GIVE BUYERS OPTIONS AND WATCH WHAT THEY CHOOSE

Most business sale negotiations move one issue at a time. Research at Harvard Business School shows this is the worst way to structure a deal conversation — and that presenting multiple complete offers simultaneously produces better outcomes for sellers and reveals more about buyers than any single-issue approach ever could.

This is article 5 of 8 in a series examining the foundational negotiating strategies documented by academic and practitioner research, and comparing the relative strengths and weaknesses of owner-direct versus advisor-led negotiation in Canadian lower-middle-market business sales. Each article draws on peer-reviewed research, transaction data and more than 30 years of Canadian M&A advisory experience.

The problem with negotiating one issue at a time

Picture the most common pattern in a Canadian lower-middle-market business sale negotiation. The seller states an asking price. The buyer counters. They negotiate price until one side moves or the conversation stalls. Then they negotiate structure: the earnout, the escrow, the working capital peg, the reps and warranties. Then employment arrangements. Then transition terms. One issue at a time, sequentially, each resolved before the next is opened.

This approach feels organized. It feels fair. It feels like progress. It is also, according to a substantial body of research in negotiation science, systematically inferior to the alternative.

The alternative is called MESOs: Multiple Equivalent Simultaneous Offers. The concept is straightforward. Instead of presenting a single proposed deal and negotiating from there, the seller presents two or three complete deal packages at once. Each package covers all the major deal dimensions: price, structure, earnout, escrow, transition and employment terms. Each package has a different configuration across those dimensions. But each package is designed to be worth approximately the same total economic value to the seller.

The buyer is then asked not to accept or reject a single offer, but to indicate which package comes closest to their preferences, and why.

The results, documented across multiple experimental and field studies, are consistently striking. Both parties achieve better outcomes. The buyer reveals their true priorities. Creative solutions emerge that sequential negotiation would never have found. And the seller signals flexibility and good faith without making a single unilateral concession.

Why MESOs work: the research foundation

The MESO technique was developed and tested by researchers at Harvard Business School, most notably Deepak Malhotra and Max Bazerman, whose work on negotiation strategy is among the most practically influential in the field.

Their research identifies three distinct mechanisms through which MESOs generate better outcomes than sequential single-issue negotiation.

Revealing priorities without asking for them directly

When a buyer receives two complete deal packages and indicates a preference for one over the other, they are voluntarily disclosing which deal dimensions they weight most heavily. A buyer who prefers the package with a higher base price and longer earnout over one with a lower base price and shorter earnout has revealed that they weight certainty of current payment more than flexibility on future performance. A buyer who prefers the package with a larger escrow and cleaner reps and warranties over one with a smaller escrow and broader indemnification has revealed that their primary concern is liability protection rather than cash flow timing.

This is intelligence the seller could never obtain by asking the buyer directly. Buyers in a negotiation do not typically share their internal weighting of deal terms. The MESO technique creates a context in which they reveal it through revealed preference rather than direct disclosure.

Signalling flexibility without conceding

In a single-offer negotiation, the only way for a seller to signal flexibility is to move from their stated position. Every signal of flexibility is therefore also a concession, and every concession raises the question of how many more will follow.

MESOs break this dynamic entirely. A seller who presents three complete packages of equivalent value has signalled substantial flexibility across deal dimensions without moving from their economic floor. The buyer understands that the seller is genuinely open to different structures. But the seller has not conceded anything, because all three packages represent the same total value to them. The flexibility is real. The economic concession is zero.

Creating room for creative solutions

Sequential single-issue negotiation produces deals that are the sum of individual compromises on individual issues. Each issue is resolved in isolation, without reference to the others. This means that trades across issues, which is where the most significant value creation in a negotiation typically occurs, are structurally blocked.

MESOs make cross-issue trades visible and possible. When a buyer indicates a preference for Package A over Package B, and explains that they prefer the earnout structure in A but the escrow provision in B, the seller now has the information needed to propose a Package C that combines the buyer's preferred elements from both. This is a genuinely better deal for both parties than either A or B would have produced through sequential negotiation. It would simply never have been found without the MESO process to surface the preferences that made it visible.

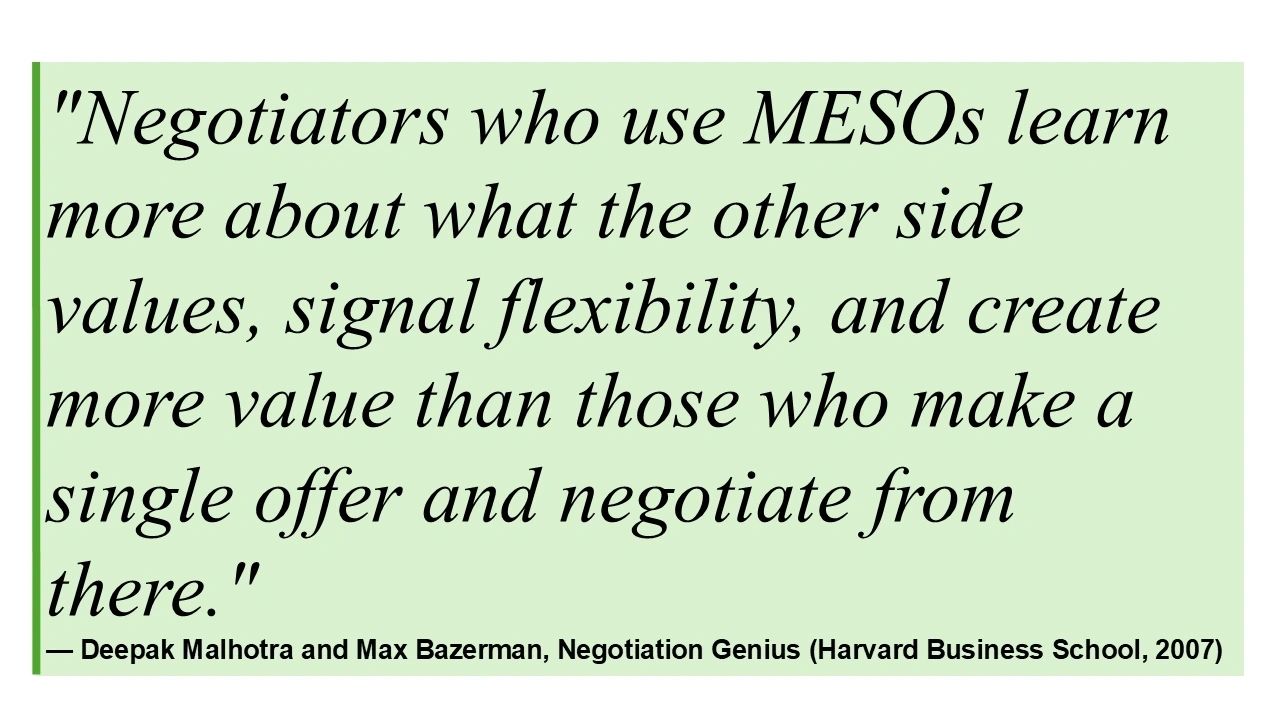

RESEARCH NOTE: Malhotra and Bazerman's experimental research documents that negotiators who use MESOs consistently achieve higher joint value than those using sequential single-issue approaches. The effect is largest in complex, multi-dimensional negotiations with multiple tradeable issues, which is precisely the structure of a lower-middle-market business sale. The research also documents higher post-negotiation satisfaction among both parties in MESO negotiations, with implications for the post-close relationship. Source: Malhotra, D. and Bazerman, M.H., Negotiation Genius (Bantam Books, 2007) — amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

MESOs in the context of a Canadian business sale

A lower-middle-market business sale is among the most multi-dimensional negotiations that most business owners will ever encounter. The deal dimensions that are typically in play simultaneously include the following.

Base purchase price. Earnout amount, duration, metrics and payment structure. Escrow amount, holdback period and release conditions. Working capital peg, target and adjustment mechanism. Representations and warranties scope and survival periods. Indemnification caps, baskets and carve-outs. Vendor take-back financing amount and terms. Equity rollover amount and structure. Transition services period and compensation. Non-compete scope, duration and geography. Employment arrangements for key management.

Each of these dimensions is independently negotiable. Each has a different relative weight for different buyers depending on their acquisition model, their risk appetite and their specific interest in this particular business. The interaction effects between them, a longer earnout combined with a smaller escrow has different risk implications than a shorter earnout combined with a larger escrow, create a deal space of enormous complexity.

Sequential negotiation navigates this complexity one dimension at a time, which means the interaction effects are never examined, the cross-issue trades are never explored and the deal that emerges is almost certainly not the one that best serves both parties' interests. MESOs are designed precisely for this kind of multi-dimensional complexity.

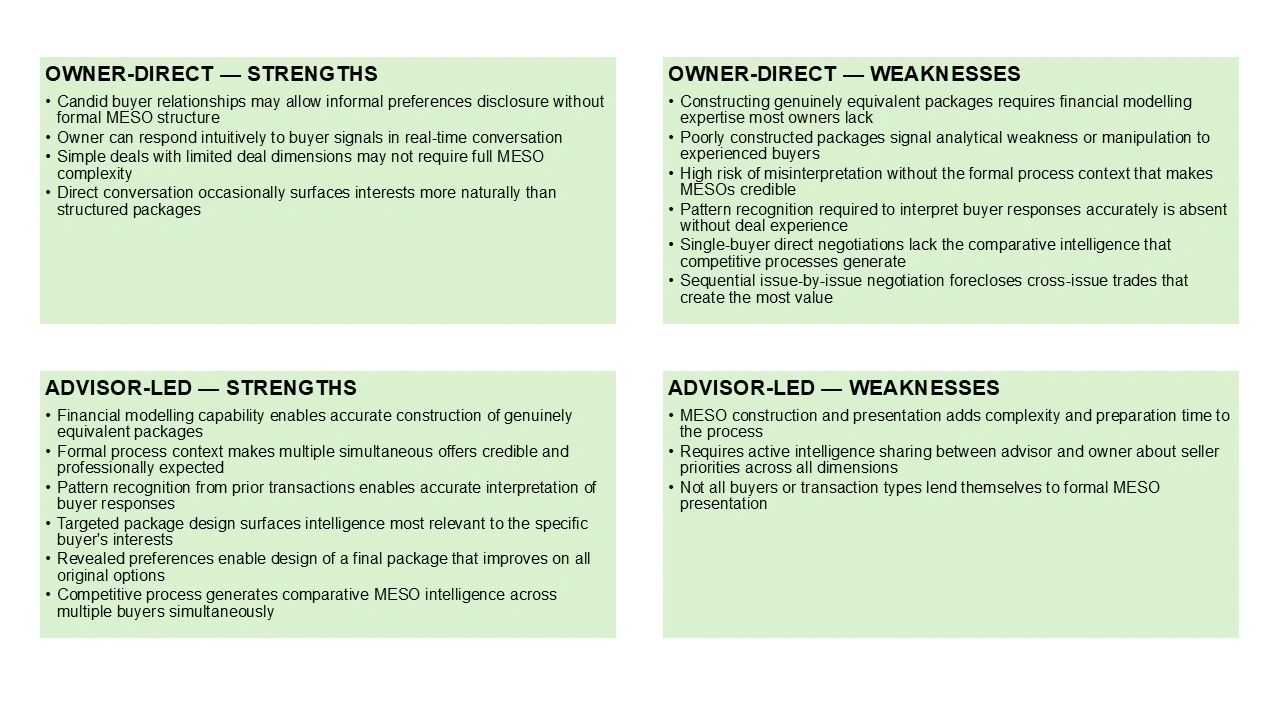

When the owner negotiates directly: why MESOs rarely appear

The construction problem

Deploying MESOs effectively requires the ability to construct multiple deal packages that are genuinely equivalent in total economic value to the seller. This is not a trivial analytical exercise. It requires a clear quantification of the seller's economic position across all deal dimensions, the ability to model the net present value of different earnout structures, the judgment to assess the economic cost of different escrow and indemnification provisions, and the skill to design packages that appear different in structure while being genuinely comparable in total value.

Owners negotiating directly rarely have the transactional experience or the financial modelling capability to do this accurately. The most common result of an owner attempting to present multiple options without proper construction is packages that are not actually equivalent, either obviously favouring the seller in ways the buyer will identify immediately, or inadvertently conceding value that the owner did not intend to offer.

A MESO that is not properly constructed is worse than no MESO at all. It signals either analytical weakness or a deliberate attempt to confuse, neither of which serves the seller's interests.

The presentation problem

Even when the packages are properly constructed, presenting multiple simultaneous offers requires a level of process confidence that is difficult to sustain in a direct owner-to-buyer conversation. The technique can easily be misread by a buyer as indecisiveness, desperation or an attempt to manipulate. Presented without the right framing, multiple simultaneous offers can undermine rather than strengthen the seller's position.

Advisors present MESOs routinely, in the context of formal offer processes where multiple packages are a natural and expected element of the negotiation. Owners presenting them in informal direct conversations are working without that contextual protection, and the risk of misinterpretation is substantially higher.

The pattern recognition problem

The value of the intelligence that MESOs generate depends entirely on the ability to correctly interpret the buyer's response. When a buyer indicates a preference for one package over another, that preference reveals something specific about their underlying interests. But translating that revealed preference into an accurate understanding of what the buyer actually values, and then designing a response that exploits that intelligence optimally, requires pattern recognition from prior transactions.

An advisor who has observed the same buyer type respond to similar package configurations in multiple previous transactions will interpret the signal accurately and act on it effectively. An owner seeing the dynamic for the first time may not recognize what the buyer's response is actually revealing, and will therefore fail to capture the value that the MESO process was designed to surface.

What owner-direct negotiation does well here

There is a limited circumstance in which owner-direct negotiation can approximate the MESO approach effectively. An owner who has a genuine, candid relationship with a buyer and has invested time in understanding that buyer's specific interests can sometimes structure an informal conversation that surfaces the same preference intelligence a formal MESO process would generate.

This typically happens in deals between parties with a long prior relationship, where the trust required for genuine preferences disclosure already exists. It is situation-specific, relationship-dependent and not transferable to deals with unfamiliar buyers. But where it does exist, it is a real capability that formal process cannot fully replicate.

When an M&A advisor negotiates on your behalf: MESOs as a structured tool

Constructing packages that are genuinely equivalent

An experienced M&A advisor has the financial modelling capability, the transaction database and the deal structuring experience to construct multiple packages that are genuinely equivalent in total economic value to the seller. This requires quantifying the seller's net position across all deal dimensions, including the time value of deferred consideration, the expected cost of earnout and escrow provisions and the risk-adjusted value of indemnification exposure.

The packages are then designed to offer the buyer meaningful and visible choice across dimensions that the advisor already suspects are relevant to that specific buyer's interests. A buyer who has emphasized management continuity in early conversations might receive packages that differ primarily on transition period length and equity rollover structure. A buyer who has focused on liability exposure might receive packages that vary primarily on escrow amount and indemnification cap design. The packages are targeted to reveal the specific intelligence most useful for the subsequent negotiation.

The formal process as MESO context

In an advisor-managed competitive process, multiple simultaneous offers are a natural and expected element of the formal bid structure. Buyers who participate in a structured process understand that presenting multiple packages reflecting different structural preferences is a standard professional practice, not a sign of seller uncertainty. The formal process provides the contextual protection that makes MESOs credible and effective.

This context is itself a significant advantage. The same technique that might appear unusual or desperate in a direct owner conversation is routine and professionally credible in an advisor-managed process. The perception of the tool shapes its effectiveness, and the advisor's process design determines the perception.

Using MESO intelligence to close the optimal deal

The intelligence generated by buyer responses to a MESO package is only as valuable as the advisor's ability to act on it. An experienced advisor uses the revealed preferences to design a final negotiating position that addresses the buyer's highest-priority interests while protecting the seller's economic floor across all dimensions.

In practice, this often means proposing a package that the buyer did not initially identify, one that combines elements from different packages in a configuration that the advisor could only design because the MESO process revealed what the buyer actually valued. This package frequently represents a genuine improvement for both parties over any of the original options, which is precisely the outcome that principled negotiation research predicts from an effective interests-based process.

Head-to-head: MESOs in owner-direct versus advisor-led negotiations

A practical illustration

Consider a seller presenting two packages to a private equity buyer.

Package A: $18 million base price, 18-month earnout of up to $3 million tied to EBITDA targets, $1.5 million escrow for 12 months, standard reps and warranties with an indemnification cap of 15 per cent of purchase price.

Package B: $16 million base price, 36-month earnout of up to $5 million tied to revenue growth targets, $750,000 escrow for 18 months, enhanced reps and warranties with an indemnification cap of 25 per cent of purchase price.

Both packages are worth approximately the same total consideration to the seller under a range of reasonable business performance assumptions. But they are structured very differently.

If the buyer responds that they prefer Package A but would like to explore whether the earnout metrics could incorporate a revenue component alongside the EBITDA target, the seller has learned something specific and valuable. The buyer weights the higher base price over the lower one. They are comfortable with a shorter earnout. But they want growth-linked upside, which Package A does not provide in the form they prefer.

The seller can now design a Package C that the MESO process made possible: a base price close to Package A, an earnout that includes both EBITDA and revenue components as the buyer signalled, and escrow terms from Package A. This package did not exist before the MESO process. It is a genuinely better deal for both parties than either original option. And it would simply never have emerged from a sequential negotiation that began with the buyer countering on price alone.

What this means if you are planning to sell your business

Three practical disciplines follow from the MESO research for Canadian business owners approaching a sale.

First, resist the instinct to negotiate one issue at a time. Sequential issue-by-issue negotiation feels controlled and manageable. It is also the approach that produces the least information about buyer priorities and the fewest opportunities for creative value creation. The discomfort of presenting multiple complete packages simultaneously is worth the intelligence and flexibility it generates.

Second, invest in the construction quality of your packages. A MESO that is not genuinely equivalent in economic value is worse than no MESO. The analysis required to build properly equivalent packages is not trivial, and the consequences of getting it wrong in front of a sophisticated buyer are significant. If you do not have the financial modelling capability to do this accurately, it is a strong signal that advisory representation is appropriate.

Third, recognize that the value of MESOs lies not in the packages themselves but in the intelligence they generate and the creative solutions that intelligence makes possible. Presenting multiple options is the beginning of the MESO process. Interpreting the buyer's response correctly and using that interpretation to design the optimal final deal is where the value actually lives.

Sources and further reading

Malhotra, D. and Bazerman, M.H. — Negotiation Genius (Bantam Books, 2007) amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

Harvard Program on Negotiation — Multiple equivalent simultaneous offers pon.harvard.edu/daily/negotiation-skills-daily/make-the-most-of-your-negotiation-with-multiple-equivalent-simultaneous-offers

Fisher, Ury and Patton — Getting to Yes (3rd ed., Penguin Books, 2011) amazon.com/Getting-Yes-Negotiating-Agreement-Without/dp/0143118757

GF Data M&A Report (2023) gfdata.com/resources/reports

Pepperdine University Private Capital Markets Report (2024) bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

Next in the series

Article 6 of 8 Strategic silence: the discipline of not talking — and why most Canadian business owners unknowingly give away their negotiating position with every word they speak after making an offer.

The complete series

Click any article to read in full

Strategy 1 · Leverage & alternatives | BATNA — know your best alternative to a negotiated agreement

How competitive alternatives determine who holds power at the negotiating table, and why the development of a strong BATNA is fundamentally different in an owner-direct versus advisor-led process.

Strategy 2 · Opening position | Anchor first and anchor high

Who sets the opening number, and why that decision shapes the entire deal. The research on anchoring bias and what it means when an owner anchors without preparation, or fails to anchor at all.

Strategy 3 · Relationship management | Separate people from the problem

Why emotional entanglement is the most costlynegotiating error business owners make, and how professional buyers exploit it deliberately, through tactics that are entirely standard in their world and entirely unfamiliar in the owner's.

Strategy 4 · Deal structure | Focus on interests, not positions

How understanding what buyers actually want — rather than what they say they want, creates deal structures that maximize total value. Why positional bargaining leaves money on the table and interests-based negotiation finds it.

Strategy 5 · Offer construction | Multiple simultaneous offers of equivalent value

How presenting two or three complete deal packages simultaneously reveals buyer priorities without a single unilateral concession, and why the analytical preparation required to do it well is beyond most owner-direct negotiations.

Strategy 6 · Communication discipline | Strategic silence

The discipline of not talking, and why most owners unknowingly concede with every word they speak after making an offer. How an advisor-managed process builds silence structurally into the negotiating dynamic, so the owner never has to fight the instinct to fill it.

Strategy 7 · Process architecture | Control the process, not just the outcome

Why process design is the most consequential negotiating variable in a business sale, and why it is structurally inaccessible to owners who negotiate without an advisor. A stage-by-stage comparison of what a designed process delivers versus a default one.

Strategy 8 · Series finale | Time pressure and deadlines

How the final 20 per cent of available time shapes the majority of concessions, and who controls the clock when it matters most. The deadline effect, the four tactics buyers use to manufacture timeline pressure, and why clock management governs all seven strategies that precede it.