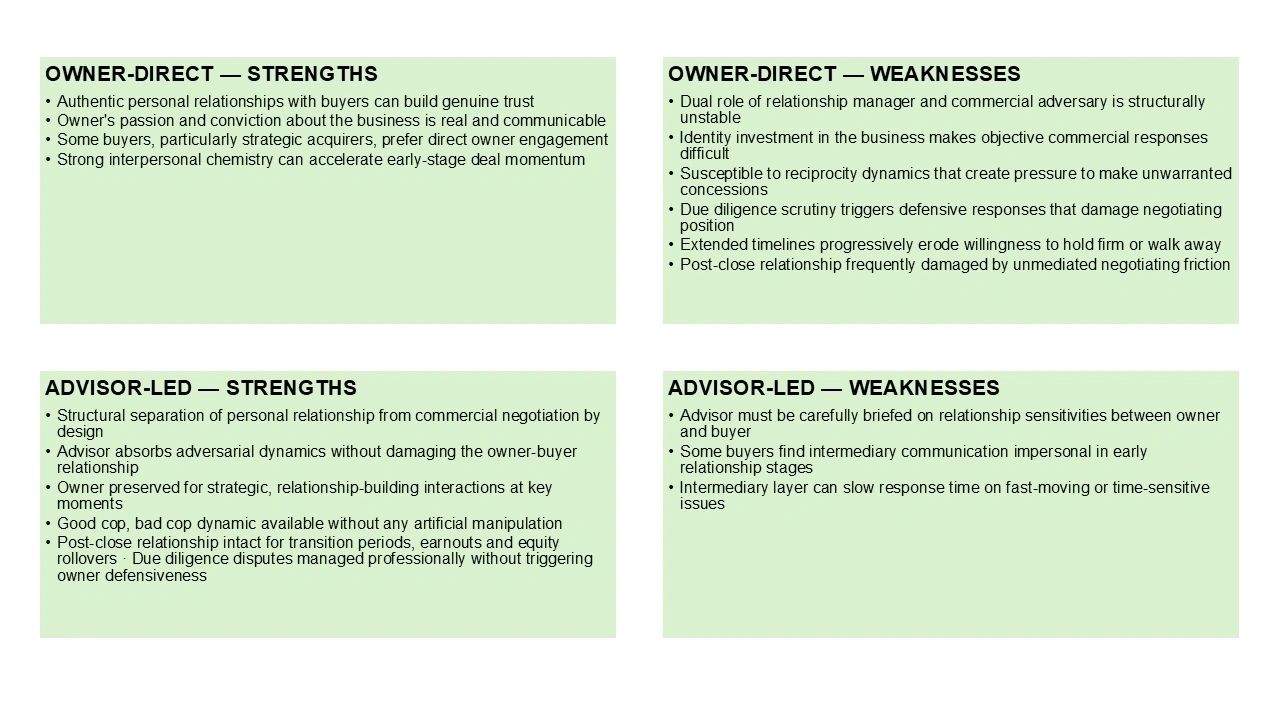

The most important structural feature of advisor-led negotiation, from a people-versus-problem perspective, is that the advisor is the buffer between the owner's emotional investment and the commercial negotiation. This is not incidental to the advisor's role. It is central to the value they provide.

When a buyer's due diligence team raises a finding that would provoke a defensive response from the owner, the advisor responds. When the buyer pushes back on price, it is the advisor who holds the anchor, absorbs the pressure and manages the commercial response. When deadlines are extended or timelines manipulated, it is the advisor who manages the owner's psychology as much as the buyer's behaviour. The owner's relationship with the buyer remains cordial, forward-looking and focused on the shared goal of closing a good deal for both parties.

This separation is not about protecting the owner from difficult conversations. It is about ensuring that difficult conversations are handled by the party best positioned to handle them without a personal stake in the emotional outcome.

The good cop, bad cop dynamic

Advisor-led negotiation creates a natural good cop, bad cop dynamic that is structurally unavailable in owner-direct transactions. The advisor absorbs the adversarial elements of the negotiation: the price challenges, the due diligence disputes, the reps and warranty negotiations and the escrow arguments. The owner remains the visionary, the strategic partner and the person the buyer is excited to work with post-close.

This dynamic is not artificial or manipulative. It reflects the genuine division of roles between an owner who built something valuable and a professional who specializes in maximizing the value of the transaction. Each party does what they do best. The result is a better commercial outcome and a better post-close relationship.

Protecting the earnout

The financial stakes of the post-close relationship are most concentrated in earnout arrangements, which are common in Canadian lower-middle-market transactions. An earnout requires the seller to continue generating results against agreed targets, typically over one to three years, while operating within the buyer's ownership structure.

The seller's ability to achieve earnout milestones depends substantially on their relationship with the buyer's leadership team. A damaged negotiating relationship creates friction in that dynamic from day one. An advisor-led negotiation that preserves the personal relationship between owner and buyer creates the conditions under which earnout performance is most likely to be achieved.

Head-to-head: separating people from the problem

The practical test

Here is a simple test for any business owner considering whether to negotiate directly or through an advisor. Imagine the following scenario.

You are six months into an exclusive negotiation. You have introduced the buyer to your key employees, your top three customers and your senior management team. You have shared three years of detailed financial statements, customer contracts and operational records. You have told your family, your board and your banker that the deal is progressing.

The buyer's lawyer then sends a due diligence finding report that includes a request to reduce the purchase price by 15 per cent, citing a combination of customer concentration risk, a pending lease renewal and a historical revenue recognition issue that your accountant considers immaterial.

Ask yourself honestly: are you capable, at that moment, of separating the people from the problem? Of assessing each finding on its commercial merits, responding strategically rather than defensively and holding firm on the items that do not warrant concession?

If the answer is yes, and you have the transactional experience to know which findings are legitimate and which are tactical, direct negotiation may serve you well.

If the answer is anything other than an unqualified yes, the structural separation that an advisor provides is worth considerably more than their fee.

Sources and further reading

Fisher, Ury & Patton — Getting to Yes (3rd ed., Penguin Books, 2011) amazon.com/Getting-Yes-Negotiating-Agreement-Without/dp/0143118757

Harvard Program on Negotiation — Principled negotiation: separate people from the problem pon.harvard.edu/daily/negotiation-skills-daily/principled-negotiation-focus-interests-not-positions

Malhotra, D. & Bazerman, M.H. — Negotiation Genius (Bantam Books, 2007) amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

Cialdini, R. — Influence: The Psychology of Persuasion (updated ed., Harper Business, 2021) amazon.com/Influence-New-Expanded-Psychology-Persuasion/dp/0062937650

Axial — Why deals fall apart (2022) axial.net/forum/why-deals-fall-apart

Pepperdine University Private Capital Markets Report (2024) bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

Next in the series

Article 4 of 8 Focus on interests, not positions: how understanding what buyers actually want creates deal structures that satisfy both sides without unnecessary economic concession.

The complete series

Click any article to read in full

Strategy 1 · Leverage & alternatives | BATNA — know your best alternative to a negotiated agreement

How competitive alternatives determine who holds power at the negotiating table, and why the development of a strong BATNA is fundamentally different in an owner-direct versus advisor-led process.

Strategy 2 · Opening position | Anchor first and anchor high

Who sets the opening number, and why that decision shapes the entire deal. The research on anchoring bias and what it means when an owner anchors without preparation, or fails to anchor at all.

Strategy 3 · Relationship management | Separate people from the problem

Why emotional entanglement is the most costlynegotiating error business owners make, and how professional buyers exploit it deliberately, through tactics that are entirely standard in their world and entirely unfamiliar in the owner's.

Strategy 4 · Deal structure | Focus on interests, not positions

How understanding what buyers actually want — rather than what they say they want, creates deal structures that maximize total value. Why positional bargaining leaves money on the table and interests-based negotiation finds it.

Strategy 5 · Offer construction | Multiple simultaneous offers of equivalent value

How presenting two or three complete deal packages simultaneously reveals buyer priorities without a single unilateral concession, and why the analytical preparation required to do it well is beyond most owner-direct negotiations.

Strategy 6 · Communication discipline | Strategic silence

The discipline of not talking, and why most owners unknowingly concede with every word they speak after making an offer. How an advisor-managed process builds silence structurally into the negotiating dynamic, so the owner never has to fight the instinct to fill it.

Strategy 7 · Process architecture | Control the process, not just the outcome

Why process design is the most consequential negotiating variable in a business sale, and why it is structurally inaccessible to owners who negotiate without an advisor. A stage-by-stage comparison of what a designed process delivers versus a default one.

Strategy 8 · Series finale | Time pressure and deadlines

How the final 20 per cent of available time shapes the majority of concessions, and who controls the clock when it matters most. The deadline effect, the four tactics buyers use to manufacture timeline pressure, and why clock management governs all seven strategies that precede it.