WHO CONTROLS THE PROCESS CONTROLS THE OUTCOME

Who controls the process controls the outcome

Most Canadian business owners focus all their energy on negotiating the deal. The owners who get the best outcomes focus first on designing the conditions under which the deal will be negotiated. Those are not the same thing, and the difference between them is worth more than any single negotiating tactic.

This is article 7 of 8 in a series examining the foundational negotiating strategies documented by academic and practitioner research, and comparing the relative strengths and weaknesses of owner-direct versus advisor-led negotiation in Canadian lower-middle-market business sales. Each article draws on peer-reviewed research, transaction data and more than 30 years of Canadian M&A advisory experience.

Process is not administration. Process is power.

There is a common misconception about what M&A advisors actually do. The assumption is that their primary value lies in the negotiation itself: arguing for a higher price, pushing back on due diligence findings, drafting better terms. These things matter. But they are not where the most significant value is created.

The most significant value in an advisor-led business sale is created before the negotiation begins, in the design of the process through which the negotiation will occur. The timeline. The information disclosure sequence. The buyer identification and engagement strategy. The structure of management presentations. The bid process letter. The data room architecture. The exclusivity trigger. Each of these is a deliberate design decision that shapes what buyers can do, when they can do it and what leverage they hold at each stage of the transaction.

This is process control, and it is the most consequential negotiating lever available to a business seller. It is also almost entirely inaccessible to owners who negotiate directly, not because they lack intelligence or commitment, but because exercising process control requires a specific combination of transactional pattern recognition, buyer relationship management and process architecture experience that only comes from having managed many transactions.

The seller who controls the process does not simply negotiate better. They negotiate in conditions that have been deliberately engineered to favour their outcome before the first substantive discussion occurs.

What process control actually means

Process control in a business sale encompasses every decision about how the transaction will be structured from initial buyer contact through to closing. It is useful to break it into five distinct dimensions, each of which represents a specific point of leverage that can serve the seller's interests or the buyer's, depending on who is making the decisions.

Buyer universe management

The first process control dimension is the identification and sequencing of buyer contact. Who gets approached? In what order? With what information? At what stage of the process?

A seller who controls this dimension can ensure that the full universe of qualified buyers is identified and engaged, that strategic buyers and financial sponsors are introduced in a sequence that maximizes competitive tension, and that no single buyer gains an informational advantage over others that could be used to undermine the competitive dynamic. A seller who does not control this dimension, typically an owner who engages with the first buyer who approaches them, has already surrendered the most important source of leverage available in the lower-middle market.

Information flow management

The second process control dimension is the staging and sequencing of information disclosure. What does a buyer receive at first contact? What additional information is provided at the management presentation stage? What is held back until exclusivity? What is released only in the data room under defined access conditions?

Information is asymmetric in every business sale. The seller knows the business far better than any buyer ever will at the point of offer. That asymmetry can work for the seller or against them, depending on how information flow is managed. A seller who releases all material information at first contact has eliminated one of their primary process advantages. A seller who stages disclosure deliberately, releasing enough to drive buyer enthusiasm while holding back enough to sustain leverage, is using process control to extend their informational advantage throughout the transaction.

Timeline management

The third dimension is timeline. When does the first round of bids close? How long is the management presentation period? When does exclusivity begin? How long does due diligence run? When is the signing deadline?

Timeline control is leverage in both directions. A compressed timeline creates urgency among buyers and reduces the window for second-guessing, renegotiation and competitive disruption from outside the process. An extended timeline, when it serves the seller's interests, can be used to develop alternative options, manage buyer fatigue strategically or wait for market conditions to improve. A seller who controls the timeline makes these choices deliberately. A seller who responds to the buyer's timeline has no choices at all.

Exclusivity management

The fourth dimension is exclusivity: the point at which the seller agrees to negotiate with a single buyer and suspends contact with others. Exclusivity is a significant concession. Once granted, the competitive tension that drove the process evaporates entirely, and the seller's BATNA weakens dramatically. Buyers know this and push for exclusivity as early as possible in the process, often before the seller has sufficient information to assess whether the exclusivity terms justify surrendering competitive leverage.

A seller who controls the exclusivity decision grants it only when the buyer's commitment and offer terms genuinely justify the concession, on a timeline and under conditions that the seller has designed rather than accepted. A seller operating without process discipline grants exclusivity in response to buyer pressure, at a moment that serves the buyer's interests rather than their own.

Due diligence management

The fifth dimension is due diligence scope, access and timeline. What records does the buyer have access to? In what format? On what timeline? Under what confidentiality protections? Who in the seller's organization interacts with the buyer's diligence team, and on what terms?

Due diligence is not merely an information verification exercise. It is a renegotiation opportunity that buyers use deliberately. Findings that emerge in due diligence, both legitimate and manufactured, are used to justify price reductions, expanded escrow requirements and more aggressive reps and warranties. A seller who controls the due diligence process, through a well-organized data room, clearly defined scope limitations and a managed timeline, reduces the surface area available for tactical due diligence exploitation. A seller without process control has no mechanism to resist it.

RESEARCH NOTE: Golubov, Petmezas and Travlos, in their 2012 study in the Journal of Finance, examined the relationship between sell-side advisory representation and acquisition premiums across thousands of transactions. Their central finding is that sell-side representation is associated with significantly higher premiums, with the effect largest in precisely the conditions that characterize Canadian lower-middle-market transactions: smaller deal sizes, higher information asymmetry and less competitive buyer universe depth. The authors attribute the premium primarily to process management rather than to individual negotiating tactics. Source: doi.org/10.1111/j.1540-6261.2012.01741.x

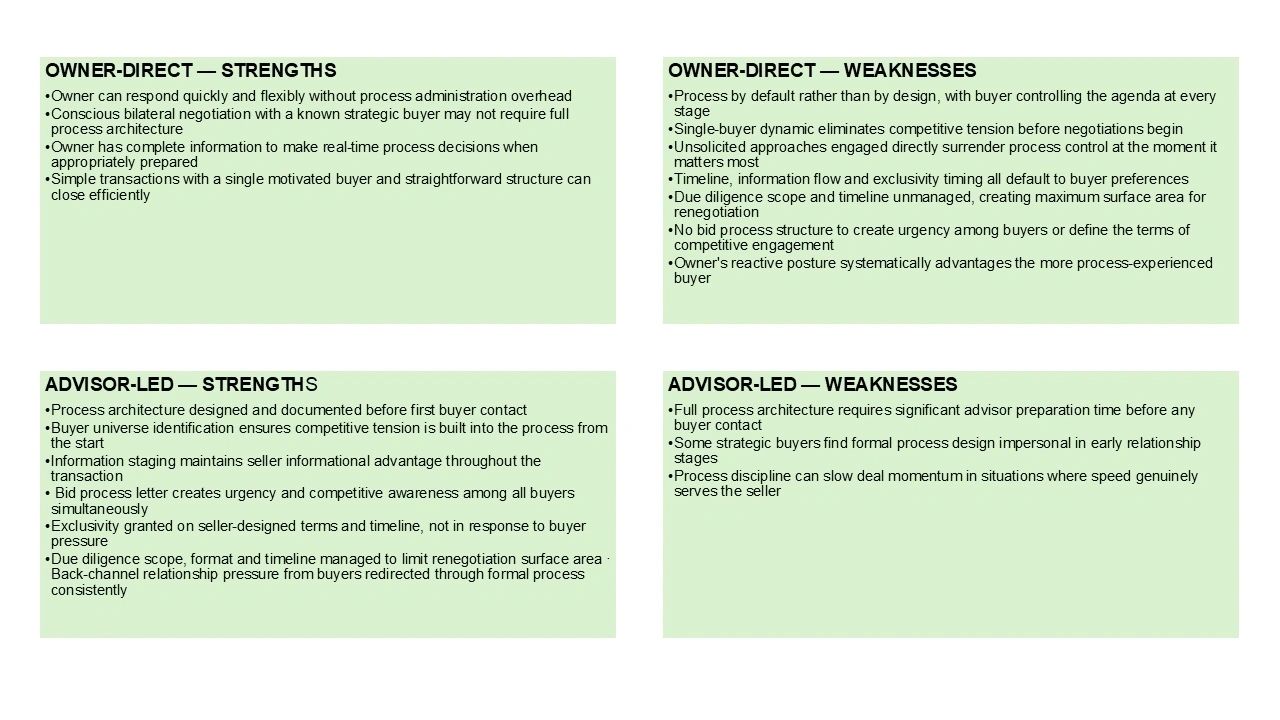

When the owner negotiates directly: process by default

The reactive posture

The defining characteristic of owner-direct negotiation, from a process control perspective, is that the owner is almost always reactive rather than proactive. The buyer initiates contact. The buyer proposes a meeting structure. The buyer requests information. The buyer introduces a term sheet. The buyer sets the exclusivity timeline. The buyer's diligence team determines the scope and pace of due diligence.

At each of these decision points, the owner who is negotiating directly responds to what the buyer has proposed rather than designing what the process will look like. This is not a failure of negotiating skill. It is a structural consequence of the absence of process architecture. The owner has not built a process, so the buyer's process fills the vacuum.

The result is a negotiation conducted entirely within a framework the buyer has designed to serve their interests. Even a highly skilled negotiator loses leverage when the conditions of the negotiation have been set by the other party.

The single-buyer dynamic

The process control problem is most acute in the most common owner-direct scenario: a single buyer, typically following an unsolicited approach, engaging with the owner in a sequential, bilateral conversation. In this context, the owner has no competitive process to manage, no information staging decisions to make and no timeline leverage to exercise. There is simply a conversation with a single buyer that proceeds on terms the buyer largely controls.

The absence of a competitive process is itself a process failure. It means that one of the most powerful process tools available to a seller, the visible and credible presence of competing buyers, has been surrendered before negotiations begin. Every other process control dimension is weakened as a result, because the buyer knows that the seller has no process to retreat to if this negotiation fails.

The unsolicited approach trap

A specific and common process control failure occurs when an owner receives an unsolicited acquisition approach and engages with it directly before designing a process around it. The buyer who initiates the approach has chosen their moment deliberately: they have assessed the owner's likely receptiveness, evaluated the business's current strategic position and identified a window in which the owner may be particularly open to a transaction.

By engaging directly and immediately, the owner accepts the buyer's process framing entirely. They are now in a bilateral conversation with a single party who initiated the engagement, controls the information flow and has the transactional experience advantage. The owner's correct response to an unsolicited approach is not to decline it, but to pause the direct engagement, bring in advisory representation and design a process that converts the unsolicited approach into a competitive dynamic. Most owners do not do this, because they do not recognize the process control implications of what has just happened.

What owner-direct negotiation does well here

There are transaction types where full process architecture is neither necessary nor appropriate. A business owner who has identified a specific strategic buyer, has a pre-existing relationship with that buyer and has made a deliberate, informed decision that a bilateral negotiation with that party is in their best interest can negotiate effectively without a formal advisory process.

This is a valid choice when made consciously and with a clear understanding of what process leverage is being surrendered. It is a very different thing from defaulting into a bilateral negotiation because an unsolicited approach arrived and engaging with it felt like the natural thing to do.

The distinction between a conscious process choice and a process default is important. Owners who make the conscious choice understand what they are trading away and why the trade is worth making in their specific circumstances. Owners who default into a process have made no such assessment.

When an M&A advisor negotiates on your behalf: process architecture as the first deliverable

Designing before engaging

The most important thing an M&A advisor does before contacting a single buyer is design the process through which buyers will be identified, engaged, qualified and ultimately selected. This is not administrative preparation. It is the strategic foundation of the entire transaction.

The process design determines the buyer universe, the information staging sequence, the timeline architecture, the bid structure, the exclusivity conditions and the due diligence framework. Each of these decisions is made deliberately, with the seller's objectives as the primary design constraint, before any buyer has the opportunity to influence them. By the time the first buyer receives the first communication, the process has already been designed to serve the seller's interests at every stage.

This is the core reason that advisor-managed transactions consistently achieve better outcomes than owner-direct ones. The advisor does not simply negotiate harder. The advisor negotiates in conditions that have been engineered to favour the seller before the first conversation begins.

The confidential information memorandum as process architecture

The confidential information memorandum, the document that presents the business to prospective buyers, is not simply a marketing document. It is a process architecture tool. Its structure, the information it includes and excludes, the financial presentation it employs and the narrative it constructs around the business's value and opportunity, all shape how buyers assess the business and what questions they ask.

A well-designed CIM answers the questions that would reduce buyer enthusiasm before they are asked, while creating questions about upside that sustain it. It presents the business at the level of the asking price, not at the level of what a buyer might assume before seeing the materials. It establishes a professional tone that signals the seller's expectations about how the process will be conducted. None of this is possible without a designed process, and none of it happens by default.

The bid process letter as leverage instrument

The bid process letter, the formal communication that instructs buyers on how and when to submit offers, is one of the most powerful process tools available to a seller. It establishes the timeline, defines the format in which offers must be submitted, sets the conditions under which buyers will be invited to proceed to the next stage and signals clearly that the seller is running a competitive process with defined rules.

Buyers who receive a well-designed bid process letter understand that they are competing against other qualified parties on a timeline they do not control. This understanding changes their behaviour. They submit more competitive offers. They respond more promptly. They are less inclined to test the seller's patience with low-ball initial bids. The bid process letter does not negotiate anything. It creates the conditions under which the subsequent negotiation will occur, and it does so entirely in the seller's favour.

Managing the buyer relationship to protect process integrity

Process control in an advisor-led transaction also extends to managing buyer relationships in ways that protect the integrity of the competitive dynamic. When buyers attempt to establish informal back-channel communication with the owner, the advisor redirects it through the formal process. When buyers attempt to accelerate exclusivity pressure outside the defined process timeline, the advisor manages the response. When individual buyers attempt to differentiate themselves through relationship investment in the owner rather than through competitive offer improvement, the advisor manages the distinction between the relationship and the commercial negotiation.

Each of these interventions protects the process architecture that the advisor has designed. Without them, the competitive dynamic that the process was designed to create erodes rapidly under buyer pressure, and the seller reverts to the bilateral, buyer-controlled dynamic that characterizes owner-direct negotiation.

Head-to-head: process control in owner-direct versus advisor-led negotiations

The process control test

Here is a practical test for any owner considering whether their current approach to a business sale gives them adequate process control.

Can you answer yes to each of the following questions?

Have you identified the complete universe of qualified buyers for your business, including buyers you do not currently have a relationship with, and designed a sequenced engagement plan for all of them?

Have you designed an information disclosure sequence that stages the release of material information in a way that maintains your leverage at each stage of the transaction?

Have you built a timeline architecture that creates genuine urgency for buyers while preserving your flexibility to extend or compress the timeline based on your interests?

Have you designed a bid process structure that makes competitive tension visible to all buyers simultaneously and defines the terms under which offers will be compared?

Have you established clear conditions under which you will grant exclusivity, and committed to not granting it earlier or on broader terms than those conditions specify?

Have you defined the scope, format and timeline of due diligence in advance, with a data room structure that provides buyers with the information they need while limiting the surface area available for tactical renegotiation?

If the answer to any of these questions is no, the process has not been designed. It is a default. And a default process serves the buyer's interests, not the seller's.

What this means if you are planning to sell your business

Three practical implications follow from the process control evidence for Canadian business owners approaching a sale.

First, treat the process design as the first and most important deliverable of the sale preparation, not as administrative overhead that follows the commercial decision to sell. The conditions under which your negotiation occurs will determine its outcome more reliably than any individual tactic applied within it.

Second, recognize that an unsolicited buyer approach is not a process. It is a buyer-initiated engagement on buyer-designed terms. Converting it into a seller-controlled process requires pausing the direct engagement, bringing in the appropriate representation and designing the competitive context before re-engaging. This step feels counterintuitive when a motivated buyer is at the door. It is almost always worth the delay.

Third, understand that the advisory fee you pay for a structured process is not primarily compensation for negotiating skill. It is compensation for process architecture: the design, management and protection of the competitive framework within which the negotiation occurs. That framework is the primary source of value in an advisor-led transaction, and it is the thing that is most completely absent when an owner negotiates directly.

Sources and further reading

Rosenbaum, J. and Pearl, J. — Investment Banking (Wiley, 2022) wiley.com/en-us/Investment+Banking:+Valuation,+LBOs,+Mergers,+and+Acquisitions-p-9781119706182

Golubov, A., Petmezas, D. and Travlos, N.G. (2012) — "When it pays to pay your investment banker" — Journal of Finance doi.org/10.1111/j.1540-6261.2012.01741.x

Axial — The sell-side M&A process guide axial.net/forum/sell-side-ma-process

Malhotra, D. and Bazerman, M.H. — Negotiation Genius (Bantam Books, 2007) amazon.com/Negotiation-Genius-Obstacles-Brilliant-Bargaining/dp/0553384112

Fisher, Ury and Patton — Getting to Yes (3rd ed., Penguin Books, 2011) amazon.com/Getting-Yes-Negotiating-Agreement-Without/dp/0143118757

Pepperdine University Private Capital Markets Report (2024) bschool.pepperdine.edu/institutes-centers/centers/applied-research/private-capital-markets

GF Data M&A Report (2023) gfdata.com/resources/reports

Next in the series

Article 8 of 8 Time pressure and deadlines: how the final stretch of a business sale negotiation is where most value is lost, why experienced buyers engineer the clock to work against sellers and what the research says about who controls the deadline controls the deal.

The complete series

Click any article to read in full

Strategy 1 · Leverage & alternatives | BATNA — know your best alternative to a negotiated agreement

How competitive alternatives determine who holds power at the negotiating table, and why the development of a strong BATNA is fundamentally different in an owner-direct versus advisor-led process.

Strategy 2 · Opening position | Anchor first and anchor high

Who sets the opening number, and why that decision shapes the entire deal. The research on anchoring bias and what it means when an owner anchors without preparation, or fails to anchor at all.

Strategy 3 · Relationship management | Separate people from the problem

Why emotional entanglement is the most costlynegotiating error business owners make, and how professional buyers exploit it deliberately, through tactics that are entirely standard in their world and entirely unfamiliar in the owner's.

Strategy 4 · Deal structure | Focus on interests, not positions

How understanding what buyers actually want — rather than what they say they want, creates deal structures that maximize total value. Why positional bargaining leaves money on the table and interests-based negotiation finds it.

Strategy 5 · Offer construction | Multiple simultaneous offers of equivalent value

How presenting two or three complete deal packages simultaneously reveals buyer priorities without a single unilateral concession, and why the analytical preparation required to do it well is beyond most owner-direct negotiations.

Strategy 6 · Communication discipline | Strategic silence

The discipline of not talking, and why most owners unknowingly concede with every word they speak after making an offer. How an advisor-managed process builds silence structurally into the negotiating dynamic, so the owner never has to fight the instinct to fill it.

Strategy 7 · Process architecture | Control the process, not just the outcome

Why process design is the most consequential negotiating variable in a business sale, and why it is structurally inaccessible to owners who negotiate without an advisor. A stage-by-stage comparison of what a designed process delivers versus a default one.

Strategy 8 · Series finale | Time pressure and deadlines

How the final 20 per cent of available time shapes the majority of concessions, and who controls the clock when it matters most. The deadline effect, the four tactics buyers use to manufacture timeline pressure, and why clock management governs all seven strategies that precede it.