SELL SMARTER: FIND WHAT BUYERS REALLY WANT

Most business sale negotiations get stuck because both sides argue over positions. The owners who get the best outcomes are the ones who stop arguing over what and start asking why.

This is article 4 of 8 in a series examining the foundational negotiating strategies documented by academic and practitioner research, and comparing the relative strengths and weaknesses of owner-direct versus advisor-led negotiation in Canadian lower-middle-market business sales. Each article draws on peer-reviewed research, transaction data and more than 30 years of Canadian M&A advisory experience.

The difference between a position and an interest

Every negotiation involves two layers. The surface layer is positions: what each party says they want. The deeper layer is interests: why they want it.

A position is a stated demand. An interest is the underlying need, concern or goal that the demand is designed to address. In a business sale, a buyer's position might be a lower purchase price, a larger escrow holdback or a longer earnout period. Their interest behind each of those positions might be something quite different: certainty of close, protection against undisclosed liabilities, or confidence that the seller remains committed to the business after the transaction.

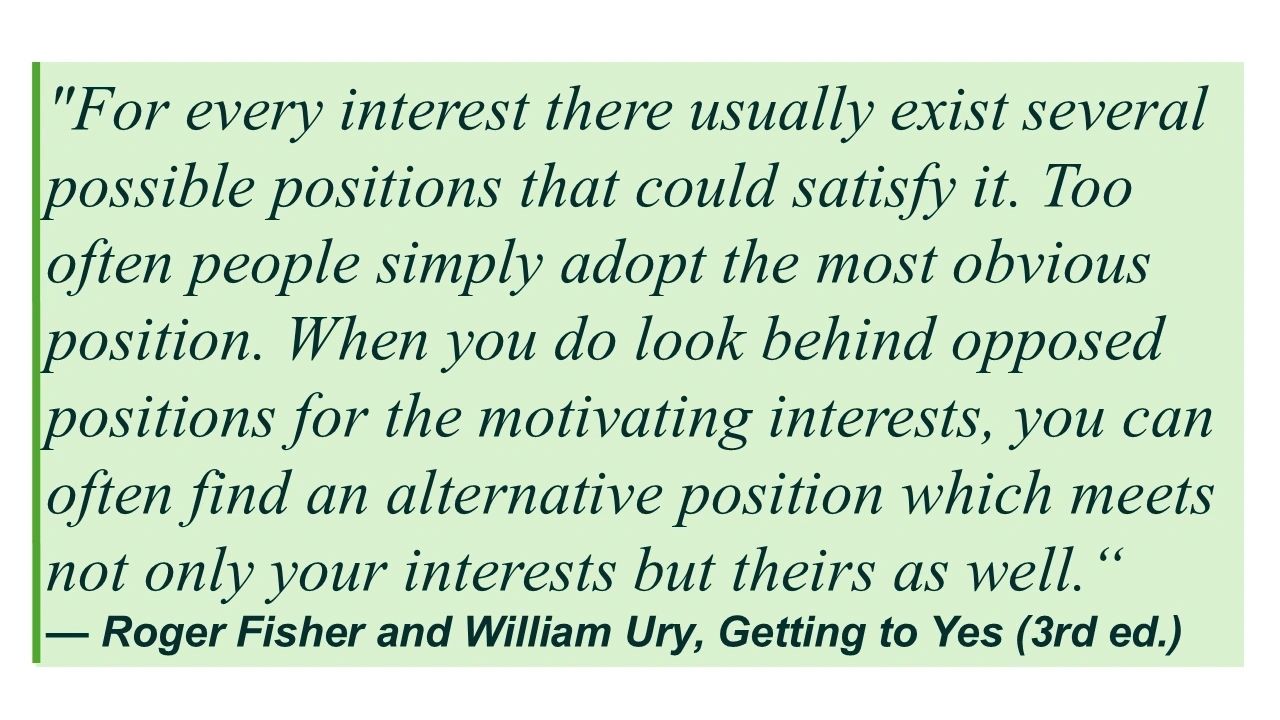

Fisher and Ury made this distinction the centrepiece of principled negotiation in Getting to Yes, and it remains one of the most practically powerful frameworks in the negotiation literature. The reason is simple: positions are zero-sum. If the buyer wants a lower price and the seller wants a higher one, one of them wins and one loses. But interests are almost never directly opposed. When you understand what is driving each position, creative solutions almost always exist that satisfy the underlying interest without requiring the other party to simply accept less.

For Canadian business owners selling their companies, this distinction between positions and interests is where an enormous amount of deal value is either created or destroyed.

Why interests matter more in the lower-middle market

In large-cap M&A transactions, the negotiation is conducted almost entirely by professional intermediaries, bankers, lawyers and financial advisors who are experienced at surfacing and trading on interests. The principals are largely removed from the day-to-day negotiation and engage primarily at the strategic level.

In Canada's lower-middle market, the situation is fundamentally different. The owner is typically the business. The buyer is acquiring not just an asset but a specific set of customer relationships, operational capabilities and often a key individual whose continued engagement is central to the investment thesis. This means the buyer's interests in a lower-middle-market transaction are substantially more personal, more complex and more varied than in a larger deal.

A private equity sponsor acquiring a platform company has different interests than a strategic acquirer looking to bolt on complementary capabilities. A family office buying a lifestyle business has different interests than a financial buyer seeking a three-to-five year return. An owner-operator acquiring a competitor has different interests than an out-of-sector acquirer entering a new market. Each of these buyer types has a distinct set of underlying interests that shapes how they weight price versus structure, certainty versus upside and speed versus thoroughness.

An owner who understands the specific interests of the buyer in front of them can negotiate in a fundamentally different way than one who treats all buyers as simply trying to pay as little as possible.

RESEARCH NOTE: Harvard Program on Negotiation research confirms that interests-based negotiation consistently produces higher joint value than positional bargaining, and that the skill gap between experienced and novice negotiators is largest precisely in the area of interests identification. Experienced negotiators spend significantly more time asking questions and surfacing the other party's underlying motivations than inexperienced ones, who tend to argue positions. Source: pon.harvard.edu/daily/negotiation-skills-daily/interests-in-negotiation

Common buyer interests that owners miss

Before examining the direct versus advisor-led dynamic, it is worth identifying the interests that most frequently drive buyer positions in lower-middle-market transactions, and that owners negotiating directly most consistently fail to recognize.

Certainty of close

One of the most powerful interests driving buyer behaviour in lower-middle-market transactions is certainty of close. Buyers who have conducted significant due diligence, allocated capital and introduced the target to their investment committee or board have a strong organizational interest in completing the transaction. When they push for a larger escrow, more protective reps and warranties or a longer earnout, they are often expressing an interest in certainty rather than a belief that the business is worth less. A seller who understands this can frequently satisfy the interest through structural assurances, insurance products or process commitments rather than price reductions.

Management continuity

In businesses where the owner is central to customer relationships or operational knowledge, the buyer's interest in retaining key people often drives positions that appear to be about price but are actually about risk. A buyer who pushes for a longer transition period, a larger rollover equity component or a more punitive earnout structure may be expressing anxiety about losing critical knowledge or relationships rather than dissatisfaction with the business's value. An owner who recognizes this interest can offer creative solutions, such as a structured knowledge transfer programme, retention arrangements for key staff or an accelerated earnout tied to specific relationship continuity metrics, that address the interest without economic concession.

Integration risk management

Strategic acquirers and private equity sponsors with existing portfolio companies have a strong interest in managing integration risk. Positions that appear to be about price adjustments, working capital normalization or reps and warranties exposure are frequently expressions of integration anxiety. A seller who can demonstrate clean systems, documented processes, a strong second tier of management and clear operational handover protocols is addressing the buyer's actual interest, and doing so far more effectively than conceding on price.

Reputational protection

Particularly among family offices, high-net-worth individual buyers and strategic acquirers with significant brand equity, reputational risk is a genuine interest that drives negotiating positions. A buyer who insists on extensive environmental, legal and employment-related reps and warranties, or who pushes for unusually broad indemnification provisions, may be primarily motivated by the reputational consequences of acquiring a business with undisclosed problems rather than by a financial assessment of the actual risk. Sellers who understand this interest can address it through enhanced disclosure, pre-transaction audits or specific insurance products rather than by accepting unlimited indemnification exposure.

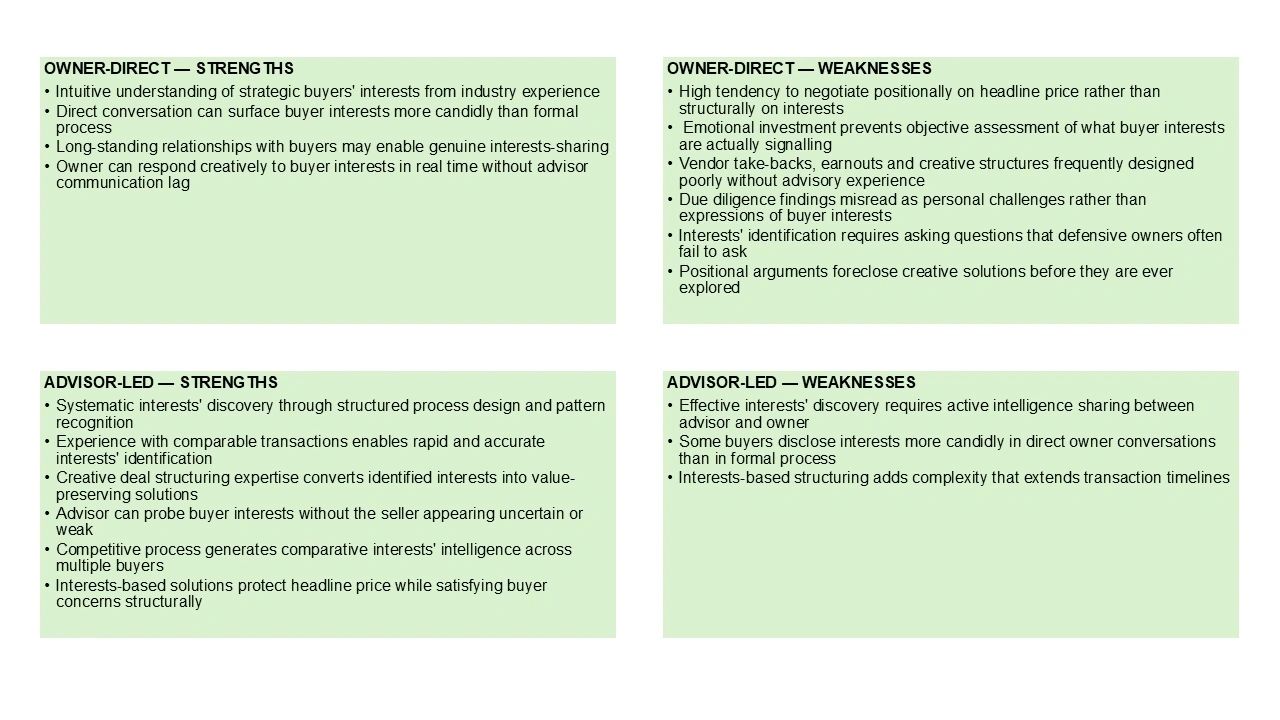

When the owner negotiates directly: the positional default

Why owners argue positions

Owners negotiating directly default to positional bargaining for reasons that are psychologically understandable and commercially problematic. The business is their primary asset and their primary identity. When a buyer challenges the valuation, the owner's instinct is to defend the number rather than explore the interest behind the challenge. When a buyer requests a larger escrow, the owner reads it as a statement about trust rather than a risk management preference. When a buyer pushes for an earnout, the owner interprets it as a lack of confidence in the business rather than a legitimate desire to share upside risk.

Each of these interpretations may have some basis in reality. None of them is a complete or accurate picture of what is driving the buyer's position. And an owner who negotiates from the interpretation rather than from the underlying interest will consistently leave value on the table.

The missed creative solution

The practical cost of positional bargaining is that creative deal structures go unrecognized and unattempted. Vendor take-back financing, equity rollovers, performance-based earnouts, staged closings, representations and warranty insurance, escrow alternatives and transition service arrangements are all tools that can be used to satisfy buyer interests without requiring the seller to accept a lower headline price.

Owners negotiating directly rarely deploy these tools effectively because accessing them requires first identifying the interest the buyer is trying to satisfy. An owner engaged in a positional argument about price is not asking the questions that would surface the interest. They are defending the number.

The Pepperdine University Private Capital Markets Report consistently documents that lower-middle-market transactions structured with creative deal components, including vendor financing and earnout arrangements, achieve higher total consideration for sellers when properly designed. The design requires interests-based thinking that is difficult to apply under the emotional and informational pressures of direct negotiation.

What owner-direct negotiation does well

There are genuine circumstances where owner-direct negotiation surfaces interests effectively. An owner with deep industry knowledge and long-standing relationships with the buyer may understand their interests intuitively and be able to address them naturally in conversation. In deals between parties who have known each other for years, the trust that makes interests-sharing possible may already exist.

Additionally, some buyers are simply more forthcoming about their underlying interests in a direct conversation with an owner than they would be in a formal process managed by an advisor. The informal candour of a direct relationship can occasionally produce insights that a structured process would not.

These advantages are real but situation-specific. They depend on the quality of the existing relationship and the sophistication of the owner's interests-recognition capability, both of which vary widely.

When an M&A advisor negotiates on your behalf: interests as process intelligence

Structured interests discovery

A skilled M&A advisor treats interests discovery as a structured analytical exercise, not a casual observation. Management presentations, buyer Q&A sessions, due diligence interactions, letter-of-intent negotiations and informal conversations with buyer representatives all generate intelligence about what a specific buyer actually values and fears. The advisor collects and interprets that intelligence systematically, building a picture of the buyer's true interests that informs every subsequent negotiating decision.

This is pattern recognition applied to deal-specific intelligence. An experienced advisor who has worked with the same type of buyer, in the same sector, on comparable transactions, arrives at interests identification faster and more accurately than an owner seeing the dynamic for the first time.

Translating interests into deal structure

Once the buyer's underlying interests are understood, a skilled advisor translates them into deal structure. If the buyer's primary interest is certainty of close, the advisor designs an escrow arrangement and reps and warranty insurance structure that satisfies the interest without reducing the headline price. If the buyer's interest is management continuity, the advisor designs a transition and retention framework that protects the seller's total consideration while addressing the buyer's organizational concern. If the buyer's interest is integration risk management, the advisor structures a disclosure protocol and operational representation framework that provides the comfort the buyer needs at a defined and limited cost to the seller.

In each case, the creative solution exists because the interest has been identified. The deal value is preserved because the structure addresses the interest without defaulting to a price reduction.

The competitive process as interests intelligence

An advisor-managed competitive process generates interests intelligence that a single-buyer negotiation cannot produce. When multiple buyers participate in a structured process, their different responses to the same information, their different questions in management presentations and their different emphasis in letters of intent all reveal the buyer-specific interests that drive their behaviour. That comparative intelligence allows the advisor to tailor the negotiation with each buyer to their specific interests, maximizing the value of each buyer relationship rather than applying a uniform approach to all of them.

Head-to-head: interests versus positions

A practical illustration

Consider a buyer who submits a letter of intent with a purchase price that is 20 per cent below the seller's asking price and includes a three-year earnout representing 30 per cent of total consideration.

The positional response is to counter at a higher price and push back on the earnout structure. This is the response most owners give. It is also the response that produces the least useful information and the least room for creative resolution.

The interests-based response begins with a question: what is driving the gap between the asking price and the offer, and what is the earnout designed to address?

The answer might reveal that the buyer's financial model cannot support the asking price at their required return threshold given current EBITDA, but that they believe the business has strong growth potential that justifies a higher total consideration over time. In that case, the earnout is not a statement that the business is worth less. It is an expression of the buyer's interest in sharing upside on growth that has not yet materialized.

Understanding this interest opens a range of creative responses that are simply not visible from a positional starting point. The seller might agree to a modest price reduction in exchange for an earnout that is shorter, better defined and carries a higher ceiling. The seller might offer representations about the growth pipeline that give the buyer comfort in raising their base price. The seller might propose a working capital mechanism that addresses the buyer's return threshold without touching the headline valuation.

None of these solutions is available to a seller who is simply arguing that the offer is too low. All of them are available to a seller who understands why the offer is structured the way it is.

What this means if you are planning to sell your business

The interests versus positions insight produces three practical disciplines for any Canadian business owner approaching a sale.

First, invest time before the process begins in understanding the specific interests of the buyer types most likely to pursue your business. A private equity buyer's interests are structurally different from a strategic acquirer's. A family office's interests are different again. Understanding these differences before the first conversation gives you a framework for interpreting buyer behaviour throughout the process.

Second, when a buyer raises a concern or requests a concession, ask why before responding. The position is rarely the full picture. The interest behind it almost always contains the seeds of a solution that serves both parties better than a simple acceptance or rejection of the stated position.

Third, recognize that the deal structures that flow from interests-based negotiation, including vendor financing, equity rollovers, performance-based earnouts and representations and warranty insurance, are complex instruments that require transactional expertise to design properly. These tools can protect your total consideration and satisfy buyer interests simultaneously. They can also, if designed poorly, create post-close obligations that cost more than the concessions they were meant to avoid. The sophistication required to use them well is a significant part of what experienced M&A advisory representation provides.

Sources and further reading

Fisher, Ury & Patton — Getting to Yes (3rd ed., Penguin Books, 2011) amazon.com/Getting-Yes-Negotiating-Agreement-Without/dp/0143118757

Harvard Program on Negotiation — Interests in negotiation pon.harvard.edu/daily/negotiation-skills-daily/interests-in-negotiation

Malhotra, D. & Bazerman, M.H. — Negotiation Genius (Bantam Books, 2007) amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

Pepperdine University Private Capital Markets Report (2024) bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

BDC — Structuring a business sale in Canada bdc.ca/en/articles-tools/entrepreneur-toolkit/sell-your-business

GF Data M&A Report (2023) gfdata.com/resources/reports

Next in the series

Article 5 of 8 Multiple simultaneous offers (MESOs): how presenting more than one complete proposal at once reveals what buyers actually value and creates room for solutions neither side could find by negotiating one issue at a time.

The complete series

Click any article to read in full

Strategy 1 · Leverage & alternatives | BATNA — know your best alternative to a negotiated agreement

How competitive alternatives determine who holds power at the negotiating table, and why the development of a strong BATNA is fundamentally different in an owner-direct versus advisor-led process.

Strategy 2 · Opening position | Anchor first and anchor high

Who sets the opening number, and why that decision shapes the entire deal. The research on anchoring bias and what it means when an owner anchors without preparation, or fails to anchor at all.

Strategy 3 · Relationship management | Separate people from the problem

Why emotional entanglement is the most costlynegotiating error business owners make, and how professional buyers exploit it deliberately, through tactics that are entirely standard in their world and entirely unfamiliar in the owner's.

Strategy 4 · Deal structure | Focus on interests, not positions

How understanding what buyers actually want — rather than what they say they want, creates deal structures that maximize total value. Why positional bargaining leaves money on the table and interests-based negotiation finds it.

Strategy 5 · Offer construction | Multiple simultaneous offers of equivalent value

How presenting two or three complete deal packages simultaneously reveals buyer priorities without a single unilateral concession, and why the analytical preparation required to do it well is beyond most owner-direct negotiations.

Strategy 6 · Communication discipline | Strategic silence

The discipline of not talking, and why most owners unknowingly concede with every word they speak after making an offer. How an advisor-managed process builds silence structurally into the negotiating dynamic, so the owner never has to fight the instinct to fill it.

Strategy 7 · Process architecture | Control the process, not just the outcome

Why process design is the most consequential negotiating variable in a business sale, and why it is structurally inaccessible to owners who negotiate without an advisor. A stage-by-stage comparison of what a designed process delivers versus a default one.

Strategy 8 · Series finale | Time pressure and deadlines

How the final 20 per cent of available time shapes the majority of concessions, and who controls the clock when it matters most. The deadline effect, the four tactics buyers use to manufacture timeline pressure, and why clock management governs all seven strategies that precede it.