WHO CONTROLS THE CLOCK CONTROLS THE DEAL

Research confirms that most concessions in any negotiation happen in the final stretch of available time. In a Canadian business sale, experienced buyers engineer the clock deliberately. Here is what that costs sellers who are not prepared for it, and what it looks like when the seller controls the timeline instead.

This is article 8 of 8 in a series examining the foundational negotiating strategies documented by academic and practitioner research, and comparing the relative strengths and weaknesses of owner-direct versus advisor-led negotiation in Canadian lower-middle-market business sales. Each article draws on peer-reviewed research, transaction data and more than 30 years of Canadian M&A advisory experience. This is the final article in the series.

The deadline effect: what the research shows

In 2004, Deepak Malhotra at Harvard Business School published research that documented one of the most consistent and practically significant findings in negotiation science. Across a wide range of negotiation contexts, the overwhelming majority of concessions made by either party occur in the final fraction of available time, regardless of how long the overall negotiation has lasted.

The implication is direct and uncomfortable for anyone who has spent months negotiating a business sale. The concessions that define the outcome of the transaction are not distributed evenly across the negotiating timeline. They are concentrated at the end, when deadlines are real or perceived to be real, when the cost of no deal has become fully apparent to both parties and when the psychological investment in completion is at its highest. The party who manages that final stretch most effectively does not simply negotiate a better outcome. They capture a disproportionate share of the value that the entire process was designed to create.

The secondary finding from Malhotra's research is equally important: whether a deadline is real or merely perceived, it produces the same concession behaviour. A buyer who creates the impression of a deadline, without any genuine time constraint driving it, generates the same urgency in the seller as a buyer facing an actual board approval date or fund closing requirement. The deadline effect operates on psychology, not on calendar facts. And experienced buyers in the lower-middle market are very good at manufacturing psychology.

Why the lower-middle market is especially exposed

The Canadian lower-middle market has a specific set of structural characteristics that make deadline management particularly consequential for sellers.

The seller's urgency profile

Business owners selling lower-middle-market companies are almost always selling for personal reasons that have a timeline: retirement planning, health considerations, partnership transitions, estate planning requirements or simply the desire to complete a transaction while market conditions are favourable. These personal timelines are real, they are often known or inferrable by experienced buyers and they create a genuine urgency asymmetry that sophisticated acquirers assess and exploit deliberately.

A private equity buyer with multiple acquisition targets, a flexible fund deployment schedule and a team of analysts generating new opportunities has a fundamentally different relationship with time than an owner who has decided that this year is the year they want to close a transaction. The buyer's cost of a delayed deal is measured in marginal opportunity cost. The seller's cost of a delayed deal is measured in personal circumstances that are not improving with time. That asymmetry is leverage, and buyers use it.

The due diligence timeline as a renegotiation tool

In the lower-middle market, due diligence timelines are among the most consistently abused process tools in the buyer's arsenal. After a letter of intent has been signed and exclusivity has been granted, the buyer's diligence team begins a structured examination of the business. That examination is supposed to verify the information on which the offer was based. In practice, it frequently extends well beyond verification into renegotiation.

Extended due diligence timelines serve the buyer's interests in two ways. First, they increase the seller's psychological investment in completion because every additional week spent in due diligence is another week in which the seller has been unable to pursue alternative buyers, has disclosed additional confidential information and has moved closer to the finish line in their personal planning. Second, they generate findings, some legitimate and some manufactured, that arrive instantly when the seller's willingness to contest them is at its lowest. The combination of extended timeline and manufactured urgency after diligence is one of the most reliable patterns in lower-middle-market buyer tactics.

The late-stage condition

A related tactic is the late-stage condition: a new requirement, concern, or deal modification introduced by the buyer in the final weeks before signing, when the seller's investment in completion is highest and their appetite for reopening the negotiation is lowest. The late-stage condition might be a modest price adjustment tied to a due diligence finding. It might be an expanded indemnification provision justified by a legal review. It might be a working capital target adjustment that the buyer's financial team has identified as technically supportable under the purchase agreement mechanics.

Each of these conditions, in isolation, may represent a relatively small economic impact. But they arrive at a moment specifically chosen to minimize resistance, and they often arrive in combination, creating a cumulative late-stage renegotiation that Axial's 2022 analysis of deal failures identifies as one of the most consistent value-destruction events in owner-direct transactions.

RESEARCH NOTE: Malhotra's research confirms that most concessions in a negotiation are concentrated in the final 20 per cent of available time, and that manufactured deadlines produce the same concession behaviour as real ones. Axial's 2022 analysis of lower-middle-market deal failures identifies late-stage renegotiation after letter-of-intent signing as one of the leading causes of both deal collapse and value destruction in transactions where the seller lacks adequate advisory representation. Sources: hbs.edu/faculty/Pages/item.aspx?num=16979 and axial.net/forum/why-deals-fall-apart

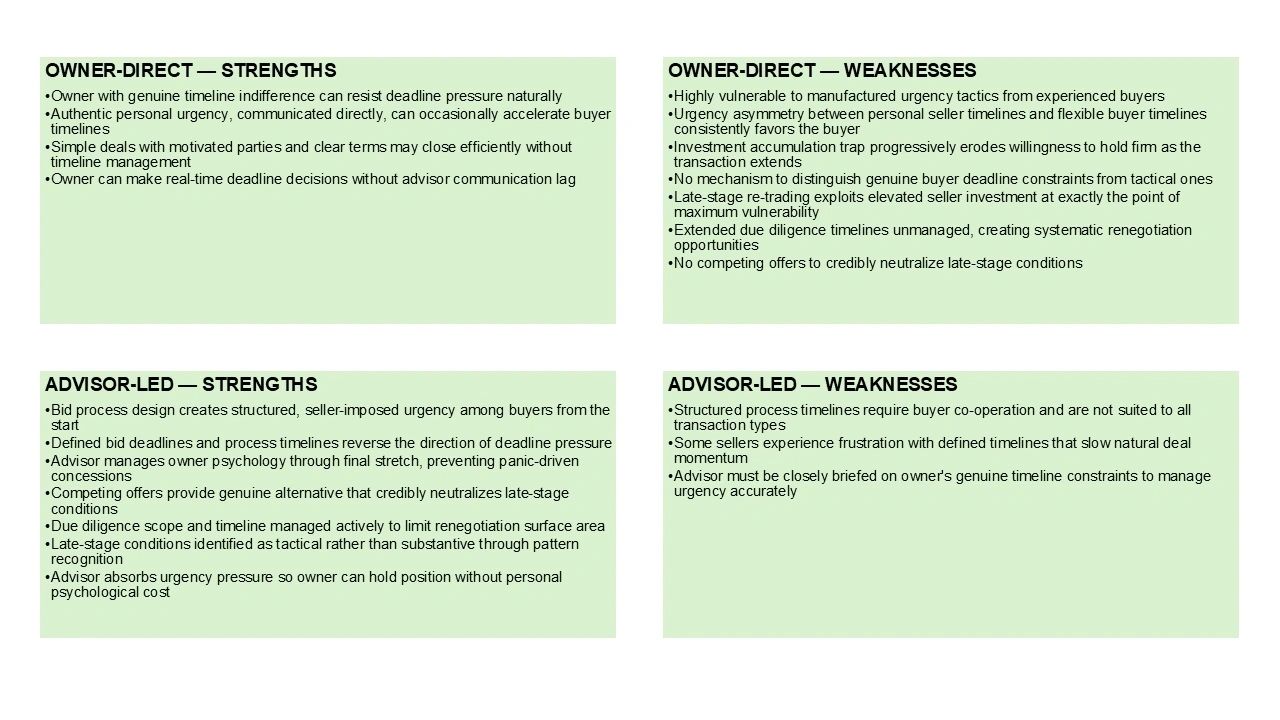

When the owner negotiates directly: how the clock works against you

The manufactured urgency problem

Experienced buyers are skilled at creating urgency that serves their interests while resisting urgency that serves the seller's. In a direct negotiation, a buyer who wants to accelerate a decision will introduce artificial time pressure: an investment committee meeting that requires a response by Friday, a competing acquisition that may absorb the capital allocated to this transaction, a fund closing date that makes a delayed close operationally complicated. Each of these constraints may be real or entirely manufactured.

An owner negotiating directly has no mechanism to assess which constraints are genuine and which are tactical. More importantly, they have no professional counterpart to absorb the psychological pressure those constraints create. The urgency arrives directly, is experienced personally and tends to produce exactly the concession behaviour it was designed to elicit: a faster agreement to terms that a less pressured seller would have held out against.

The reverse dynamic is equally damaging. When the seller wants to accelerate the timeline, a buyer who is comfortable with delay simply allows the process to slow. Requests for additional information extend the due diligence window. Legal reviews take longer than anticipated. Internal approvals require additional documentation. The buyer's timeline management is passive, almost invisible and completely effective. The seller's urgency is real. The buyer's accommodation of it is entirely optional.

The investment accumulation trap

The timeline problem in owner-direct negotiations is compounded by what we might describe as the investment accumulation trap. As a negotiation extends over months, the seller's investment in completing the transaction accumulates in multiple dimensions simultaneously.

Financial investment: professional fees for accountants and lawyers engaged during the process. Time investment: dozens of hours spent in meetings, due diligence preparation, management presentations and document review. Emotional investment: the seller has begun planning for life after the transaction, has told family and key advisors that the deal is progressing and has mentally moved toward a future that includes the completion of this specific sale. Relational investment: the seller has developed a genuine relationship with the buyer's team, shared confidential information and built a degree of mutual trust that makes the idea of starting the process over genuinely unappealing.

Each of these investments increases the seller's psychological cost of walking away. And each additional week that passes without completion adds to all of them simultaneously. By the time a buyer introduces a late-stage condition in week twenty-two of an exclusive negotiation, the seller's accumulated investment in completion is so high that the rational economic case for contesting the condition is overwhelmed by the psychological cost of risking the deal.

Buyers in the lower-middle market understand this dynamic with precision. The timing of late-stage conditions is not accidental.

The re-trading pattern

The most financially damaging manifestation of deadline pressure in owner-direct negotiations is what practitioners call re-trading: the systematic renegotiation of agreed deal terms in the final stages of a transaction, using due diligence findings and manufactured urgency as the justification.

Re-trading typically follows a predictable sequence. A letter of intent is signed at an agreed purchase price. Due diligence begins. Findings emerge, some legitimate and some tactical. The buyer communicates that the findings justify a price adjustment, an expanded escrow or a modified earnout structure. The seller, now in exclusivity, aware of their accumulated investment in completion and facing a defined signing timeline, makes the adjustment.

This sequence repeats, sometimes multiple times, before the transaction closes. Each individual adjustment may be modest. The cumulative effect over the final weeks of a transaction is frequently substantial. The purchase agreement that is signed bears a meaningful resemblance to the letter of intent but is rarely identical, and the differences are almost always in the buyer's favour.

What owner-direct negotiation does well here

There is a narrow circumstance in which an owner who is genuinely indifferent to the timing of a transaction can use deadline management effectively. An owner who has no personal urgency, has multiple qualified buyers engaged simultaneously and has the emotional discipline to walk away from a late-stage condition without hesitation is well-positioned to resist deadline pressure.

These conditions exist. They are uncommon in the lower-middle market, where most owners are selling for reasons that create genuine personal timeline pressure. And even where they exist, the structural advantages of a designed timeline, one that creates urgency among buyers rather than simply resisting urgency from them, are difficult to replicate without advisory process architecture.

When an M&A advisor negotiates on your behalf: controlling the clock from both ends

Building urgency into the process architecture

The most important timeline management tool available in an advisor-led transaction is a bid process design that creates genuine, structured urgency among buyers from the start. A formal bid process letter that specifies a first-round offer deadline, a management presentation period and a final offer deadline imposes a timeline that buyers must respond to rather than manage.

This urgency is not manufactured in the sense that buyers experience it as pressure they can dismiss. It is structural: the competitive process will advance on the defined schedule whether any individual buyer is ready or not. A buyer who misses a bid deadline loses their place in the process. A buyer who does not respond to a management presentation invitation does not receive one. The timeline is the timeline, and the seller designed it.

This reversal of urgency direction is one of the most powerful effects of a well-run competitive sale process. Instead of the seller experiencing pressure to respond to buyer-imposed deadlines, buyers experience pressure to meet seller-imposed ones. The psychological dynamics of the deadline effect operate in the seller's favour rather than against them.

Managing the owner's psychology through the final stretch

An advisor's second critical timeline management function is managing the owner's own psychological experience of the final stages of a transaction. When a buyer introduces a late-stage condition, when due diligence extends beyond its scheduled completion and when the signing date slips for the third consecutive time, the owner's instinct is to accommodate, to find a way to keep the deal moving, to make the concession that will unlock the next step toward closing.

The advisor's role in these moments is to provide the professional detachment the owner cannot easily provide for themselves. An experienced advisor who has seen the same pattern in dozens of prior transactions can identify a late-stage condition as tactical rather than substantive, advise the owner to hold their position and communicate to the buyer that the condition will not be accommodated without a concrete alternative offer of equivalent value. This advice is straightforward. It is extraordinarily difficult for an owner to act on without a professional buffer between their psychological state and the commercial decision.

Using competing offers to manage deadline dynamics

In a well-run competitive process, the presence of competing offers provides the most powerful deadline management tool available: the genuine alternative. When a buyer introduces a late-stage condition, the advisor can credibly communicate that the seller has other qualified parties prepared to proceed on the terms already agreed. This communication is not a bluff. The competing process exists. The alternative is real.

The credibility of the alternative is what neutralizes the late-stage condition. A buyer who knows that accommodating the condition is a choice, not a necessity, because the seller has a genuine alternative, will frequently withdraw the condition rather than risk losing the transaction entirely. This outcome is not available to an owner in a single-buyer exclusive negotiation, where the absence of alternatives makes the seller's resistance to late-stage conditions structurally incredible.

Protecting the due diligence timeline

An advisor also manages the due diligence timeline actively, setting defined completion expectations, limiting scope creep in diligence requests and ensuring that the buyer's diligence team operates within parameters that prevent the extended timeline tactic from taking hold.

When diligence requests extend beyond the agreed scope or the timeline stretches without justification, the advisor communicates firm expectations about completion and, where necessary, signals that the process will advance on its defined timeline whether diligence is complete or not. This communication is credible precisely because the advisor has managed prior transactions in which it was acted upon. The buyer understands that the timeline threat is real, and diligence tends to accelerate accordingly.

Head-to-head: deadline management in owner-direct versus advisor-led negotiations

The pattern in practice: a composite illustration

Consider a business owner twelve weeks into an exclusive negotiation following a letter-of-intent signing at an agreed purchase price of $22 million. Due diligence was scheduled to complete in six weeks. It is now in week twelve with no defined end in sight.

The buyer's diligence team has identified three items for discussion: a customer concentration finding, a lease renewal that falls within the earnout period and a historical accounting treatment that the buyer's auditors have characterized as aggressive. Each finding has been presented as a potential basis for price adjustment. No specific adjustment has been proposed yet.

The owner has told their spouse, their banker, their accountant and two trusted advisors that the deal is progressing. They have mentally committed to the transition and have begun quietly planning for what comes next. Their lawyer has billed $85,000 in transaction fees. The owner's personal circumstances that motivated the sale have not changed.

The buyer calls to propose a meeting to discuss "resolution of the outstanding diligence items." The meeting is proposed for the following week. The buyer mentions, in passing, that their investment committee meets at the end of the month and that a delay beyond that date would require re-approval.

Every element of this scenario is a deadline management tactic. The extended diligence timeline has maximized the seller's accumulated investment. The three findings have been held back to arrive simultaneously rather than addressed individually as they were identified, creating a consolidated negotiating moment at a point of maximum seller vulnerability. The investment committee meeting introduces artificial urgency with a specific date attached. The meeting proposed for the following week prevents the seller from having adequate preparation time.

An owner negotiating directly is facing all of these dynamics simultaneously, with their own psychology working against them and no professional counterpart to interpret what is happening and advise on how to respond. Most owners in this position make concessions in that meeting that they would not have made six months earlier, when the same findings would have been contested on their merits.

An advisor in the same scenario would have managed the diligence timeline so it never reached week twelve. Would have addressed the findings individually as they arose. Would have identified the investment committee deadline as either genuine or tactical through professional relationship channels. And would have prepared the owner, in advance of the meeting, with a clear position on each item and the professional support to hold it.

What this means if you are planning to sell your business

The deadline management evidence produces four practical disciplines for any Canadian business owner approaching a sale.

First, understand your own timeline pressure honestly and completely before you begin. The buyers you will engage with will assess it accurately. An owner who knows their timeline, understands how buyers will read it and has designed a process that converts personal urgency into structured process urgency is far better positioned than one who discovers mid-negotiation that their personal circumstances are being used against them.

Second, design deadlines before you need to resist them. A competitive process with defined bid deadlines, management presentation windows and exclusivity conditions creates seller-imposed urgency that is structurally more powerful than any resistance an owner can mount against buyer-imposed deadlines. The time to build the clock is before buyers are engaged, not after they are already managing it.

Third, treat late-stage conditions as a pattern to be expected, not as surprises to be managed in real time. Every experienced M&A advisor in the lower-middle market has seen late-stage re-trading in the majority of transactions they have worked on. It is not exceptional. It is standard buyer practice. A seller who expects it, has prepared a response strategy and has a professional advisor to execute that strategy is not caught off-guard. A seller who discovers it for the first time in week twenty-two of an exclusive negotiation is negotiating without a map in territory the buyer knows well.

Fourth, be direct with yourself about the accumulation problem. The longer a transaction runs in exclusivity, the more expensive walking away becomes, and the more that expense works against your ability to hold firm on terms that matter. A well-run competitive process that maintains urgency among multiple buyers and preserves alternatives through the final stages of negotiation is the most effective protection against the investment accumulation trap. It does not eliminate the psychological cost of the final stretch. It ensures that the seller is not navigating that stretch alone, without alternatives and without professional support.

A note on the series

This is the eighth and final article in a series examining the foundational negotiating strategies documented by academic and practitioner research, applied to the specific context of selling a Canadian lower-middle-market business.

The consistent finding across all eight strategies is not that owners lack the intelligence or commitment to negotiate their own business sales. The finding is that these strategies operate through structural mechanisms, competitive process design, information asymmetry management, timeline architecture and professional pattern recognition, that are not accessible to a first-time negotiator operating without advisory representation, regardless of how capable or well-prepared they are.

The evidence base for advisory representation in lower-middle-market M&A is substantial, consistent and publicly available. The research has been cited throughout this series. The practical experience behind it spans tens of thousands of transactions in the Canadian and North American lower-middle market.

The decision to sell directly or through an advisor is yours alone to make. This series has been written to ensure that when you make it, you make it with full awareness of what each approach actually involves.

Sources and further reading

Malhotra, D. (2004) — "The pursuit of power in negotiation" — Harvard Business School hbs.edu/faculty/Pages/item.aspx?num=16979

Malhotra, D. and Bazerman, M.H. — Negotiation Genius (Bantam Books, 2007) amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

Axial — Why deals fall apart (2022) axial.net/forum/why-deals-fall-apart

Golubov, A., Petmezas, D. and Travlos, N.G. (2012) — "When it pays to pay your investment banker" — Journal of Finance doi.org/10.1111/j.1540-6261.2012.01741.x

Fisher, Ury and Patton — Getting to Yes (3rd ed., Penguin Books, 2011) amazon.com/Getting-Yes-Negotiating-Agreement-Without/dp/0143118757

Rosenbaum, J. and Pearl, J. — Investment Banking (Wiley, 2022) wiley.com/en-us/Investment+Banking:+Valuation,+LBOs,+Mergers,+and+Acquisitions-p-9781119706182

Pepperdine University Private Capital Markets Report (2024) bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

GF Data M&A Report (2023) gfdata.com/resources/reports

This Concludes the series

Eight negotiating strategies for Canadian business owners; The complete series covers BATNA, anchoring, separating people from the problem, interests versus positions, multiple simultaneous offers, strategic silence, process control and deadline management. Each article is available individually on this site. If you found this series useful, Karl E. Sigerist, Jr., ICD.D has written the definitive guide to selling a Canadian business: Selling Your Canadian Business: A Step-by-Step Guide to Maximizing Value and Securing Your Legacy, available now

The complete series

Click any article to read in full

Strategy 1 · Leverage & alternatives | BATNA — know your best alternative to a negotiated agreement

How competitive alternatives determine who holds power at the negotiating table, and why the development of a strong BATNA is fundamentally different in an owner-direct versus advisor-led process.

Strategy 2 · Opening position | Anchor first and anchor high

Who sets the opening number, and why that decision shapes the entire deal. The research on anchoring bias and what it means when an owner anchors without preparation, or fails to anchor at all.

Strategy 3 · Relationship management | Separate people from the problem

Why emotional entanglement is the most costlynegotiating error business owners make, and how professional buyers exploit it deliberately, through tactics that are entirely standard in their world and entirely unfamiliar in the owner's.

Strategy 4 · Deal structure | Focus on interests, not positions

How understanding what buyers actually want — rather than what they say they want, creates deal structures that maximize total value. Why positional bargaining leaves money on the table and interests-based negotiation finds it.

Strategy 5 · Offer construction | Multiple simultaneous offers of equivalent value

How presenting two or three complete deal packages simultaneously reveals buyer priorities without a single unilateral concession, and why the analytical preparation required to do it well is beyond most owner-direct negotiations.

Strategy 6 · Communication discipline | Strategic silence

The discipline of not talking, and why most owners unknowingly concede with every word they speak after making an offer. How an advisor-managed process builds silence structurally into the negotiating dynamic, so the owner never has to fight the instinct to fill it.

Strategy 7 · Process architecture | Control the process, not just the outcome

Why process design is the most consequential negotiating variable in a business sale, and why it is structurally inaccessible to owners who negotiate without an advisor. A stage-by-stage comparison of what a designed process delivers versus a default one.

Strategy 8 · Series finale | Time pressure and deadlines

How the final 20 per cent of available time shapes the majority of concessions, and who controls the clock when it matters most. The deadline effect, the four tactics buyers use to manufacture timeline pressure, and why clock management governs all seven strategies that precede it.